Lemonade: I don't get it $LMND

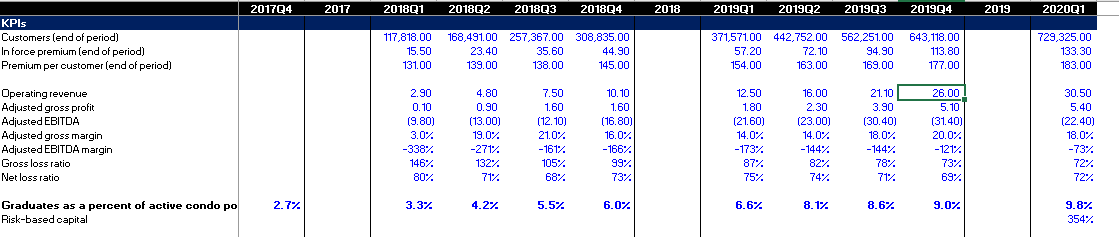

Back in 2012, Facebook bought Instagram for $1B. It's truly one of the greatest acquisitions of all time: today, Instagram is probably worth >200x what Facebook paid for it; in addition, buying Instagram destroyed a potential Facebook competitor, handicapped another (Twitter), and accelerated Facebook's mobile strategy. I'll always remember that deal because it marked an important turning point for me. I always considered myself a traditional deep value value investor (I got my start investing looking for Ben Graham style net-nets), and I generally joined along with my deep value brethren when they mocked companies like Amazon or Salesforce that traded for higher multiples of sales than the multiple of earnings of companies I was interested in (i.e. the tech high flyers traded for 15x sales and I wouldn't buy a company for more than 12x earnings). I was confident that momentum buyers today might enjoy those high flyers, but when the bubble burst I was confident my deep value peers and I would have the last laugh (How quaint! I wish I could go back then and enjoy the momentum buyers!). The instagram deal changed all that for me. Paying $1B for a company with no revenue and a handful of employees (I believe it was 33 employees when the deal was announced)? Insanity to my deep value investors, and I saw plenty of them mock the deal online (in fact, you can find articles of people questioning the deal even one year after Facebook made it!). I felt differently. Instagram was huge. All of my friends were on it and using it nonstop. Sure, revenue might have been zero on a trailing basis, but it would be so simple to put some ads into Instagram and once they did the revenues would be enormous. Yes, there's risk to any deal (particularly buying a social network that was still growing), but on a risk-adjusted basis I was pretty sure Facebook had just stolen Instagram even though they paid an enormous multiple to non-existent sales. Unfortunately, I never bought facebook stock or anything. But I'll always remember the Instagram deal fondly because it was my first step as an investor to realizing the power of scale economics for online platforms and that maybe (just maybe!) you could buy something that didn't look cheap on a trailing basis because the future was so bright. I know what you're thinking- cool story bro. What the heck does it have to do with title of this post, Lemonade? Well, one of my rules for both investing and this blog is not to take shots at new companies because I don't understand their valuation. Often, if the valuation of a tech company seems ridiculous to an outsider, it's because the outsider isn't looking at the possibility for a company once they scale or to a competitor with a ton of synergies (similar to how many deep value investors mocked the Facebook / Instagram acquisition). If I don't get the valuation, it's probably because I'm not thinking big enough about the risk/reward for a start up, not because the start up is overvalued. But Lemonade is different to me. I read the S-1 yesterday and then looked at the stock price and honestly thought I had read the wrong S-1 / looked at the wrong stock price. I guess I can see what the market is looking at: Lemonade is a fintech insurance company. The insurance market is huge and dominated by legacy players doing business the old school way (grabbing customers through advertising and/or networks of brokers compensated on commissions). If Lemonade can disrupt that model with a better / lower cost way of grabbing customers, the potential payoff is enormous. So, at it's best, I guess you could paint a picture of Lemonade as this generation's Geico: 50 years ago, Geico had an enormous moat because all of their competitors sold insurance through highly priced sales agents, while GEICO could offer a product that was both lower priced and more profitable by going direct to consumer and cutting out the expensive sales agent (Geico also benefited from positive selection bias because their original customer, government employees, were less likely than average to make claims). This mid-90s NYT article on Buffett buying the piece of GEICO he didn't already owns lays it out a bit more clearly: a sales agent generally costs >10% of auto insurance; GEICO could take the money they saved on an agent and use it to lower their price while also selecting only to sell to the lowest-risk, safest drivers. Lemonade could get something of that GEICO double play going at its best: leveraging their tech and avoiding the cost structure of their legacy peers would let them have a lower cost structure, while they could use their data to cherry pick the most profitable customers who are less likely to make a claim. Lemonade's better technology and superior user interface would result in happier customers, which would increase customer lifetime value (and improve odds Lemonade can upsell customers more products longer term). In addition, as a certified B Corp, Lemonade's might attract a more socially minded customer who might be less likely to make claims (similar to how Geico's government employee focus self selected customers less likely to make claims). So I get it. I can see the upside. Buying GEICO in the 70s is one of the best investments Buffett ever made. It's a career making investment. But it just seems so unlikely that Lemonade plays out like that. Start with the obvious: valuation. Post IPO, LMND's tangible book value is $10.33/share (and basically all of that is from the IPO; tangible book was negative $17.39 before the IPO). As I write this, LMND is trading for >$72/share, or ~7x tangible book value. Buffett bought into GEICO in the mid-70s when the company was in some temporary distress; I believe he bought for less than book value and around 5x earnings. LMND is.... not at 5x earnings. It's not at 5x revenue. Heck, it's not even at 50x revenue. (model below from Daloopa; you can find the full model here)

