Now could be the time to tune into $MSGN

I’ve mentioned MSGN (disclosure: long) a few times on this blog (here and here); I did a fuller write up in the wake of sports betting legalization and thought I'd share it here as well. Enjoy!

On Monday, the Supreme Court struck down a law that banned commercial sports betting. MSG Networks (MSGN; disclosure: long) will almost certainly be an outsized beneficiary of the ruling; in many ways, I think MSGN may be the best public market play on the rise of domestic sports betting.

MSGN was written up on VIC in early 2016 and is likely familiar to most readers who have spent time in the NYC area, so I won’t spend a ton of time covering the basics but I will provide a quick overview. MSGN is a regional sports network in the NY area whose key assets include the local broadcast rights to the New York Knicks (basketball) and New York Rangers (hockey) for the next 15+ years.

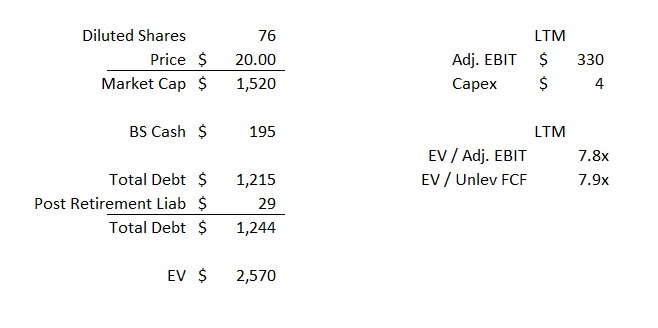

Even before factoring in the sports gambling upside, I think MSGN is likely undervalued. The company trades for just ~8x EV / EBITDA (which basically equals EV / Unlevered Cash flow given de minimis capex needs). With a high debt load and low interest rates (~3% interest rate), the after tax cash flow to equity is ~14% (~7x multiple) using a 21% tax rate (note: I’ve excluded stock comp, which runs ~$10m/year and is way too high; you can subtract if you want but I figured it wasn’t worth splitting hairs over).

Why is the market selling MSGN so cheaply? There are five key reasons

Cable bundle fears: anyone who is invested in any legacy TV network / cable company is well aware of the cord cutting fears, and MSGN has not been immune to those worries / issues as their subscriber base continues to decline at a low single digit rate (this article, while focused on ESPN, not RSNs, provides a good way of thinking about a lot of the issues).

This fear has a particularly interesting twist for RSNs and sports networks (like ESPN). RSNs are some of the highest priced channels in the bundle, and there’s an ongoing debate over whether the sports networks over-earn in the bundle or hold the bundle together. If RSNs over earn, the bundle collapsing will be a disaster for them / skinny bundles without sports like AT&T’s soon to release $15 service should take share rapidly.

Deal renewal overhang- somewhat related to the above, just about every year MSG Networks has one of their major affiliate deals up for renewal, and investors perpetually fret that MSGN will get blacked out when their deal comes up (they were blacked out in 2012). While the company doesn’t make it easy to tell, it appears their next renewal is with Charter at the end of this year.

Current results weak: both the Knicks and Rangers failed to make the playoffs this year, resulting in weak ratings, advertising make wholes (giving free ads to advertisers to make them whole for low ratings), and a tough comp versus last year (when the Rangers made the playoffs).

Failed sale process: MSGN was clearly spun off to be sold to a larger player, and the rumor is they tried to find a buyer last year and failed. (this article contains plenty of interesting tidbits as well)

Dolan Discount: This guy (who once had an article calling him the dumbest owner in sports) is MSGN’s chairman / controlling shareholder.

While all of these fears are real, I think they all tend to be overblown and more than factored in to today’s price. Just addressing the fears in order

Cable bundle fears- Cable bundle fears are real, but I think owning the rights to local sports teams will continue to retain overwhelming value. RSNs continue to deliver strong ratings, and ultimately people will want to watch their local teams and MSGN will find a way to monetize that viewership.

