Yet another guide to media stocks, Part 1b: broadcasters update $TGNA

Hi! Welcome to Part 1B of Yet Another Guide to media stocks. Today’s post will cover a brief update on the broadcasters, particularly Tegna (TGNA; disclosure: long). Before diving in, I’d highly encourage you to check out the intro section to the guide, which goes over why I’m doing this and dives into the most important thing hitting the media sector today: cord cutting. You can also find links to all of the pieces in this series here. The broadcasters were the first group I covered in the media series. Rereading that post, I'd say I was slightly bullish on the broadcasters. They were just so cheap.... but I couldn't pull the trigger on buying them because I was worried about terminal value issues (Modest proposal (frustratingly) summed up my worries quite well). In addition, I thought the opportunity costs for buying the broadcasters were kind of high: FOX and VIAC (the networks) were both trading at multiples similar to the broadcasters despite (IMO) much better businesses. To date, failing to buy the broadcasters has been a mistake; since my post, the broadcasters have all enjoyed quite a nice run, significantly outperforming both the networks and the overall market.

Generally, I try not to revisit themes and ideas too much on the blog (except for cable companies and sports team valuations; you're stuck with me ranting about those!). However, two things happened recently that made me want to revisit the broadcasters: CBS's (VIAC, disclosure: long) renewal with Comcast and activism at Tegna. Let's start with the simplest: the CBS / Comcast renewal. I want to focus particularly on the second paragraph of the renewal:

In addition, CBS All Access, CBS’ digital subscription video on-demand and live streaming service, will be available on Comcast’s Xfinity X1 and Flex platforms later this year. This will mark the first time CBS will make the CBS All Access app available on an MVPD-based set-top box.

Why do I care about that sentence? Well, it seems like that deal can easily be the start of CBS and Comcast edging out broadcasters in a variety of ways. The simplest way (though not the only way) would be to look at this through Comcast Flex. Flex is Comcast's service for cord cutters. If you get internet from Comcast, they'll give you Flex for free, and you can use it to subscribe to any streaming service you want (Netflix, Hulu, etc.). By using Flex, all your shows and bills will be in one place. Everyone wins: apps get access to all of Comcast's internet subs, Comcast keeps control of a customer and gets a cut of the billing, and the customer gets to access all of their shows in one place. The CBS / CMCSA new agreement puts All Access on Flex. Say you're Nexstar, and you own the local CBS affiliate in a Comcast market. I'm sure right now you'll get a cut of any sub who subscribes to CBS All Access through Flex (I don't know the specifics of the agreement and don't think it's been put out there, but I feel like the broadcasters would be absolutely rioting if Comcast was offering CBS All Access to customers in their local areas and the broadcasters weren't getting a cut, so it's probably safe to say they get a piece), but why should that be the case in the future? I mentioned this in the first part of the series, but right now broadcasters basically extract payments from distributors based on the strength of the network programming they get from their affiliate deal plus their local programming (mainly news). I'd argue the vast majority of broadcaster's value comes from the strength of their network programming and the legacy rules that prevent the networks from owning broadcasters across the whole country; it seems agreements like the CBS / Comcast deal are a stepping stone to cutting broadcasters out of the picture in the future. Anyway, I just wanted to highlight that because it seems to be such a clear stepping stone towards a network getting to a place where they can cut a broadcast affiliate out of a large piece of the pie. The other thing I wanted to mention in this update is the recent activism at Tegna (TGNA). I'll be upfront and note I have a small position, but it's still a work in progress and the position can get larger or smaller (or go away!) at any time! This week, Standard General went hostile looking to replace the board at TGNA. They own just shy of 10% (they first filed in October); in addition to Standard, we found out this week activist Donerail apparently owns just under 5% of Tegna. That's almost 15% of Tegna in the hands of activist investors that want it sold. That's a lot of pressure on the company. My belief is that pressure will likely lead to a sale of Tegna. We know that Apollo has previously approached Tegna, and Apollo just completed the purchase of Cox Media group in December. It seems pretty likely that if Tegna was up for sale, Apollo / Cox would be eager bidders.

PS, speaking of Apollo, I thought it was interesting that Tegna's CEO was willing to comment directly on Apollo's investment in Cox. Tegna made these comments at the DB conference in March 2019, so presumably this was after Apollo had approached Tegna.

It's tough to get a clean earnings number for Tegna. They did ~$705m in EBITDA in 2019, but their go forward earnings should be much higher for a few reasons.

2019 wasn't a political year. 2020 will be, and by all accounts it will be an enormous one. I spoke about this a bit in part one so I won't dive in further here, but the further into this cycle we go, the more robust political spending looks like its going to be, and Tegna seems to be one of the best positioned for how the political map is going to break.

