$NRE: Limited Downside, Decent Upside, Tight Time Frame

I love to read. And, as a semi-avid reader (my level of reading tends to ebb and flow inversely with how much time I’m spending working; over the past few months I’ve found myself tilting harder to work than reading), I’ve thought a lot about writing a book. Because most of my reading time is spent reading fantasy (probably not a surprise given I have an entire series devoted to interesting worldbuilding IP!), my “daydream” of writing a novel generally focuses on writing a Game of Thrones-esque fantasy series.

But that’s really just a pipe dream; my day job takes up too much of my time to write a series of fantasy novels (and I like my job too much to take that much time off!). So, if I ever do write a book, it will (unfortunately) be yet another finance / investing book, not a fantasy novel. I think the structure of the finance book would look something like this: each chapter would start with an overview of a different investment type (i.e. a spin-off, a share cannibal, a net-net, an activist candidate, etc.)). After a quick overview of what the investment type is and why it’s potentially attractive, the chapter would quickly shift to a historical case study of a successful example. I think the twist I’d put on the structure is the case study would have a heavy emphasis on links to SEC filings from the time of the case so readers could “recreate” the investment and the thought process behind it if they wanted to. I am aware that showing a successful example introduces strong “survivorship bias” type risk (i.e. it’s possible the category as a whole is unattractive and I’m simply cherry picking one successful example), but I still think this case study driven type book would be the best type of book for somewhat experienced investors who are looking to get better (which is who I would be targeting; I don’t plan on writing yet another intro to value investing book).

Why do I mention this (purely theoretical) book idea? Because every now and then when I stumble on an investment I think to myself “that is a perfect book case study”. And that’s exactly what I thought about when I stumbled on NRE (disclosure: long) earlier this year: NRE was the perfect example of how a change in management incentives could serve as a catalyst for value maximization. Unfortunately, that “incentive” story has largely played out at this point, but today NRE is probably the stock that offers the best combination of decent upside / limited downside / strong catalyst that I know of, so I figured I’d do a combination case study / current write up on NRE.

A quick overview of NRE heading into this year (you can find a bit more background in the 2015 VIC write up and the early 2018 write up). NRE was created in 2015 as a REIT focused on European prime office space. NRE was spun out from and externally managed by Northstar Finance, which did not have a great reputation (management was best known for maximizing their own fees / salaries, not creating shareholder value. The anecdote about the management team ordering leather swatches for their custom yachts while waiting on their deal to close should tell you all you need to know about where their real priorities were). In 2016, Colony Capital bought / merged with Northstar and became NRE’s new external manager (interestingly, Colony initially was not interested in buy Northstar as a whole but was instead focused on buying the NRE management contract (see p. 110), but eventually Colony decided to just full out merge with all of Northstar).

The Northstar / Colony merger has been, to put it kindly, a disaster for Colony and its shareholders. But it’s the perfect starting point for our NRE story, as the merger actually played a key role in helping to unlock NRE’s value. Northstar had spun NRE off with a management contract that was both onerous and effectively perpetual (you can see details of the contract on p. 122 of their 2016 10-k). On the heels of the Colony / Northstar merger, hedge fund Bow Street went public with an offer to buy NRE for $13/share and noted that the Colony / Northstar merger presented NRE with a unique opportunity to reject the management contract without paying any fees. Bow Street’s efforts were ultimately unsuccessful, and they ended up selling their ~8% stake in NRE to Colony for $12.75 in May 2017; however, even though Bow Street’s efforts were unsuccessful, I think they were an important piece to the story as Bow Street selling their stake to Colony meant, for the first time, NRE’s manager (Colony) had some equity “skin in the game”.

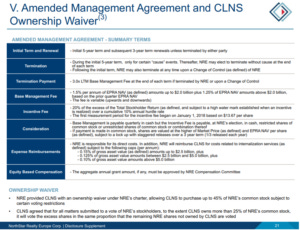

After Colony bought Bow Street’s stake, things started to change at NRE. First, Colony started to buy more shares on the open market. In late May, they bought another ~1.2% of NRE on the open market. The biggest change, however, happened in September 2017, when NRE announced they had changed their management agreement with Colony and given Colony a waiver to increase their share ownership in NRE. This was a huge move, as the new management agreement (I’ve screenshotted the highlights of it below, from NRE’s Q4’17 supplemental disclosure), while far from perfect, was decidedly more shareholder friendly than NRE’s previous agreement. Colony followed the new agreement up by immediately buying another ~1.2% of NRE on the open market.