Deal renewal overhang- The 2012 blackout occurred in a much different era. Blackouts are rare (as Judge Leon said in the TWX / T case, negations are like a kabuki dance where everyone threatens to go dark but rarely does), and MSGN’s markets give them an even better chance of avoiding blackout than a traditional cable channel. Thanks to FIOS, most MSGN customers now have multiple cable/broadband choices, so a MSGN blackout could see fans quickly flea their cable provider for a competitor where they can watch games. When a subscriber switches providers, the cable company that blacked MSGN out would lose not just a video customer but a high margin broadband subscriber. That’s not to say MSGN can’t get blacked out; just that they’re in a better position than most RSNs (or cable channels in general) since so many of their customers can switch so quickly / easily in a black out. In addition, MSGN’s next renewal appears to be with Charter, and the ties between Charter / MSGN run deep: Charter’s executive roster is littered with people with ties to MSG and the Dolan’s (though their CEO’s departure was a bit rocky), Charter invested in the Dolan’s TV measurement firm, and Charter has sponsorship deals all over Madison Square Garden itself (which would make for an awkward brand image in a blackout). Given the strong ties between the companies and the competitive NYC market, I doubt Charter is going to black MSGN out (plus, given Charter’s regulatory issues in NY, I doubt they want the further negative press that would come with a black out).

Current results weak- I actually think this is an opportunity, not a risk. Current results are likely at a trough. Both the Rangers and the Knicks have some promising young players and assets; once they return to the playoffs ratings and advertising dollars should pick up nicely.

The Knicks in particular present a lot of upside; they’ll likely be awful next season given how much time Porzingis will miss, but they have a promising new coach, some interesting young players, all of their picks going forward, and a lot of salary cap space as the awful Phil Jackson contracts roll off. While the recent past and near term outlook is dark, I think they could build a strong contender in the next two or three seasons, and given how awful the team has been for the past decade local ratings would likely skyrocket if the team could put together one good season.

Failed sale process: MSGN is a nice asset, but the media landscape is in wild flux and all of the most likely buyers are engaged in more pressing deal (TWX / T trying to close, CMCSA / DIS / FOX bidding war, etc.). Once the landscape is a bit more settled, I think a variety of strategic buyers would be interested in buying MSGN. I’d note that the “failed” process occurred last year when the tax rate was still 35% (very meaningful for a super cash generative domestic business like MSGN) and FOX said DIS is valuing their RSN’s at ~12.5x earnings versus MSGN’s current ~8x multiple.

There would be decent synergies to a larger player buying MSGN. Revenue synergies from more negotiating leverage w/ cable providers, synergies from firing the wildly overpaid board / Dolan family, operating synergies from sharing DTC tech (I think the future is going to be RSNs going DTC, and if you own 10 RSNs you can leverage the same tech / app across each of them).

Dolan discount- Dolan may be “an awful rude bully”, but if you look at his capital allocation and deal history over the past ten years, he’s been somewhere between competent to solid (all the MSG spins, selling Cablevision at a nice price (here’s a bit more on that deal), selling Fuse right before the wheels came off pay TV) and I ultimately think he’ll maximize value for shareholders.

Note the Dolan family owns >15m shares (James has ~3.6m), so you’d hope the family is relatively incentivized to maximize value here.

I’m happy to address any other aspects of MSGN’s valuation or the issues facing them in the comments, but I want to focus a bit more on the sports betting angle because I think it’s so unique / under discussed. I would guess most commentary / questions would focus on cord cutting, and I’d note that there’s been a lot of discussion that topic in the cable company (particularly Charter) and TV Network (CBS) threads, so I’d encourage you to look at those for background as well.

Basics out of the way, let’s discuss sports betting and why I think it’ll be so beneficial to MSGN specifically.

Sports betting in general should be a boon for all sports broadcasts. The benefits will come in two different forms: engagement/ratings and advertising

Engagement / ratings: It’s human nature: you care more about a game when you have something personal on the line, and sports betting lets you have a vested interest in every game. It’s tough to exactly quantify how much legalized sports betting will improve ratings, but it’s likely to have a significant boost (FWIW, here’s a Nielsen study commissioned by the American Gaming Association that suggested the NFL would see a >30% boost in viewers). Improved ratings will drive increased advertising revenue in the short term (more eyeballs = higher ad rates) and improved carriage fees in the long term (more leverage when negotiating new deals).

