Comcast and the "curse" of "diversified holdings" companies $CMCSA

I was swapping thoughts back and forth with a few people on Comcast (disclosure: long) and the cable industry in general last night and thought I'd put some pen to paper.

The reason for the "thought swap" was (obviously) Comcast's recent bid to buy Sky, which is what I want to focus on here (I'll give some thoughts on Comcast's valuation at the end of this post if you're interested). The market reaction to the Sky bid has been awful: Comcast's shares were immediately down >5% on news of the bid, have declined >10% in the past month (and taken most of the cable sector down with it), and analysts and investors have been rushing to criticize / downgrade the company. The reaction certainly makes sense: investors wanted to see Comcast increase its leverage by increasing share buybacks, not take on debt to diversify out of their cable business and into a European satellite business. You can tell management was ready for this criticism: their 19 page acquisition deck included three "trust us; we have a good track record" slides (slides 14-16), and management has responded to the criticism by saying (this is my summary of their words) "you doubted us when we bought AT&T broadband and you doubted us when we bought NBC; both of those turned out great so trust us here".

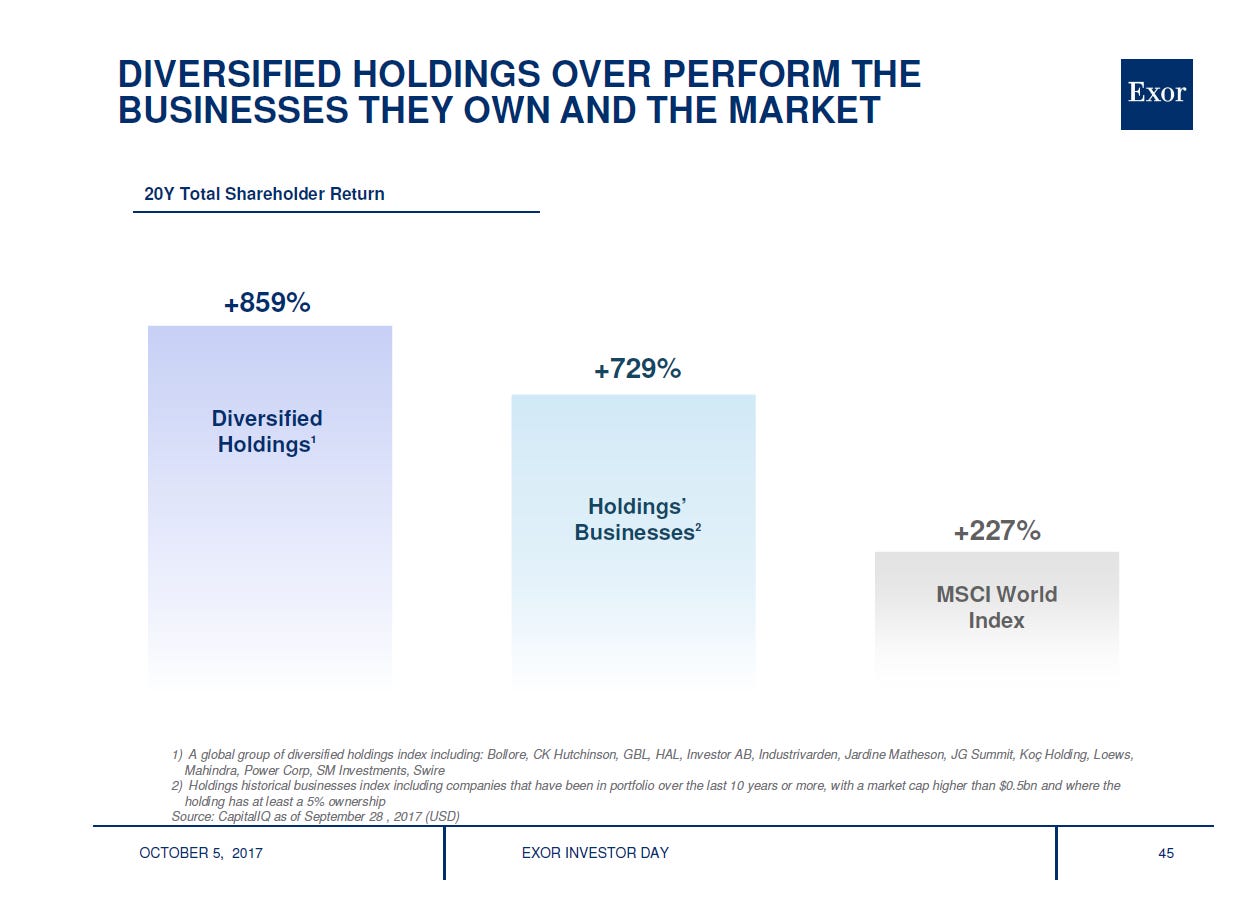

As I read CMCSA’s arguments for why buying SKY made sense, I couldn't help but thinking of the Exor (disclosure: long) investor day. Slide 45 of their deck (plus a small supplemental deck) showed how companies owned by “diversified holdings’” companies tend to outperform markets over time, and the diversified holdings companies themselves tend to outperform their own holdings.

Most of the peers on that slide tend to follow a broadly similar strategy: long term holdings of above average business combined with conservative debt levels. And this strategy isn’t completely unique to those holding companies: this Economist article (which Exor owns) mentions a bunch of controlled companies (including EXOR and Berkshire) and dives into how family-controlled companies tend to take longer term views of businesses, run with lower than average leverage, and outperform over time.