Seriously, I think 2020 is going to be bonkers for political spend. I live in NYC, and the only live TV I've watched so far this year is the Saints loss to the Vikings (I don't want to talk about it) and the Tigers National Championship Game. I feel like I watched more Bloomberg commercials than actual football during those two games. Again, this is on national feeds in NYC. Imagine what the advertising in battleground states must be like.

Tegna completed ~$1.4B in acquisitions throughout the year ($110m in Toledo / Midland deal in January 2019, $740m Nexstar divest in September, and $550m Dispatch deal in August 2019). For a ~$8B EV company, that's a lot of deal making. Obviously the 2019 earnings number doesn't include the full runrate of those deals; in addition, their should be significant synergies from those deals that begin to bleed into Tegna's financials over the next year.

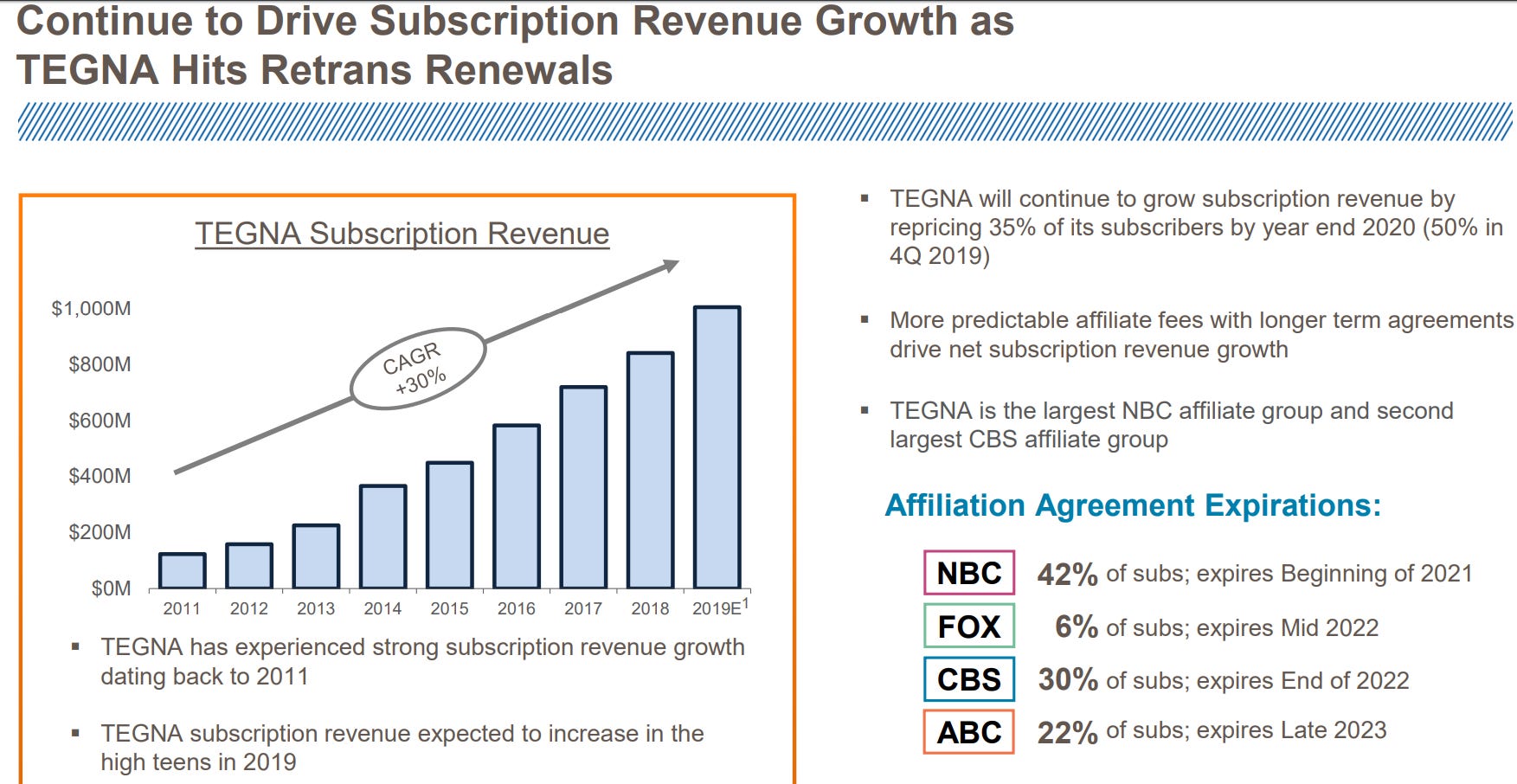

Speaking of synergies, tegna has a lot of distributor contracts expiring over the next year (per the January 2020 investor deck below, 35% of subs expire this year). Given Tegna's significantly larger size post all of those deals, Tegna should have some additional negotiating leverage in these deals, which should drive better pricing and earnings.