Advertising: Sports books are going to be huge new advertisers as they get up and running. In Britain, sports books plow 20-30% of revenue back into advertising (mainly on TV). MSGN will obviously be a huge beneficiary of this ad stream (the easiest way to reach potential sports bettors is to advertise to people who watch sports, and really the only way to do that for Knicks / Rangers fans is through MSGN). However, I think this simple analysis significantly understates how big the near term opportunity is going to be for MSGN. First, because sports betting will be legalized at the state level, advertising at the local / regional level is the best way to reach potential new bettors, so a disproportionate amount of that advertising revenue should go to RSNs like MSGN. Second, British sports books are spending 20-30% of revenue on advertising in a market that is already relatively saturated. The U.S. market will be greenfield (i.e. customers will have no existing sportsbooks / habits), and sports books will be spending like crazy to reach new customers / have the customers place their first bet (and establish their first relationship) with them versus some other book. Remember the FanDuel / DraftKings crazy advertising blitz a few years back, where almost every commercial during football season was for one of those sites as they tried to grab new users? That was for a business model less proven and less profitable than sports betting. The potential land grab for new sports bettors could result in a huge spike in MSGN’s near term financials, and long term rates will likely settle much higher than today’s levels.

Bottom line: I think sports betting will be a bonanza for MSGN, as it will drive higher ratings and sharply higher advertising rates, particularly in the near term. And the great thing about MSGN is that, of all the RSNs, they are uniquely positioned to take advantage of the sports betting boom. MSGN is widely distributed in New York, New Jersey, and Connecticut, as well as parts of Pennsylvania. Those four states are some of the farthest along in terms of legalizing sports betting, which means MSGN’s sports betting “payoff” should be much quicker than most other RSNs.

There are also some “blue sky” scenarios where sports betting results in MSGN being worth multiples of today’s prices. A lot of that would depend on how far the league lets RSNs and sports teams get embedded with sports betting. For example, will leagues let sports books be the presenting sponsors of games (similar how to how Ford sponsors the Fox NFL Sunday show; could MSGN have “the Knicks brought to you by sportsbetting.com”?)? Would a league be ok with an RSN airing a gambling focused broadcast (similar to MSGN’s DraftKings Fantasy broadcast early this year)? The farther the leagues let sports betting “infiltrate” broadcasts, the more advertising money that will be up for grabs for the RSNs.

The biggest blue sky scenario would be if MSGN is allowed to integrate sports betting directly into their direct to consumer (DTC) app. The product / integration would look something like this: MSGN would take MSG GO, their consumer app, and add sports betting functionality so that you could place wagers in real time while watching the game without switching to a separate sports book app. Whether MSGN owns the sports book themselves or simply takes a cut from a sports book that they allow to integrate into their app, that product would take huge share and the revenues from it would almost certainly dwarf advertising revenues in the medium term. There are a lot of questions here (particularly around if leagues would allow such tight integration between their broadcast and gambling), but obviously any type of integration would have insane upside for MSGN as it would be near pure profit that I haven’t seen anyone account for when thinking about MSGN long term.

Maybe that type of integration is a dream scenario. But I think it illustrates a key point: MSGN owns the rights to local viewership, and over time more and more of that viewership will likely be through a DTC app that MSGN controls. Sports gambling makes that type of DTC control even more valuable, and at ~8x trailing earnings (i.e. earnings without any sports gambling factored in) the market currently has factored in precisely zero impact from sports gambling or MSGN’s brightened LT outlook.

Some other odds and ends

Sports betting was just approved a few days ago, so the end result is still up in flux and dependent on both league regulations (like the ones mentioned above on how deep they let RSNs integrate with sports books) and state regulation (what if a state allows sports betting but bans advertising? Will states allow all sports betting or restrict it to certain types (i.e. you can bet on game outcomes but not on individual play outcomes)). There’s also the question of timing (I think most of the northeast will have this legalized in some form in the next year, but gambling can be politically sensitive and maybe it drags a bit longer than that). All of those are good concerns / interesting questions, but no matter how this plays out, sports betting is going to be good for MSGN (even in the unlikely event sports betting advertising were banned completely, you would still see a tick up in engagement and ratings for MSGN, and I’d guess sports books would pay MSGN something just to get some type of access to their customer data on the backend) and, at today’s prices of 7-8x LTM earnings, you’re paying nothing (or less than nothing) for any sports betting type bump for MSGN.

