Something's BREWing at CBA $BREW

Craft Brew Alliance (ticker: Brew, but nicknamed CBA) new deal with Anheuser-Busch could lead to a buyout at a big premium.

Declines at other brands have hidden Kona's growth recently, but that should change in the near future

At today's prices, shareholders have multiple ways to win.

In August, Craft Brew Alliance (ticker: BREW; CBA for this article; disclosure: long) announced a deal to expand their distribution agreement with Anheuser-Busch (AB). The agreement was complex, but what really interested me about it was the agreement included a framework for AB to acquire CBA. Per the 8-K,

“Under the terms of each of the Brewing Agreement, the International Distribution Agreement, the Master Distributor Agreement and the Recapitalization Agreement (as defined below) (collectively, the “Commercial Arrangements”), a “qualifying offer” is defined to include any offer made by ABCS or an affiliate thereof, for the acquisition of all of the issued and outstanding shares of common stock of CBA (“CBA Common Stock”) not owned by ABCS or its affiliates, on customary terms and conditions for a transaction of the type proposed by ABCS or its affiliate, in each case, for an aggregate value of (x) not less than $22.00 per share of CBA Common Stock if the offer is made between the date of the Brewing Agreement and on or prior to August 23, 2017, (y) not less than $23.25 per share of CBA Common Stock if the offer is made between August 24, 2017 and on or prior to August 23, 2018 and (z) not less than $24.50 per share of CBA Common Stock if the offer is made on or after August 24, 2018.”

I kept turning my wheels on that buyout clause and wondering why either party would put it in there unless AB was truly serious about acquiring CBA. And the more I thought about that sale arrangement, the more I was reminded of this VIC write up by Charlie479. The underlying thesis of that write up was fantastic, but I’ll boil it down to this: AmBev exchanged some of their operations with Quinsa and took an equity stake in them as a result; in addition, AmBev got a put/call option that allowed them to acquire Quinsa for a predetermined price that was significantly higher than the price Quinsa was trading at.

The similarities between Quinsa then and CBA now are striking. Agreed upon buyout offer formulation at a price higher than today’s? Check. Strategic acquisition target? Check. AmBev is the buyer and already owns a minority stake in the target? Check (AmBev, which bought Quinsa, has evolved into AB through mergers and currently owns ~1/3 of CBA).

The deal between CBA and AB is pretty complex, but there are three main pieces to it (in addition to the buyout clause): the amended master distributor agreement, the contract brewing agreement, and the international distribution agreement.

Amended Master Distributor Agreement: CBA has used AB as their exclusive master distributor in the U.S. for years (the relationship dates back to 1994, and the agreement had last been modified in 2011). The prior agreement was up for renewal in December 2018. The new agreement extends the deal through 2028. In addition, the prior agreement had a distribution fee of $0.25/case that CBA paid AB; that fee was set to go up to $0.75/case in 2018. The new agreement keeps the fee at $0.25/case provided that CBA reinvests half the savings into marketing in key strategic markets.

Contract Brewing Agreement: CBA can shift up to 300k barrels of beer/year from their own facilities into AB’s facilities, and AB guarantees cost savings of $10/barrel for any barrel shifted to them.

International Distribution Agreement: AB gets the exclusive right to distribute CBA in any country CBA hadn’t already awarded rights to, including Mexico, Brazil, and Chile. CBA manages the export and AB pays CBA a royalty fee of $30-40/barrel plus shipping costs. In addition, AB promises minimum payments of $3m in 2016, $5m in 2017, $6m in 2018, and an incentive payment of $20m in 2019 before shifting to that royalty fee structure.

To me, the bottom line is the deal clearly incentivizes both sides to merge sometime before August 23, 2019. On CBA’s side, AB can hit them for pretty significant penalties (cancellation of all the one time payments, pulling their distribution agreement) if CBA declines to be acquired by AB after AB makes an offer. On AB’s side, those onetime payments for international rights are pretty significant and the overall terms of the deal are pretty generous to CBA. Given the market cap of non-AB owned CBA shares would be ~$325m at a share price of $24.50 (the minimum takeout price in 2018), I can’t see AB looking at that $20m incentive fee in 2019 and thinking it makes more sense to pay that fee versus buy all of CBA, particularly once the substantial potential synergies from taking CBA in house are factored in.

