MEI Pharma: Massive upside not reflected in today's price $MEIP

A failed Phase II trial for their main drug caused investors to abandon MEI Pharma (MEIP)

Today, the company trades for below net cash

Despite the failed trial, some recent good news suggest there could be significant upside potential hiding here

This week the blog is focused on companies trading for less than cash value. We started off with Opthotech (OPHT) on Sunday (and gave an update this morning!) and then covered Dyadic (DYAI) on Tuesday (disclosure: I’m long both DYAI and OPHT). Today, we focus on MEI Pharma (MEIP; disclosure: long), probably my favorite of the group.

MEIP’s backstory is very similar to OPHT's. MEIP’s primary drug is Pracinostat (Prac). The market was very excited about Prac for use in MDS. However, in early 2015, MEIP announced their phase II trial for MDS failed to meet its primary clinical endpoint. The market’s response was… not kind.

However, similar to OPHT, that massive sell off could represent opportunity for value investors. At today’s price of ~$1.50, MEIP is trading for a discount to the ~$1.60/share in cash on their balance sheet. In addition, I think MEIP has several avenues to hidden growth that could lead to shares being a multi-multi-bagger from today’s prices.

Let’s start with some background. MEIP develops drugs for the treatment of cancer. They currently have 3 drugs. Two of them, ME-401 and ME-344, are promising but very early stage. If they work out well, they could and would drive significant value. In the short term, they will be small to medium cash drags as the company invests in cash to fund clinical trials for them. For simplicity, I will assume each of them are worth nothing, though given the lottery ticket nature of early stage drugs they will either be a mild negative or a huge home run.

The main reason to be excited about MEIP is Pracinostat (Prac). Prac is an HDAC inhibitor used for treating cancer. Specifically, it is targeted for patients with Myelodysplastic syndromes (MDS) or Acute Myeloid Leukemia (AML) who cannot handle intensive chemotherapy, either for health reasons or because they are old (75 years old or older).

Some background here will help explain how the opportunity popped up. MDS is basically a prelude to AML; patients w/ MDS are often healthy and the disease can be treated in ambulatory clinics. However, if MDS is not treated, it can/will lead to AML, which is a much more serious condition that carries an extremely poor outlook (untreated, life expectancy is 6 months or less). Once diagnosed w/ AML, patients are immediately put on chemo if they are healthy enough to take it. However, many patients over 75 so they're not healthy enough to be put on chemo (i.e. Prac's target market). AML is the most common form of adult leukemia (~25% of adult leukemia in the western world).

As mentioned above, Prac failed its phase II trial for MDS in early 2015. Shares have consistently traded in the low to mid $1 range since failing that trial. In many ways, it feels like MEIP has been left for dead: investors were burned investing in MEIP once, and they have no desire to enter the company now that it trades below net cash.

I don’t think that’s quite fair. In fact, I think that’s missing a lot of good news that has come MEIP’s way in the past year or so.