So, even if LMND follows the Geico path, that probably wouldn't be good enough to make a good return on your investment today. The share price is simply too high. Clearly, the market is pricing in LMND today as having a brighter future than Geico did ~40 years ago. In fact, the market is pricing LMND so brightly that they have to be valuing it as more than an insurance company; remember, insurance companies are regulated, so even if LMND is mammothly profitable their growth will be severely restricted by insurance regulations and capital requirements. LMND can somewhat skirt those requirements by using reinsurance (which they make liberal use of) and raising capital (they made liberal use of that with their IPO, and I suspect they will continue to do so), but still: their growth as an insurance company will be constrained by capital, and at today's pricing the market is certainly not pricing in constrained growth. If the market's pricing in the future o fLMND as more than an insurance, the most obvious future is a something as a super advantaged customer acquirer: they use their superior tech and great brand to acquire customers at an unheard of price, then they offload the risk to a reinsurer. Because Lemonade acquirers such good customers at such low prices, the company mints money as reinsurers are desperate to take their risk and the company grows to the moon. But, here's the thing: great customer acquisition tools already exist. Basically, you just described an insurance version of Lending Tree (with maybe a little more value add if they can truly get better customers). In fact, the insurance version of Lending Tree already exists... inside of Lending Tree (their quote wizard product). Lending Tree is profitable today (>$100m in EBITDA), yet trades for a market cap below LMND's. I suppose a slight twist on this customer acquisition tool is that Lemonade is uniquely good at acquiring young people who don't have insurance now. In this bull case, LMND acquirers these customers and doesn't make much now, but in a few years when those customers are richer LMND will "own" them and be able to upsell them more expensive / profitable policies.

The chart below (from LMND's S-1 p. 5) is their way of pitching exactly that: over time, the % of our condo insurance policies coming from people who "graduated" from renter's insurance is increasing.

Except that makes no sense. Look, there's no doubt that acquiring a young customer who could spend more with you in the future is a great way to create value over the long term. But every other insurance company knows this too! So LMND will face competition on both ends: other insurance companies will aggressively compete for younger people with renter's insurance; sure, maybe LMND wins them, but they'll win them at a level that isn't super profitable. And while LMND will have an advantage when it comes to selling their customer's more expensive insurance down the line, it's not like the insurance product is crazy sticky. One of the great things about selling a company software is it's super sticky; if all of your spreadsheets are in excel, you're likely to pay significant price increases for excel next year because losing all of those files would be a mammoth pain. And you're more likely to buy products that have excel plug ins because those products increase the value you get from both those products and excel. But consumer insurance isn't difficult; it's a super minor inconvenience to go shopping around for new insurance when I'm ready to change policies. Just because LMND wrote a customer renter's insurance, they don't have a right to significant price raises or owning all of the customer's future spend. Also, the chart above is ridiculous. Of course the number of people buying insurance from you who have done so in the past is going to grow over time. Lemonade is a freaking start up. Most of their customers are brand new! That chart is completely useless. The only way it could be useful is if they showed a real customer retention graph and then comped it to a peer. Something like "hey, in Q1'17, we sold 100 insurance policies. In Q1'18, 90 of the policies renewed, 5 upgraded to condo insurance, and 5 left. Peer averages show that only 60 renew with 2 upgrading and 38 leaving, so our retention and ability to upgrade far surpasses peers." As is, the chart is mindless. It's something that looks and sounds nice but falls apart if you think about it for maybe half a second. Another chart later in their S-1 has similar problems. The chart below shows that customers' increase their spend on renters insurance over time. But that's how pretty much every business works: you get a customer and hope to increase their spend over time. The chart is completely useless without lemonade disclosing how much it cost Lemonade to get the customer, how many of those customers are churning, and how profitable the insurance is. A comparison to what a peer's customer spend looks like over time would be nice too. Some of those numbers can be inferred or assumed by doing some leg work, but many of them cannot. I suspect that's not a coincidence: LMND's management team knows that providing more detailed churn info would be helpful to investors. I suspect that their focus on customer spend over time and the potential for future up selling while leaving out more detailed churn and retention info is not an accident.

I could go on and on about Lemonade and how ridiculous the share price is, but honestly I started this post because I read the S-1 and the valuation was so ridiculous to me that I had to write something and I'm kind of running out of steam at this point. A simple summary: I agree with "Shitfund" on this one: every few years, a fintech product comes along and investors get super excited it will revolutionize some boring industry like insurance or lending. The company sells a bunch of product (loans, insurance, etc.) for fifty cents on the dollar until eventually it becomes clear that they'll never stop burning money and they got hit by a mammoth amount of adverse selection. I see nothing defensible about Lemonade and expect it to roughly follow the Lending Club path; I just hope the options gods create on market on Lemonade before then (there are no publicly traded options on it as far as I can tell, and I'd be very interested in the puts) One last anecdote before I sign off: A few years ago, investors got really excited about Lending Club and bid its market cap up to ~$10B... but then reality set in. The banking market is reasonably regulated and highly competitive as lending people money is basically a commodity product. Lending Club was able to grow because they were under pricing competitors who were extremely sophisticated at pricing risk. That lead to a bunch of bad loans, and the stock quickly blew up as investors realized there was no secret sauce. I suspect Lemonade follows a similar model: initial euphoria, and then a decline as investors realize they aren't offering anything special (and, even if they were, it could quickly be copied by established competitors with significantly better marketing / sales arms). (PS- this is N=1, but a big part of the Geico story was their superior cost structure gave them superior pricing. I compared Lemonade's insurance to my current renter's insurance and found it significantly more expensive. Maybe I'm a horrific risk; if you've done something similar, feel free to respond to this poll and see the results! As I write this, it appears most people would like me to stop talking about LMND, but outside of that it appears ~65% of people are finding their current insurance cheaper than LMND).