So the upside here is pretty obvious. AB seems pretty interested in acquiring CBA based on this contract, and if AB bought CBA out currently, it would be for “not less than” $22/share. Shareholders would obviously be pretty happy with that outcome given shares are currently at ~$13 (assuming the offer comes before that $20m payment is due in August 2019, the IRR from today’s prices ranges from >30% on the low end to well over 100% on the high end depending on the timing of the offer). Management would make out pretty well too: they updated their CoC payments in May 2016 to provide a pretty nice payday if they get bought out.

I’ll dive into the business in a second, but given all that is public information (CBA even highlights the buyout agreement in their IR presentations), it’s worth asking real quickly: why does this opportunity exist? I think there are three main reasons:

Craft Brew Hangover: This Barron’s article on Boston Beer’s (SAM, which owns Sam Adams and a few other brands) weak Q4’16 earnings / FY17 outlook does a nice job covering it, but basically craft brewing grew rapidly over the past 20 years, and that growth attracted a huge number of new breweries. As the industry’s growth has slowed over the past few years, competition has gotten intense. Large players are entering with their own craft brands (a trend that CBA helped start when they sold their stake in Goose Island to AB), local and regional players are popping up all the time, and the sheer number of choices can be overwhelming for consumers and push them back to “big beer”.

This can seem small when you first hear it, but I think it’s a real question mark for the larger Craft Beer players going forward. Craft Beer has traditionally been a premium priced product that took a bit of effort to find; I went to Duane Reade the other day and they had a full craft beer aisle (including some Kona). It’s certainly worth wondering if some of these larger craft brands are hurting their premium perception / getting lumped in as big beer by significantly expanding their reach and are vulnerable to losing share on both ends as a result (become more of a middle ground player and lose to the regional / local players on the high end and “big beer” on the lower end).

Management lost credibility: The accounting issues / Friday night filing I’ll mention in the next bullet doesn’t help, but management also has a history of providing aggressive guidance and then waiting until it is completely impossible for them to meet guidance to cut. I think that past has shot a lot of their credibility with investors. I’ll give two examples of this:

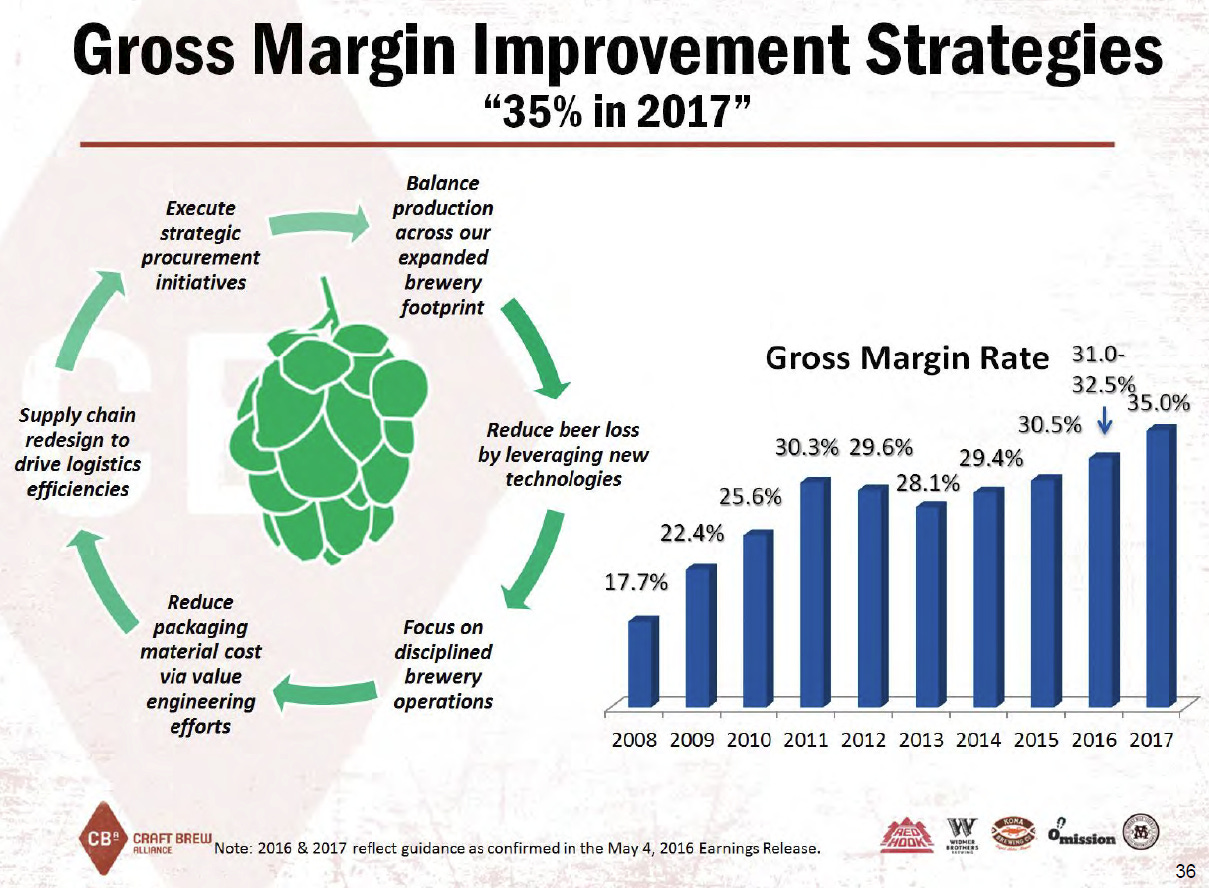

CBA badly missed their original guidance for FY15. They had a very rough Q1’16, causing one analyst to ask them why they felt confident sticking with their 2016 guidance in light of how off they were for 2015. Management gave a lot of explanation on how seriously they were taking the 2016 guidance and how much faith they had in hitting their targets. Management proceeded to cut 2016 guidance after a pretty poor Q3, and then managed to miss even that guidance when they posted FY16 results (full year gross margin, for example, was 29.4%, 160 bps below their guidance range).

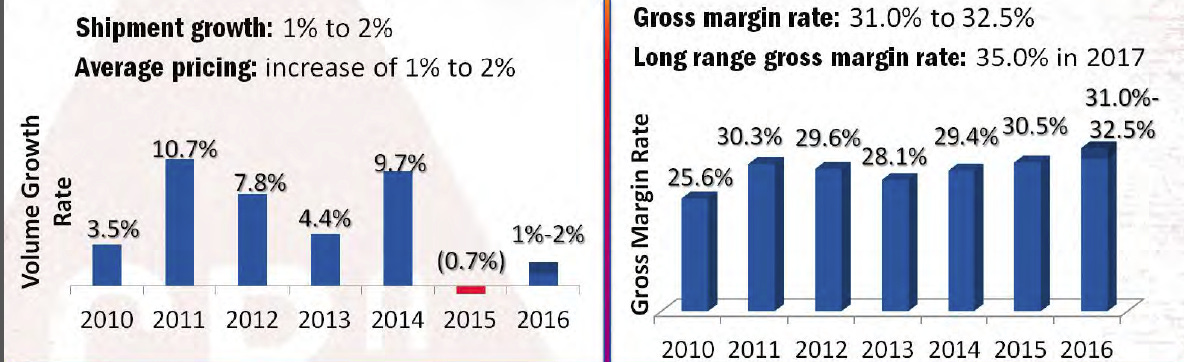

Since October 2014, management has been guiding to “35% in 2017”; that was their target of 35% gross margins by 2017 supported by a large two year capex program. They reiterated this target as recently as September 2016 (see slide below). They even went so far as to talk about it in the August 2016 call announcing the new AB deal and highlighting that their 35% guidance did not factor in all the benefits from the new AB deal (suggesting that the AB deal would let them improve on that number). Then, in their Q3’16 call in November, management suddenly stopped mentioning “35% in 2017”; they didn’t confirm that they were dropping the target until a caller asked them about it during Q&A. In their FY17 guidance, they guided to a GM of 30.5% to 32.5% for the full year.

I talked to the CFO pretty extensively about these issues. I don’t really care if a company gives guidance or not, but for a company to give out guidance and then miss it that badly consistently obviously raises a lot of red flags about internal forecasting. FWIW, he laid out clear reasons why they had missed (mainly, the capex programs didn’t ramp up like they were hoping and the gross margins from the AB deal getting pushed out plus several other things that seemed relatively one time), even if I didn’t agree with / like a lot of them. I came away feeling decently that a lot of the issues had been corrected.

Earnings / 10-K Delay: On Feb. 23, CBA delayed their full year earnings call and the filing of their 10-K until March 13; on March 10th, they filed a dreaded Friday night press release (at 9 PM EST!) announcing they wouldn’t hit the March 13th deadline and would “announce the timing for the release of its 2016 financial results and related conference call details shortly”. The reason for the delay was actually pretty innocuous (accounting treatment for the AB international payments), but to delay earnings twice and put out a late Friday night release like that is not a great look for a management team.