Anyway, you can probably tell where I’m going with this. Most investors (including me!) would prefer Comcast take their leverage levels up from their laughably low current levels (~2.2x) and use the proceeds to repurchase shares. Most of us see the Sky transaction as a distraction at best and a stepping stone to a value destructive overbid for Fox at worst. Those concerns are all real. But both Comcast’s business profile and their track record puts them squarely into the “Diversified Holdings” category (yes, they don't fit the exact definition, but I think they 100% fit the spirit / profile of one), and given the track record I’d guess it’s pretty unlikely they’d ever pursue an acquisition that actually resulted in a long term 10%+ hit to shareholder value (which is what the market is pricing in currently).

You’ll note I titled this post “the curse of the diversified holdings company”. Why is that? Because it probably would be better for Comcast to drop the Sky bid and just pursue a levered buyback strategy (a la Charter, which I am long). Heck, Comcast management likes to point to the success of the NBC acquisition, but if you compare the NBC deal to the opportunity cost of pursuing a levered buyback of Comcast shares over the past decade the NBC acquisition was probably a dud. But part of what makes “diversified holdings” companies great over the long term seems to be their conservatism (their lack of leverage leads to fewer blow ups, and their long term vision makes them the buyer of choice for family sellers who are willing to sell at lower multiples to avoid having their company dismantled for a quick buck), and that conservatism does not mesh well with a levered buyback strategy. So the funny thing is that the very thing that would make these companies so attractive for a levered buyback strategy (great assets sold to them at nice prices) is also the thing that keeps them from pursuing “optimal” strategies that could juice returns. It makes you appreciate the beauty / genius of Berkshire a bit more: the company clearly could have done better with a bit more leverage over its history, but taking on more debt might have kept Buffett from getting his “conservative” reputation and may have prevented him from getting some of the really cheap deals from family sellers (or the "buyer of last resort" deals during the financial crisis).

Other odds and ends

It is crazy to me how much market value Comcast has lost for this Sky bid. Comcast is offering to buy Sky for ~$41B EV, which comes out to ~$6B more than Fox was offering and ~$16B more than SKY was trading for before Fox made a bid for them way back in December 2016. With CMCSA shares down >10% since the bid, the market has knocked >$20B off of Comcast’s market value. So the market is basically saying that by offering to buy Sky, a business that Disney said was “a real crown jewel”, for a bit more than 12x EBITDA, Comcast’s capital allocation has gotten so out of control that they need to discount not just Comcast overpaying for Sky but a continued future of poor capital allocation at Comcast. Count me a skeptic on that bet.

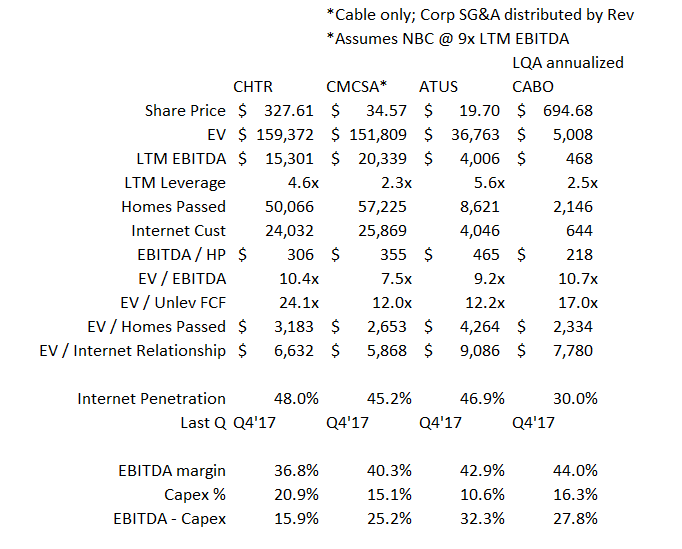

Why buy Comcast today? Because it’s probably the cheapest of the cable companies despite having the most scale, the most evolved wireless strategy, some of the best assets, etc. To put it in perspective, Comcast’s cable business, which is ~25% bigger than Charter’s, is currently selling for less than Charter. There are a lot of assumptions in here (assuming NBC is worth 9x EBITDA, not giving Charter value for their NOLs, etc.), but they’re not big enough to swing the core takeaway (that the market is seriously discounting Comcast).

The chart above does not add back the ~$500m Comcast has lost investing in the wireless business over the past twelve months (I simply allocates the losses by revenue as part of SG&A spend). Those losses will get worse before they get better, and Comcast is not alone in prepping to spend significant amounts on wireless. Charter will start that investment in the middle of this year, and Altice will begin their wireless strategy sometime in 2019. Given cable’s infrastructure advantage and the track records of the parties making the wireless investment, I’d guess the wireless investments are NPV positive for all of them, but given Comcast’s scale and that they’ll be starting quicker I’d guess Comcast’s investment has better returns than Charter’s and both of them have significantly better returns than Altice’s.

While we’re on Altice, I’ve talked to quite a few people about ATUS as we head into their share spin / big dividend. It’s definitely an interesting set up: given their high leverage and low capex, on a cash flow to equity story Altice is crazy cheap. And the combo of a nice share repurchase, a big dividend, and a huge distribution of shares in kind to Altice NV shareholders (forced selling? Sloppy trading?) makes for a really interesting event story. Still, I’m not sure it’s sustainable for Altice to run margins this high and capex this low (remember, Altice USA’s model is based on following the Altice Europe blueprint, and Altice Europe sort of blew up last year) , and I figure in the long run I’ll win either way by investing in Charter. If it turns out Altice’s model is sustainable, then Altice will buy Charter for a premium and realize a ton of synergies. If it turns out the Altice model is not sustainable, Charter will buy Altice in distress at some point in the future. Win/win.