Again, one of the coolest things about the “sports betting upside” angle is no one knows how it will play out or even how large the potential upside is. I’ve seen estimates that the “underground” gambling economy is currently ~$200B. However, as gambling becomes more main-stream (both in terms of legality and ease to execute), I’d expect that figure to balloon. Right now most people bet on who will win a game (i.e. I think the Knicks will win). As sports gambling gets fully up and running you’ll be able to bet on the results of each play (will the Knicks score on this possession? Will Kristaps hit his next free throw?), and I’d guess that results in higher dollar figures gambled. I’d also guess that those type of “next possession” bets carry higher margin and are much easier to do on the platform you watch (i.e. connected to the game broadcast on MSG GO), which should create huge value for MSGN specifically. It’s difficult to pin down an exact number for how big this will be, but I’d point to how big micro-transactions have been for gaming and other social apps (Tinder) as an example of how popular and large tiny, immediate bets and transactions can get.

Per MSGN’s 10-K, a significant portion of viewers are age 25-54 with high household incomes (exactly who sports betting companies will want to reach).

I danced around it in the write up, but MSGN is a huge beneficiary of tax reform. This is a high margin U.S. exclusive business that paid a full tax rate; the combination of deleveraging + their tax rate dropping is going to drive huge FCF expansion going forward.

MSGN has a $150m stock repurchase program, which would let them buy ~10% of shares at today’s prices. They have yet to act on it (as of the end of Q3), but based on their language on the conference call it sounds like they’ve gotten active in Q4.

MSGN is likely paying in the low $100m/annual range for their Knicks distribution rights and <$40m/annually for their Rangers distribution rights (at spin, they paid $100m and $30m, respectively, and that went up every year). Given the Charlotte Hornets just signed a deal that paid them ~$25m/year for their local rights, and that Charlotte is…. Quite a bit smaller than the New York market, MSGN’s rights are probably significantly underpriced / a big asset for MSGN.

I’ve focused on the Knicks and Rangers distribution rights, but MSGN has a variety of other (mainly hockey) teams: the Sabres, the Devils, and the Islanders. That is a lot of live content that is locked up long term at rates that didn’t factor in sports betting (either from an in-app standpoint or from an advertising standpoint).

The most likely acquirers are probably your big traditional media companies with lots of RSNs (Comcast, Disney after they buy Fox, AT&T), but there are some other options. Disney could be forced to divest the Fox RSNs to compete the Fox deal; in that case, the Fox RSN spinco could be a buyer of MSGN to continue to gain scale. Facebook, Amazon, and Google have all shown an appetite to get involved with live sports. While they’ll probably lean more towards national deals, given the size of the New York market I could see any of them talking themselves into buying MSGN to bundle local rights and lure North East consumers into their respective bundles (the amount of data all of them have would also allow them to monetize these games like crazy).

An interesting thought on MSGN’s potential strategic value- if MSGN is early to integrating gambling into their DTC app, an acquisition of MSGN by a larger player with RSNs is no longer simply about cost synergies; it’s also about buying technology that they can immediately roll out to their other RSNs as gambling becomes legal / mainstream in their other markets.

James Dolan is currently going through a divorce, and there’s always rumors that he could look to take MSG (disclosure: long) private. I know a lot of people who think a sale of MSGN would help with both of those (make the estate easier to split in the divorce or help fund an MSG go private bid), though I don’t put much stock into either of those as catalysts.

“The NBA is hot”. The league is extremely well positioned for the digital age (it is flat out crazy they’re posting ratings increases given almost everything other form of entertainment is posting significant ratings declines) and given the majority of MSGN’s value comes from their Knicks’ rights, MSGN is well positioned as well. I’d also note that the NBA has probably been the most forward thinking and open to legalized sports betting, which suggests they’ll be more open to deeper sportsbook / RSN “integration”.