Alright, so let’s dive a bit deeper into CBA. As you might guess from the name, CBA is a craft brewing company. Their major brands are Redhook (Seattle area), Widmer (Portland), and Kona (Hawaii). They also have Omission, which is the largest Gluten Free beer with ~45% market share of an admittedly extremely small market. All in, CBA measures themselves as the 6th largest craft brewing company; I’ve got some issues with the way the chart below is set up since it gives companies credit for every beer the own, but however you cut the data CBA is a major player in the craft space and Kona is one of the biggest brands in craft beer.

Until late 2014 / early 2015, CBA was focused on growing all three of their brands into national brands. However, as the craft segment got more competitive, CBA adopted their “Kona Plus” strategy: the Kona brand would be their flagship national brand, and they would “retrench” Widmer and Redhook from national sales to focus more on their local markets. To replace the lost sales from Widmer/Redhook in their non-home markets, CBA would begin striking up alliances with interesting local brewers that took advantages of the local brewers’ brand strengthen and CBA’s distribution with AB. The retrenchment decision has had a big impact on their financials: while the Kona brand has seen continued strong growth (shipments up high teens annually) the other two brands have seen strong declines which has led to a relatively stagnant total shipments / revenue numbers for CBA for the past few years.

Ok, so you’ve got a business that has shown flat growth for several years and a management team with little to no credibility with the street at this point. Aside from the possibility of a buyout, what makes CBA attractive today?

Growth inflection point: I think we should be hitting an inflection point today where CBA can start showing growth again in the near future: Kona now accounts for well more than 50% of CBA’s shipments (~53% in FY16 and growing), so any future declines from Widmer / Redhook should be more than offset by Kona’s growth if Kona can grow anywhere close to today’s rates.

International is still a “small percentage” of CBA’s business but it’s growing quickly (Kona international was up 43% in 2016 per the Q4 call). AB is paying CBA $34m in fixed payments over the next three years for the right to distribute internationally; the only way AB could justify paying that much (plus the $30-40/case royalty) is if they saw a pretty big international opportunity.

Kona brand: Kona’s the real reason to be excited about CBA. It’s more than tripled shipments over the past seven years (shipped ~113k barrels in 2009to just under 400k in 2016), and it’s not really showing signs of slowing down (the Q4 earnings highlighted Kona depletions up 17% YTD through Feb.). The AB deal also seems very centered around Kona: the agreement calls for CBA to reinvest some of their savings into Kona marketing, and it gives ABI international distribution of CBA’s beers in most markets. The international distribution agreement was almost certainly designed with Kona in mind, as Kona’s a beer / brand that will likely travel very well. I think it makes sense in general that the whole AB / CBA agreement was centered around Kona: CBA decided Kona was their best brand for national / international relevance, and AB probably isn’t interested in buying brands that can’t at least be distributed nationally given a regional brand doesn’t budge the needle at all for them / isn’t worth their time.

The AB acquisition formula seems to be written with the Kona brand specifically in mind. Peer Lagunitas sold to Heineken at an $800m valuation, or >$1,000/barrel, in late 2015. Acquisition multiples have likely come down a bit since then given the slowdown in craft beer, but it’s interesting to note that AB’s current $22/share offer price would imply a valuation price of ~$1k/barrel on 2017E Kona shipments assuming Kona continues to grow in the mid-double digits (it’s <$1,200/barrel on LTM Kona barrels). If you assume AB is really only interested in Kona, it makes sense that their takeout price framework would only give CBA a value for Kona.

This could also prove important for regulatory /antitrust issues: it’s possible AB would need to dispose of some of CBA’s brands to acquire them; if they do, they could literally hand them away and still feel good about it given they’re only paying for Kona at these levels.

Management has been ramping up marketing spend for Kona in the past few quarters, and the AB agreement specifically calls for some of their cost savings to go to increased marketing investment in Kona. The increased spend should support continued strong growth for Kona.

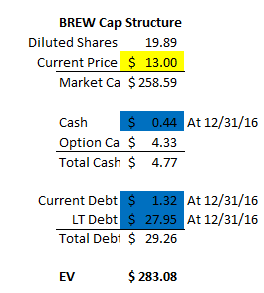

Margin expansion opportunity: In addition to hitting a growth inflection point, I think CBA is at a point where they have the ability to significantly increase their gross and operating margins. All told, I see a relatively easy path to $10m in annualized cost cuts just from things that have already been announced (pretty significant versus a <$300m EV at today’s share price of ~$13.00), and I would be surprised if there wasn’t significant room for more cost leveraging either as a standalone business or from a strategic acquirer. The margin expansion will be driven by three things: the AB agreement, operating leverage, and internal cost cutting.