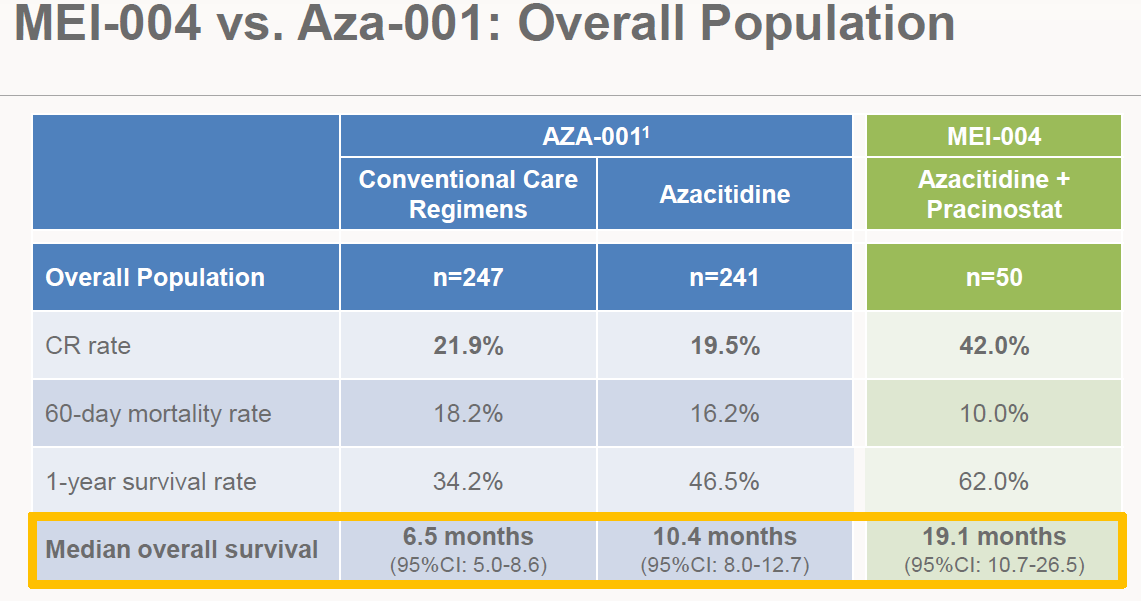

First, in late 2015, the company reported positive Phase II results for Prac in AML. On August 1, the FDA gave Prac breakthrough designation for AML as well as reaching agreement on phase III trial design. MEIP immediately followed all of this up by entering into a strategic agreement w/ Helsinn. The strategic agreement licenses Prac to Helsinn in exchange for a $5m equity investment (priced at $1.91/share), $20m in upfront payments, $444m in regulatory and sales based milestones, royalties once the drug starts selling, and Helsinn agreeing to fund the global development of Prac.

That’s obviously a lot, but the summary is: Prac had very good news on AML. You can see the results above: complete response rate, survival rates, median survival rates; all were roughly double conventional care or the use of Aza standalone (a generic that is currently used to treat high risk AML patients). The FDA recognized the value of this and made Prac a breakthrough drug, which means it gets priority review from the FDA (designed to expedite drug development for serious or life threatening diseases; more here). And Helsinn saw the potential here and licensed MEIP’s drugs in exchange for funding the phase III.

The Helsinn partnership is huge for MEIP for several reasons. First, it somewhat validates the opportunity size here- the size of Helsinn’s upfront payment and equity investment suggest they think this has a chance of being a blockbuster drug (revenue well into the hundreds of millions per year) and validates the underlying research. Perhaps more importantly, it funds MEIP’s phase III trials. Running a phase III is hugely expensive, and with MEIP’s market cap approaching $50m raising equity to fund the phase III would have been incredibly dilutive. Helsinn’s partnership will fully fund the phase III trial while letting MEIP maintain material upside if the drug is successful / approved. The combo means MEIP no longer needs to raise equity, so current shareholders can fully participate in the upside if MEIP is approved.

And the upside here is potentially massive- $444m in milestone payments for regulatory approvals and sales plus royalties starting in the mid-teens and going up as sales increase. Those royalties could be huge; both the size of Helsinn’s investment and projections from a peer drug by Celator (discussed later) suggest Prac could do >$500m in peak sales on approval, so the royalty payments could easily be >$100m/year if approved. Prac’s patent don’t expire until 2028, so if you assume the drug is approved by ~2020 and ramps up to >$500m in annual sales, MEIP could easily be looking at a total royalty stream of over $1B from 2020 to 2028. Obviously you’d need to risk adjust that number, tax it, and discount it back to the present, but I’ve played around with all of the numbers and the bottom line is this: if Prac is a success and the royalties come anywhere close to those levels, MEIP is going to be looking at multiples of today’s share price in royalties (using a 10% discount rate, I got an NPV of their royalty stream between $15-25/share. Note that number is neither risk adjusted nor taxed and that I don’t feel like sharing all of my assumptions I used to get there (you get what you pay for!), but you can probably back into them pretty closely). MEIP management has also suggested they can extend their composition of matter patent on PRAC for five years through patent restoration; if they’re right, it would add another $500m-$1B in royalties using the above assumptions.