Anyway, most broadcasters trade on an average 2 year EBITDA multiple (so, take fiscal 2020 and 2021 and average the EBITDA over those two years) in order to adjust for the political / Olympic cycles. It's tough to get an exact earnings number for Tegna over 2020/2021 given how many moving parts there are here. My guess is EBITDA averages $950m/year over that time frame; I think that's directionally correct but you could add or subtract ~$40m in either direction and I probably couldn't argue with you. Anyway, we know average broadcaster M&A happens at a tough over 9x EBITDA. If Tegna got that multiple, shares would be worth ~$22/share in a takeout.

I actually think that might be a conservative takeout valuation for two reasons.

Tegna represents a one-stop shot to achieve huge scale. If you're Apollo, your Cox stations right now are probably subscale, and getting them to scale will take several deals over the next ~5 years. Buying Tegna represents the chance to achieve enormous scale in one shot instantly. That type of certainty of scale often commands a premium.

Somewhat related, when I look at the list of major broadcasters with scale similar to Tegna, Tegna appears to be the only one (potentially) available to buy. Being the only large, strategic player on the table available to buy often results in a nice premium.

Tegna (and all broadcasters) are cash flow monsters, and I'm using Q3'19 net debt numbers. By the time Tegna is actually put up for sale (say, over the summer this year), they'll have generated nine months worth of cash flow. That will be hundreds of millions of dollars; let's use $500m as a nice round number. That cash generation would represent an additional >$2/share of value, taking the take out price closer to $25/share.

There are a lot of different places I could cover here, but this is still a work in progress so I think I'm going to wrap it up here. My bottom line is that Tegna is in a consolidating industry and I think it's an extremely strategic piece that would command a nice premium. With 15% of shares in the hands of investors who will likely push for it to be sold, I think Tegna is likely to start a sale process at some point in the next few months. The process should lead to a sale at a nice premium to today's price. Odds and ends

I'll note again this is a work in progress. I've done a lot of work in the sector, and I've been through all of Tegna's earnings calls / 10-ks / etc in the past few days. So I'm not just some random guy talking here.... but I'm also far from an expert and I'm willing to admit that! If you've done work on the sector and feel like there's a place where my numbers or off or I'm just completely wrong, I'm very open to hearing them!

At today's prices, Tegna probably trades for a slight premium to Nexstar. Nexstar is a larger business (and scale is important in this industry) run by better operators and with a better capital allocation / M&A history. I feel a little strange buying Tegna over them, but I'm just convinced Tegna is going to be sold and they'll be sold for more than today's price. I'm worried about the terminal value for broadcasters; buying one that I think will be sold near term helps alleviate that concern somewhat.

I'm kicking myself I didn't buy Tegna as soon as Standard filed on it. Standard has invested in a broadcaster before through Media General. Their thesis at Media General was simple: participate in consolidation. It wasn't a super clean story (Standard backed a Media General / Meredith deal that was pretty ill received until Starboard got involved and eventually got Media General sold to Nexstar), but in the end shareholders who participated along with Standard in Media General did really well (their 13-D highlights this). It was pretty clear from the moment Standard filed that something was going to happen at Tegna.

One of Standard's complaints against Tegna is that Tegna is overpaying for M&A. I think that's probably fair; I don't think they've destroyed value through M&A, but I do think they've given up all of the value from synergies to the sellers. The Dispatch and Nexstar acquisitions from last year are probably good examples; Tegna paid just under 8x 2-year average EBITDA after synergies for both deals. That feels too high to me. Consider: Nexstar bought Tribune for 7.5x EBITDA after synergies. It seems like Tegna should be buying the divestiture from Nexstar / Tribune for a lower multiple than the actual deal itself as 1) Nexstar is a forced seller and 2) Nexstar combining with Tribune is much more strategic / synergistic than Tegna picking up some of the divestitures (again, larger deals in this space should have bigger synergies given increased negotiating leverage, so you can pay up a bit for larger deals).

Another interesting angle here is that, at some point, the national cap is likely to be lifted. If that happens, Tegna becomes an even more interesting acquisition piece. Say the cap was lifted to 60% of the national (or eliminated completely). You could suddenly have an arms race to beef up among the broadcasters.... and Tegna would be the largest target around that was a willing seller. That could drive a very active auction process for Tegna. Of course, the rumor the national cap will be lifted has been circulating for years, so maybe it just never happens... but I view it as a really strange piece of legacy regulation and I feel like it has to be changed at some point.