AB agreement: Part of the AB agreement called for CBA to brew 300k barrels annually at AB owned facilities instead of CBA’s own facilities (they will have shifted 150k by FY17 yearend). As part of the deal, AB guaranteed CBA that they would cut the cost per barrel by $10 within one year of beginning production. That’ll translate in $3m in cost savings annually for CBA, and both sides have agreed to explore further cost cuts as the program ramps up.

Interestingly, switching 300k barrels from CBA’s facilities to AB’s won’t just provide CBA with significant cost savings; it will also provide them with significant growth opportunities. At YE16, CBA had production capacity of 1,075,000 barrels, and they were investing another $25m to add ~300k barrels ($10m for 200k in Portland and $15m for 100k in Hawaii). Switching that much capacity from internal facilities to AB gives CBA significant untapped capacity to use for building partnerships / alliances to help local brands scale.

Internal cost cutting: As part of their Q3’16 earnings, BREW announced plans to cut $5-7m in annual costs. The company hasn’t laid out much more on those plans, but obviously versus an LTM EBTIDA number of ~$12m that could make for a pretty nice earnings boost.

A lot of that money will be reinvested into marketing Kona, so while it might not immediately pop up on the bottom line, it should result in long term value creation by supporting Kona’s growth.

Operating leverage: Somewhat related to the cost cutting program above, but I think CBA has significant room for operating leverage as they continue to grow. I base this on two thoughts: Boston Beer’s operating structure and CBA’s costs over time.

Boston Beer Comparison: CBA is not Boston Beer / Sam Adams. Sam Adams has a better brand and is 4-5x the size of CBA. Even with that understood, it’s hard for me to look at SAM’s cost structure compared to CBA’s and think there’s not room for significant improvement. SAM is doing 50%+ gross margins and ~20% EBITDA margins versus CBA at ~30% GM and low single digit EBITDA margins.

Some of the difference is accounting driven (SAM seems to put distribution costs in SG&A versus BREW putting them into COGS), but the difference is still massive

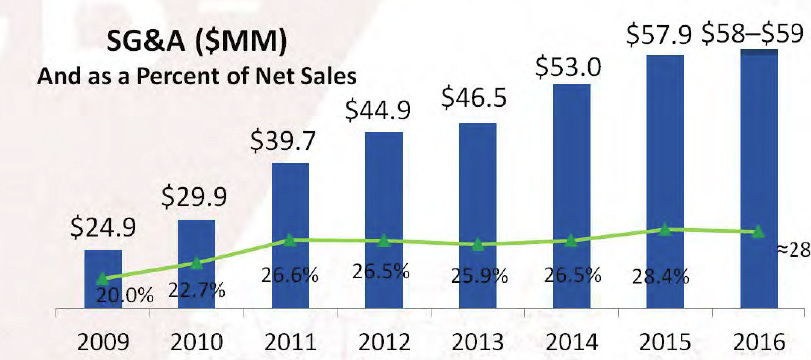

Costs over time: Since 2011, CBA has seen flat gross margins and increasing SG&A as a % of sales. Given sales have increased 50%+ over the same period, it’s pretty shocking they haven’t been able to get any boost over this time frame, even from just leveraging their public company costs and such. Some of this has been because they were increasing promotional spend to build the Kona brand, and some of it was probably due to simply not running a tight enough ship. Either way, I think the company has significant potential to realize operating leverage going forward now that Kona is the majority of their volume.

2017 will certainly be a bit of a messy year as the company begins to shift barrels from owned facilities to AB facilities (temporarily lowering utilization) and finishes up their capex projects. However, if we look forward to 2018, I think CBA’s inflection point will be completely visible. The cost cuts should have fully run through, Widmer / Red Hook will hopefully have bottomed out (and, even if they haven’t, they’ll be dwarfed by Kona assuming continued double digit growth), the international payments will be fully running through CBA’s income statement, and the cost savings from the 150k barrels that CBA will have shifted to AB facilities will be starting to kick in. Add it all up, and CBA could very easily be looking at $250m in revenue and $35m in EBITDA in 2018, with an outlook for continue strong growth as the company more fully penetrates international markets / improves growth margin. With today’s EV hovering under $300m and decent cash generation as the capex programs wind down and the AB international payments pop onto the balance sheet (the first payment was made in January 2017), and the stock looks pretty interesting /undervalued even absent the possibility of AB offer at a big premium.

