Is $QRTEA a Textbook Malone Special Sit or a Classic Value Trap?

One of the best things about running a blog / podcast is that investors get to know your style and reach out to you with ideas that they think you'll like / fit your style. And I've got to say: after almost five years of running this blog, my readers know me really well, as I don't think I've ever been pinged as much on any one stock / special sit as I have on QRTEA in the past month.

The basic thought process behind the QRTEA pitch is: "This is now a John Malone special sit / dividend recap media play. The similarities to the Malone situation in You Can Be a Stock Market Genius (IMO the best book on modern investing) are real." If you made a word cloud for the posts on this blog, every word in that last sentence would be a contender for the largest word in the cloud. Honestly, the only word missing is cable/Charter, and you could argue QRTEA could check that box too. So, yes, my readers know me well. (For more background, here's the best public summary of the QRTEA bull investment thesis / current situation I've seen).

Of course, long time readers may also recall the QRTEA was one of my worst mistakes last year, so it's entirely possible I'm bringing some personal baggage to the situation. That caveat out the way: while I see the appeal of QRTEA, I think it's misguided. There are huge differences between QRTEA today and the Malone special sits in You Can Be a Stock Market Genius. In fact, I think the move at QRTEA reveals an underlying... I don't want to say bearishness, but I will say desire for Liberty to get capital out of QRTEA and into other situations.

Let me back up and start with a brief overview. QRTEA is the holding company for QVC and HSN (so basically, home shopping networks). For years, the bull thesis looked something like this:

The company was really cheap, generally trading at a single digit EBITDA multiple and a double digit free cash flow to equity yield.

QVC + HSN merging would have big synergies

Despite cord cutting, the company was doing much better holding on to viewers / shoppers than a casual observer would think

The company spit off a ton of free cash flow that was returned to shareholders through massive repurchase running the classic Malone levered free cash flow model. Combined with the cheap valuation, these repurchases would result in huge cash flow accretion to the remaining shares.

That thesis fell apart either partly or completely in 2019. Revenue and margins declined, customer count went negative, and in response to the business declines the company shut off their repurchase machine and instead focused on debt paydown. That particularly hurt because the company had been a voracious repurchaser of shares for years in the low $20s, but they slowed down in 2019 when shares were in the mid-teens and then stopped by year end as shares went below $10 (see chart below; the crude drawings on the right represent the average price/share paid during the year).

Let's fast forward from the past to the present. QRTEA was a mammoth beneficiary of work from home and the economy closing. QRTEA almost got hit with a double whammy of good trends from COVID. Similar to online retail, they took share from physical retail because all physical retail was closed. And, similar to Netflix and other streaming services, they gained viewership because people were stuck at home and a lot of other forms of entertainment (sports, movies, etc.) were closed. That combination resulted in impressive customer growth and double digit revenue increases in Q2. Not bad for a company trading at ~5x EBITDA and that many think is in terminal decline! The company believes that the near term environment will continue to benefit them too; obviously Q2 was something of an outlier, but a lot of the underlying trends that helped them remain in place. The below is from their Q2 call:

However, even more than the COVID windfill QRTEA realized, what has people so excited today is QRTEA is engaging in some classic financial engineering. The company will pay out $1.50/share cash div plus a $3/share preferred stock dividend. With QRTEA shares trading for ~$11/share, that represents a return of just under 50% of equity value to QRTEA shareholders. The remaining equity "stub" will be interesting; QRTEA today trades for ~5x EBITDA and is leveraged ~3x. The dividend, in total, represents ~1x of EBITDA, so in total QRTEA is taking leverage up by one turn (from 3x to 4x) and levering the equity more (common equity goes from 40% of the cap structure to 20%). Given the high leverage and relatively capital light nature of QRTEA, the levered cash flow to the equity is huge post-recap; it comes down a little bit to how you adjust for taxes and interest expense and such, but I don't think it's unreasonable to say that QRTEA will have a ~$2.5B market cap post-recap and generate >$1B in cash flow to equity. That's an insane number; QRTEA has argued they may restart share repurchases after the recap, and at these levels QRTEA could retire ~40% of their shares every year with their cash flow post-recap.

Ok, so that's the bull case. Why am I so "bleh" on the deal?

Overall, I think it's just because I don't believe in the long term future of the business. That's a change for me from a year or three ago. I think I can explain this best through an anecdote: Netflix has said they'll never get into sports because, in the long run, the sports leagues will just cut out the middleman and go direct to consumer. In today's world, I view QRTEA as something of a middle man: people turn in QRTEA to watch the personalities and hosts they love, and QRTEA connects them. Over time, I suspect that most of the hosts find it easier to go direct; you can air live on twitch / youtube / instragram, sell stuff through spotify, and even if your audience is a little smaller than QRTEA, you'll capture way way more of the economics. Even if the current crop of hosts don't do that, I think the next batch of QRTEA hosts do, and there will be 1000s of would be hosts who chose to launch their own platforms. Basically, I think QRTEA is competing for attention, and overtime the attention goes to other people, particularly hosts going direct. I just don't see much terminal value in QRTEA anymore.