In addition to the new management agreement, directors started to get awarded in RSUs that were subject to significant TSR hurdles (see footnote 3, “the restricted stock units will vest (i) at 25% of the target if the TSR from the grant date through February 28, 2021 equals 8% per year, compounded annually, or greater, (ii) at 100% of the target if the TSR during this period equals or exceeds 15% per year, compounded annually, or greater, and (iii) at 200% of the target if the TSR during this period is equal to 20% per year, compounded annually, or greater, with the amount vesting for performance between such hurdles based on linear interpolation. If earned, each restricted stock unit will be settled in shares of common stock of NRE”).

So, in the course of one year, NRE went from having a horrible external management contract and almost no “skin in the game” from their managers and directors to having a manager that had invested ~$70m into NRE’s equity and a management contract (plus director payouts) that heavily emphasized shareholder return.

Now the case study kicks in: what happens to a company when management goes from focused on driving fee streams to incentivized to boost the stock price?

NRE’s new management contract went into effect on January 1st, 2018 and gave the manager 20% of any shareholder return over NRE’s 1/1/18 stock price of $13.67. Assuming the company kept their $0.15/share quarterly dividend steady throughout the year, Colony would need NRE’s share price to end the year >$14.44 to start receiving incentive payments. NRE’s “ERPA NAV/share” (basically a fair valuation of their portfolio done by an independent auditor) at the start of the year was $19.85, so Colony had some fairly easy levers to pull to hit their TSR payouts: have NRE repurchase shares at a big discount to NAV until the market rewarded NRE. If the market wouldn’t respond to the first bit of share repurchases, sell some buildings at NAV and use the proceeds to buyback even more shares (this route has the added benefit of “proving” to the market that the NAV mark is good). As NRE’s largest shareholder, the repurchases benefit CLNY both because they boost the NAV/share of the remaining shares and because they make it more likely CLNY will get their TSR payout.

Sure enough, when NRE announced their Q4’17 results, they announced a $100m share repurchase plan (a significant amount given NRE’s ~$700m market cap at the time). And NRE was very aggressive in using the repurchase plan: from announcement in March through mid-May, NRE repurchased ~$45m in shares, and the company had gotten to over $80m in repurchases by the time they reported Q2 results. With the repurchase cost averaging <$14/share versus NAV of ~$20, these repurchases were crazy accretive for the remaining shares.

Anyway, that would be the overarching story for the case study. I’d probably build it out a little more by diving into NRE’s individual buildings, their history of selling buildings at or slight above NAV, and some other stuff (a lot of which you can find in this 13-D from September; the PR of the letter has some charts that are lost in the 13-D if you’re interested in them), but that’s the high level overview.

Let’s switch to the present day, and why I think NRE is so interesting now. I may be spiking the football at the one yard line here, but at this point the NRE case study has largely played out successfully. Along with their Q3’18 earnings, NRE announced they were selling their largest asset (Trianon Tower) at a price in-line with their NAV. The next day, NRE announced they were exploring strategic alternatives; importantly, this announcement included an agreed upon price to buy CLNY out of their management agreement.

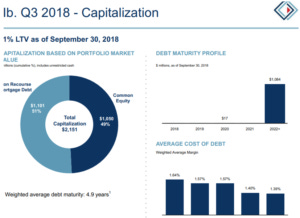

At today’s share price of ~$16/share, NRE is trading for ~77% of their Q3’18 NAV/share of $20.85. However, I don’t think that’s the right way to look at it. Selling Trianon will release ~$360m onto NRE’s balance sheet. While NRE has significant debt (~$1.1B at 9/30/18, though that will go down after Trianon is sold and its mortgage is paid down), all of that debt is non-recourse / property specific. That makes a huge difference: if the debt was recourse, small changes in NRE’s underlying building values could demolish NRE’s NAV and consume all of NRE's cash. However, because the debt is non-recourse, if one building is worth way less than NAV it will hurt NRE’s downside but not demolish the whole company / investment thesis (and the cash provides a significant downside cushion).