To reaffirm that I’m not completely crazy in thinking the drug could be worth ~$1B, it’s worth looking at Jazz Pharma’s recent $1.5B acquisition of Celator. Celator had one drug: VYXEOS. Vyxeos is an IV drug targeting AML. The drug completed a successful phase III trial in March 2016; however it had not yet received a new drug application (NDA). The successful phase 3 trial sent Celator’s stock skyrocketing- from $1.68 to just under $9/share. As soon as the trial was reported successful, Celator’s phone started ringing off the hook with acquisition offers. A review of the company’s merger filing shows at least 6 companies trying to acquire them after phase 3 trials were successful. Eventually, Jazz won with a bid of $30.50/share (~$1.5B); a 73% premium to the prior day’s closing price and ~15x higher than the share price the day before the trial was declared a success. As discussed in the risks section, I don’t think Celator is a perfect comp because they owned the rights to Vyxeos versus MEIP licensing out Prac, but Celator’s premium does reaffirm the market opportunity and show how lucrative a successful drug could be. Celator’s base case in their projections had Vyxeos peaking at ~$800m in revenue in 2028, and Jazz obviously thought the market potential was huge to be willing to pay $1.5B for a one drug company before the drug was officially approved by the FDA.

To realize Prac / MEIP’s upside, we’ll need a successful phase 3 trial. But what are the odds of a successful phase III trial?

For that, I suggest turning to the “clinical development success rates 2006-2015” from Biomedtracker. According to Biomedtracker, the overall odds of approval for phase III drugs is ~50%. The overall odds of approval for oncology drugs is lower than that at ~34%. AML phase III drugs have a slightly lower overall rate of approval, but that is on a somewhat small sample size (only 11 drugs). Hematological cancer phase III (which AML is a subset of) actually has a higher odd of approval than oncology, so overall I feel comfortable saying that our base rate for approval of Prac is 34%. Based on the data we’ve seen so far for Prac, the higher than normal odds of success for hematological cancer, and the confidence in the data Helsinn’s investment implies, 34% may actually be conservative (i.e. this drug’s chance of approval could be better than a typical drug given the underlying data) but I think 34% is good for a base case.

So if we put all of that together, we’ve said that Prac’s royalty is worth at least $15/share in NPV w/o risk adjusting or taxing it. Assume a ~33% chance of approval, and the royalty is worth $5. Maybe it’s worth $4 after adjusting for taxes. Either way, that’s significantly higher than today’s share price… and we haven’t even included any potential value from Prac getting approved for MDS or any other indication.

It’s true Prac failed its initial MDS trial. However, a further look at the data revealed that was mainly due to people dropping out of the trial right when they started taking the drug, and that patients who stuck with the drugs actually reported strong underlying data. MEIP believes people dropped off the drug because of normal side effects (basically, side effects that are tolerable when you have AML and are going to die in a few months might not be tolerable if you have MDS and are generally healthy) and that proper dosing might fix the drop off problem. The MDS market is ~3x the size of the AML market, so any success there would be worth many multiples of today’s share price.

At today’s share price of ~$1.50, investors are paying basically nothing for any of that upside. The company has a market cap of ~$56m at today’s share price of ~$1.50. They have $58.9m in cash on their balance sheet at 9/30/16; in addition, Helsinn owes them another $5m (~$0.13/share) when they dose their first patient for the phase III AML trial or by March 1, whichever comes first. So investors are buying in a decent bit below net cash despite the potential upside, and unlike most net cash companies MEIP shouldn’t be burning too much cash in the near term as Helsinn will pay for the phase III AML trial, though cash burn could pick up if MEIP decides to fully pursue a re-trial of Prac for MDS (Helsinn splits costs of an MDS trial with them).

Are there risks here? Absolutely. In list form

Obviously your biggest risk is a failed phase 3 trial. Nothing to do about that- completely binary risk, and I feel extremely comfortable today’s share price more than compensates for that risk. Given the potential upside, the market is effectively pricing in a low to mid-single digit % chance of the phase 3 trial being successful (after adjusting for cash burn on the downside) and a 0% chance of any of the additional upside drivers discussed. Based on both the underlying data and base rates, that’s too low.

My other big worry here is insider ownership is minimal. This is somewhat typical for early stage biotechs based on my experience (OPHT, for example), but it can obviously lead to issues where management’s incentives and investor’s are not aligned. For example, if it becomes increasingly clear that Prac is going to fail its trial and that it would make more economic sense to stop trials and return cash to shareholders, management may prefer to keep the trials going and continue to collect a salary.