Risks (aside from the accounting delay / other risks covered above)

Kona: To a large extent, an investment in CBA is a bet on the Kona brand’s ability to continue to grow into a national or even international brand. If Kona stalls out or shrinks (a la Widmer / Redhook over the past few years), AB is not going to be interested in buying the company at the prices discussed above, the economics of the company don’t really workout, and as a shareholder in general you’re not going to be happy. Obviously, anything can happen when it comes to consumer taste / preference, but I feel pretty good that Kona as a brand has staying power for a number of reasons:

Probably most important thing in thinking about the Kona brand and its potential / sustainability is the degree of faith AB is indicating in the Kona brand. AB is committing a lot of resources to CBA, and they’re clearly doing it with Kona in mind. No one has a crystal ball, but I would guess AB has a significant amount of data that suggests this brand has huge potential for them to put this level of resources into Kona.

This is more my subjective thoughts on the brand, but I do think Kona has all the makings of something that can sustain a large brand and a brand that can find international success. The brand has a clear play and feel (Hawaii / laid back paradise); it’s very similar to Corona in that way to me. Their main beer (longboard island lager) is a pretty light beer, so it can have a much wider appeal than a stout or ale or something.

Further backing up that the brand has something that appeals to consumers, Kona continues to grow pretty quickly, even as the overall craft market has slowed a bit.

I don’t put a ton of stock in these, but Kona has won a decent number of brewing awards, suggesting the beer is decent quality.

Lawsuit risk: Kona is getting sued by some consumers in California for not brewing Kona in Hawaii. I don’t think the case has any merit and doubt it’s a real risk; Beck’s is a $500m+ annual brand and settled a similar suit for $20m. I would guess Kona gets a significantly smaller settlement and it’s mainly covered by some form of insurance.

AB relationship: AB controls ~1/3 of the equity and distributes all of CBA’s beer domestically. Obviously any issues w/ AB could destroy the company.

Again, I’m comforted here by the AB contract. I don’t think AB puts that contract into place if they don’t plan on doing everything they can to help CBA grew.

It is worth noting that AB has a ton of outs that would preclude any activism going against their wishes (even if an activist can beat back a 33% equity owner). AB can cancel their distribution contract if any major decisions (i.e. a management change) are made against their wishes. So, like it or not, AB is in control of the company.

An interesting question: what would happen if AB decided they just wanted to make an offer for Kona (similarly to how they bought Goose a few years ago) and exit the rest of the company? The agreement, as far as I can tell, does not preclude AB from making an offer for a single brand. I don’t think the board would take that given the tax complications and that they could always just push AB to buying all of CBA and then disposing of the brands they don’t want, but it’s certainly worth thinking about how that could play out. Without Kona, this would be a super subscale company, so CBA would probably look to buy smaller brands with the cash proceeds, and I personally would not be thrilled with that outcome. Super tail-risk though.

Other brands: Widmer and Redhook have seen very aggressive and accelerating declines recently. If they continue to decline, the near term financials for CBA might not look great, as the brewery utilization would continue to decline and result in some operating deleveraging.

I said this in the article, but at this point Kona is >50% of CBA’s shipments. Assuming Kona continues to grow, it takes some pretty significant declines in the near term to cancel out Kona’s growth, and the two brands become a rounding error rather quickly after any more shipment drops.

Partnerships strategy: Outside of Kona, CBA’s strategy is to partner with local breweries and try to help them scale regionally; their Miami Craft Brewery deal is a good example of this (they also have deals w/ AMB in North Carolina and Cisco Brewers in New England). Finding partnerships isn’t a hugely risky strategy, but if they pick poorly it will cramp growth and could cost them some money. I think there’s a particular near term risk as CBA shifts some of their current brands to AB facilities as part of their new deal: if CBA can’t find partnerships to replace that capacity, CBA’s breweries are going to operate way below capacity and margins could suffer. It will also take some pretty significant partnership for CBA to make up for 300k barrels leaving their facilities for AB.

Capacity / utilization: Speaking of utilization, after the capex programs finish up, BREW will have >1.3m barrels of capacity. In addition, they can shift 300k barrels over to AB and save a significant amount of money in doing so. In 2016, the company shipped ~750k barrels. As that capacity comes on line and barrels are shifted to AB, utilization could really drop, which calls in to question if they can really get operating leverage and how the heck they can fill all this capacity.

Management has openly hinted that the solution here is to selling some of their older / less efficient breweries, so you’re taking on sale / pricing risk if they follow through on that. If they don’t, utilization and margins will be subpar until they can figure out a way to grow into their footprint.