So I think the right way to look at NRE is to separate out their holdco cash and the NAV of their buildings. At 9/30/18, NRE had $61m in holdco cash. They’ll get another ~$360m once they sell Trianon, but they’ll also need to shell out ~$70m to get out of their CLNY contract (which will also knock ~$1.55/share off their NAV). So, post Trianon sale and CLNY payout, NRE will have ~$350m, or $7/share, in cash on their balance sheet and an NAV of ~$19.30. If we assume NRE is getting sold / liquidated in the near future, I think the right way to look at NRE is to assume that $7/share in cash is money good for shareholders; if we look through that NRE ex-cash is today trading for ~$9/share versus a ~$12.55/share NAV for P/NAV of ~71%.

Betting on the gap between NRE's share price and their NAV closing seems like a good bet to me. NRE has historically been very successful in selling buildings at or above NAV, and the prospect of closing that ~30% NAV gap in the next few months (on a successful strategic review) is pretty appealing. Plus, the downside seems pretty limited: at today’s share price of ~$16/share, you’re getting more than 40% of your investment in cash on NRE’s balance sheet. Of course, I’m advocating to look through that cash, but even looking through that you’re paying 70% of NAV and all of the debt is non-recourse, so if one or two buildings turn out to be worth below NAV things probably work out just fine. The manager is incentivized to sell NRE and has already agreed to be bought out of their management contract, so between management alignment and an activist with a 10% holding who wants this to be sold, I view this as a pretty low risk bet with decent upside and a tight time frame (the market for prime office buildings in developed countries is generally quite liquid, so we should know the results of the strategic review in a few months. The big question is probably if NRE sells the whole company to one buyer or sells the buildings one by one, but either way I think shareholders will make out well here).

One more thing before I wrap this post up, because I think it’s worth thinking about for every investment: why does this opportunity exist? NRE is a small cap (market cap ~$800m, free float ~$650m) REIT that is externally managed (by a manager who has been an absolute disaster). In addition, NRE is focused on European prime office buildings, but it trades in America. Mix all of that together and you get a really strange public company that probably has a very limited potential shareholder base. I’m not saying “European company on American exchange” is a recipe for mispricing in and of itself, but it certainly is a strange combo. Combine all of that with a rapidly shifting balance sheet (the non-recourse debt, the massive cash release from the Trianon Tower sale, the pending cash payment to CLNY to get out of the management contract) and I think it’s easy to see the potential for mispricing in NRE's shares.

(PS- As I wrapped this post up, Clarkstreet published some similar thoughts on NRE. Always worth checking his posts out!).

Risks

Trianon Tower deal falls through: A big piece of this thesis rests on the limited downside due to the cash from the sale of Trianon Tower. If that deal falls through, then obviously you get a bit more market risk.

Counterpoint: Trianon will almost certainly close (it’s scheduled to close before year end); even if it didn’t, we have an external mark that validates the NAV of Trianon, and NRE could just look to sell the Tower to another buyer at around the same price.

Currency: all of NRE’s buildings are located in Europe (post Trianon sale, ~35% of them will be marked in GBP, with the remainder marked in Euros), so you do get some currency risk given they trade in USD / mark their NAV in USD. Both the Euro and GBP have weakened a bit since their Q3’18 NAV was released, so there’s probably a little currency headwind currently but not enough to dramatically change anything. A huge drop is a risk though.

Brexit is a very related risk. ~35% of NRE's operating income post Trianon will come from England; I would venture that their 9/30/18 NAV mark incorporates the current thinking on Brexit but if Brexit turns into a complete disaster or the GBP falls significantly, Brexit could obviously hit NRE's NAV. Still, with NRE is trading at a ~30% discount to NAV (looking through the cash), and that wide of a gap can cover a lot of noise for their ~35% GBP exposure.

Strategic process fails: NRE could decide to cancel the strategic process and either maintain CLNY as their manager or go it alone as a standalone, internally managed European focused REIT. That would… not be ideal, though how much downside there would be from here is questionable given the nice discount to NAV.

The big question with this risk is what would happen to NRE's cash. Given how small they are, they would almost certainly chose to reinvest the cash and try to scale up a bit versus returning the cash to shareholders, so forgoing the strategic process would significantly alter the risk/reward here (and most likely not in a good way)

Still, I think this is a long shot risk. CLNY clearly wants the liquidity from this position, and there’s a 10% activist here too. If NRE wants to liquidate, they easily can, either by selling the whole portfolio or by selling the buildings one by one. If the desire is there, they’ll be able to do it.