We may have seen an example of this in MEIP’s choice of Helsinn as a partner. Management explicitly stated that Helsinn’s support / agreement to cofund MDS trials was part of the reason they went w/ Helsinn. We will never know, but it’s possible management turned down better partnership offers that would not fund MDS because management knew the MDS lottery ticket would result in a huge pay day for them, even if no one else would fund it because it was uneconomical.

Heck, it’s even possible management turned down a takeout offer at a big premium because the potential upside for management from partnering and developing the drug far exceeds the small CoC agreements they would have gotten in a takeout, even if the takeout was at a huge premium.

It’s also worth noting that the shareholder base is pretty ripe for management abuse. No activists and no concentrated owners. As part of the licensing agreement, Helsinn bought a ~7% equity stake in MEIP for $1.91/share (another validation that someone sees a lot of upside here), but they did not take a board seat. With no activists or big owners on the board, the potential for shenanigans increases.

Ultimately, I take comfort here that everyone’s incentives should be aligned as what makes the most sense for everyone is a successful phase 3 trial for AML. Its success and the potential payoff to all parties dwarves everything else.

The end game here is unclear. Unlike Celator, MEIP no longer owns the worldwide rights to their drug. If the drug is massively successful, MEIP will own an incredibly valuable royalty stream, but what do they do with it? It’s not exactly an attractive acquisition candidate at that point- big pharma is willing to pay big premiums for unique drugs / assets, but they generally want to acquire full drug rights so they can push through their sales force, control pricing, and realize synergies. Helsinn might want to acquire MEIP to gain control of the royalty stream, but having only one logical buyer doesn’t make for a big premium. MEIP could take the royalty cash and invest it in drug development, but they’ll be getting so much cash from the royalties if Prac is successful it will way dwarf what they could reasonably invest in research (they could become a huge research shop, but they’d basically be blowing money to become a “me too” pharma player). They can sell off the royalty stream, but that creates taxable issues. Ultimately, I’m just saying the upside here is so big that I’m willing to stomach the fact the exit might be a bit suboptimal.

Catalyst time horizon: Prac is obviously the main driver of value here. Phase 3 trials start in early 2017 and we likely won’t know much about them until they start wrapping up in late 2019 / early 2020 or maybe even until they announce results and prep for launch (I’m assuming they announce results in early 2020 and launch by mid to late 2020, though I have seen bulls who think breakthrough status plus strong underlying data could be enough to get this approved in early 19 / launched late 19). While we’ll get some smaller news in the meantime (trials and trial results for their earlier stage drugs), 2019 / 2020 is obviously a long time horizon where the stock will be running “dead”. Maybe the market wakes to the opportunity in the meantime, or maybe I’m wrong and we get preliminary dosing data when the trials are running, but most likely we are just waiting….. waiting…. waiting while the company is burning cash to cover SG&A. Again, given the massive upside, I’m comfortable holding and waiting, but it is a frustrating scenario that can introduce a lot of other risks into the equation.

Drug pricing- for this to be a home run, they need to be able to charge current cancer drug like pricing ($50K+ minimum). A single payor system, big healthcare overhaul, Bernie Sanders style “revoke patents for expensive drugs”, etc. would all be a disaster.

Here, I take comfort in three things. 1) Pfizer bought MDVN for a massive, massive premium last summer, and MDVN was the direct target of the Bernie Sanders patent revocation rant. 2) Similar to PFE / MDVN, Takeda just paid a huge premium for Ariad despite a Bernie Sanders “castigation. 3) A lot of the milestone payments are regulatory related, so even if pricing was hugely hit you would still get some upside from the milestone payments.

Patent issues- lowest in my concerns but still relevant as a tail risk; if the Prac patents are invalidated for any reason, all of this upside goes away.

MEIP has an incredible patent portfolio for Prac- orphan designation (the absolute strongest protection) for the drug alone plus working on it for prac + aza (which would be a home run) and composition of matter through 2028 at the earliest.

Cure for cancer / huge medical breakthrough- probably not a near term risk, but the drug won’t come out till 2019 / 2020. It’s not completely out of the realm of possibilities that by 2020 we are staring at massively improved treatment options for cancers that make this drug obsolete or on the verge of being obsolete, but this risk is a moonshot possibility.

Overall, an investment in MEIP is probably going to involve a lot of waiting and praying, but if Prac pays off, the rewards to shareholders at today’s prices is going to be substantial.