Marijuana: Management called out on their most recent calls that they think increasing marijuana legalization is stealing some demand from beer. I understand that can sound silly, but I can definitely picture a few marginal users switching from an after work beer to after work weed as marijuana continues to gain acceptance.

I think CBA / Kona would do well regardless of the status of nationwide marijuana legalization, but I also don’t think legalizing weed is a high priority for the Trump administration.

Odds and ends

Sale synergies: I think the synergies in a sale to AB would be massive. CBA paid their top 5 execs ~$3m in comp in 2015; I estimate they spend between $1-2m on board costs (7 directors @ ~$80k/year each), audit costs ($300k+ annually), and other publicly company costs, so you could pretty quickly see AB rip out $5m of overhead on day 1 of buying CBA. The EV of CBA is ~$500m at the high end of AB’s offer price structure, so $5m in annually costs is relatively meaningful.

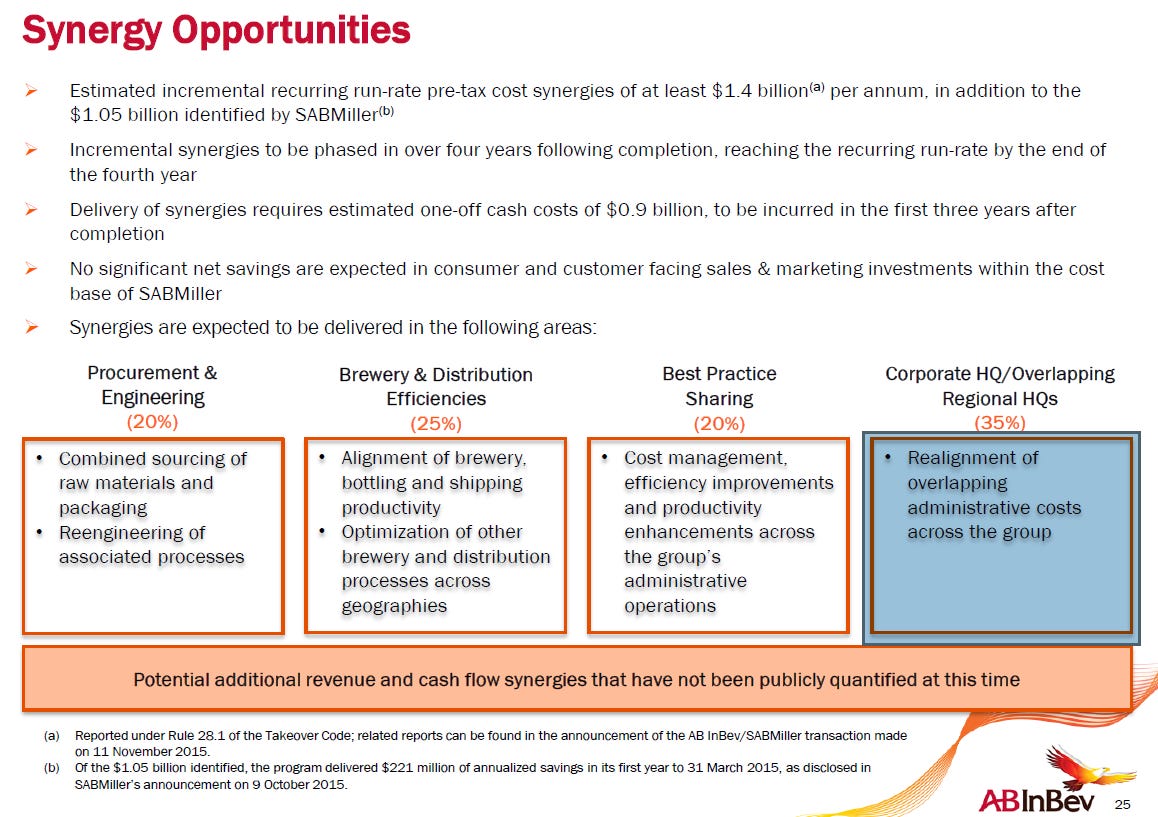

AB forecasted >$2.5B in annual cost synergies in their purchase of SAB Miller. Synergies were pretty evenly split between 4 buckets (See slide below). That’s ~15% on SAB’s annual sales. We’re comparing apples to oranges when talking about a bolt on like CBA versus a global mega merger like SAB, but I would guess the synergies from buying CBA would actually come out higher as a % than for SAB. If AB can get just 10% of sales as synergies, that’s another $20m in annual EBITDA at today’s sales levels; again, pretty significant versus a ~$500m EV at the high end of AB’s purchase structure.

Excise Tax Cut- The house recently introduced a bill that would slightly cut excise taxes on beer shipments. Not a huge needle mover, and a bulk of the benefits from the tax cuts would probably be competed away, but an incremental positive if passed.

Per the 10-k (see p. 12), “In January 2017, the Craft Beverage Modernization and Tax Reform Act (S.236/H.R. 747) was introduced in both the U.S. Senate and the U.S. House of Representatives. If enacted, the act would provide significant tax relief to all brewers and importers. Our benefit would be significant because it would reduce the excise tax from $7 to $3.50 per barrel on the first 60,000 barrels shipped and from $18 to $16 per barrel shipped on the next 6 million barrels shipped.”

Standalone value: Just building a bit more on the standalone valuation I worked around at the end of the article.

It’s a tough exercise as it’s very dependent on if Kona can keep growing (and at what pace) and where the other brands bottom out.

Again, CBA is not SAM and doesn’t have anywhere near Sam’s margins, but SAM is probably the best comp on the public market.

SAM trades for ~2x sales and 11-12x EBITDA. Sam saw mid-single digit declines in shipments and depletions in FY16 and has guided for low to mid-single digit declines in 2017, so you’d have to balance Sam’s better economics / significantly higher margins against the fact that their brands seem pretty maxed out and Kona could have a long runway for growth ahead of it.

At 2x sales, CBA would be worth ~$19/share.

At 12x LTM EBITDA of ~$12.5m, you’d be looking at a high single digit stock price. I obviously think that’s too draconian; if you used my $35m in 2018E EBITDA, you’d be talking about ~$17/share even before adding in the onetime international payments (which significantly lower EV).

CBA will never quite approach SAM’s margins for a variety of reasons, including that CBA operates their own brew pubs and serves food, a much lower margin business than selling beer.

Cash flow: Cash flow right now doesn’t look great; the company is doing ~$13m/year in EBITDA and spending ~$20m in capex, not to mention taxes, interest, etc. However, I think that’s a bit misleading. The company should wrap up their Portland and Hawaii expansions this year / early next, and once they’re finished capex should come down substantially. There also shouldn’t be any need for more big capex projects given the AB brewing agreement frees up 300k barrels annually (>20% of CBA’s capacity). Once the expansion is over, CBA should be a pretty nice cash flow generator: management has guided to ~$3m in annual maintenance capex. I think that might be a bit aggressive, but if you use my ~$35m 2018E EBITDA, and an MCX anywhere close to that $3m level, the company could easily throw of $20-25m in annual FCF.

Someone else buys them: I’ve suggested throughout the article that AB is the only acquirer. That’s not quite true; if AB decides not to buy CBA, CBA can sell themselves to someone else provided it’s not a strategic competitor of AB. If CBA sells themselves w/o an AB buyout offer, AB needs to abide by the current distribution agreement and let CBA keep all of the upfront payments. That could make CBA interesting to a private equity acquirer looking to roll up the craft industry at some point.

Here’s a nice Bloomberg Gadfly article on SAM’s weak Q3 earnings that walks through several potential acquirers and why they’d be interested; the same math would apply to CBA though the AB deal obviously makes that complicated. Speaking of Bloomberg Gadfly, here’s an article on the CBA / AB deal that walks through a lot of the acquisition rationale, and an older article that discusses Big Beer’s interest in buying craft brewers.

PP&E protection: Even if Kona completely blew up, I do think there would be some asset protection on the downside from all of Kona’s breweries. If you look at the expansion costs for Kona’s recently announced expansions, it looks like the capex costs to add one barrel of capacity are ~$80/barrel. I would guess the cost to new build a brewery is even higher than that. CBA will have 1.35m barrels of capacity after the expansions come online this year; if we just assume those are worth $100/barrel the breweries alone would be worth ~$5/share + all of CBA’s debt. Obviously it wouldn’t be fun to visit that price from today’s levels, but it gives CBA no value for anything else they own (like their brands) and suggests pretty decent downside coverage if things go horribly wrong here.

Insider buying: FWIW, there was a small bit of insider buying from the VP of Emerging Business this month in the $13.50 range. Obviously not a massive amount, but he’s been an officer since 2014 (and appears to have been involved in predecessor companies in some form dating back to 2005) and this is the first time he’s ever bought shares.