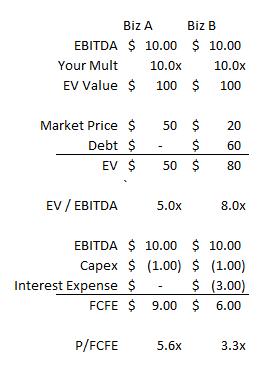

I'm also a little hesitant on using the "look at free cash flow to equity" argument. Obviously that can work really well; the great thing about investing in equity is your downside is limited and your upside is unlimited, so buying levered things at a low multiple tends to work out simply because the ones that work can really work. But I try to stop myself before buying something just because it's got a high free cash flow yield to equity; if you let high cash flow to equity drive you, then you're naturally going to gravitate much, much more to super levered companies. Again, an example might show this best. Say you're looking at two identical companies (Company A & B). You think each is worth 10x EBITDA. Company A has no debt and currently trades for a market cap of $50m, while company B has $60m in debt and currently trades for $20m.

Which would you prefer? Both companies would be ~doubles to reach your fair value estimate. Company A is cheaper on an unlevered basis, but company B is cheaper on a cash flow to equity basis despite being way more expensive.

There's no right answer here. You can do well buying either. But, increasingly, I prefer the margin of safety investing into company A and taking the somewhat safer route versus buying into company B. I just think the increased optionality from the stronger balance sheet and the overall cheaper multiple is worth more.

Again, that's just a hypothetical; obviously I played around with the numbers a bit to get to a more interesting outcome so I admit there are plenty of assumptions in there. But, in effect, QRTEA was already company B, and the current recap is making them more levered. I don't see any value creation there; it just makes it a more levered bet (though you could argue the right way to look at QRTEA equity is a call option on the cash flow lasting longer than the market thinks, and the current financial engineering just increases the volatility of the equity (which increases the value of the call option!)).. Nothing wrong with taking levered bets, but I just wanted to point out the current reshuffling doesn't really create value.

Ok, at this point I've covered how the levered recap doesn't really create value and why I'm increasingly skeptical of the terminal value of QRTEA. Let me turn to my last and biggest issue with QRTEA currently: people seem to think this is some type of bullish Malone special situation, and when I look at QRTEA I see something of the opposite. It seems to me like Malone and co. are trying to get capital out of QRTEA to redeploy elsewhere.

I think most people I talk to who are bullish on QRTEA as a special situation are bullish because it's a Malone vehicle engaged in financial engineering. That recalls the financial engineering at Liberty detailed in Chapter 3 of You Can Be a Stock Market Genius. I get it, but a key piece of that chapter is that Malone was doing everything he could to get money into the Liberty spin.

Compare that to QRTEA today. If insiders were really bullish on QRTEA, they could ignore the market and just keep buying back shares. Malone owns ~30m shares of QRTEA, representing ~7% of shares outstanding. If Malone was really bullish on QRTEA, wouldn't he take the cash that's about to be paid out and use it to repurchase shares instead? Doing so could get him from 7% of shares outstanding to ~10% ownership. Remember, Malone is famously tax adverse; having the company buy back shares directly instead of dividending out money would let him increase his ownership of the company and avoid taxes. If he wanted to get really bullish, Malone could offer a preferred for common swap to shareholders instead of a preferred dividend (i.e. let shareholders exchange common for preferred, with anyone who holds on to their common owning an increasing percentage of the business). Combine the two, and I think Malone could easily get to 25% ownership of QRTEA through simple and tax efficient financial engineering.

Instead, QRTEA is paying out a big dividend. To me, the dividend simply screams "like most retail businesses that didn't have a physical presence, QRTEA benefited from the pandemic. We're going to use that one time boost to get cash out of the business, because we see a lot more attractive opportunities to deploy cash elsewhere."

Look, maybe I'm making this too complicated. Maybe my history with QRTEA means I can't look at it objectively. Perhaps the simple "Yo, it's John Malone + financial engineering + a crazy cheap asset" bull case is the right one and I'm just overthinking it. But I feel like people can be too quick to read bullishness into every move that Malone / Liberty make. Remember, Liberty is an absolute shark. Every move they make is designed to maximize their long term gains. If they're paying a huge dividend out of QRTEA, to me it screams much more "we want to get money out of this business" than "we are bullish on the long term for this business." I'd never want to bet against the team at Liberty, but it somewhat seems to me that buying into QRTEA when Liberty is trying to get money out to redeploy elsewhere is doing exactly that.

PS- remember, when Malone / Liberty is bullish on something, they try to get money into the company. While I think the rights offerings are somewhat strange, I think LILAK / LSXMA rights offerings (mentioned here) check way more of the "bullish" Malone special sit boxes than QRTEA does. Here's an interesting tidbit: if I'm doing my math right, Malone's check for the LILAK rights offering will come out to ~$75m. I believe Malone's cash out from the QRTEA div will come to ~$45m. Allow for a little bit of margin (which Malone has certainly been known to use!), and you could argue the QRTEA dividend was designed specifically to cover Malone's check for the LILAK rights offering. Maybe I'm getting too tin-hat here, but QRTEA's div is payable September 14th and the LILAK rights offering ends September 25. Is that 100% a coincidence?

PPS- also worth remembering that in early 2019 there was a bunch of insider purchasing at QRTEA around ~$12/share. That includes purchases from the CEO, Malone, and Greg (twice!). In total, they bought ~$15m of stock at prices higher than the current price. I think it's pretty telling that they were putting money into the common stock then (both through insider purchases and share buybacks) and now, at prices lower and with a big COVID windfall, they seem to be finding ways to get money out of the company.

PPPS- I believe I'll be taping a podcast on QRTEA with Bill Brewster in the next week or so. Bill is much more bullish than I am, so it should be a fun and informative conversation. Bill's also using his QRTEA pitch to raise money for suicide prevention in a friendly competition; it's a great cause and to the extent this piece or the podcast deliver any value a donation would be much appreciated. As always, if you have questions for the podcast, please feel free to leave them in the comments section (or just slide into my twitter dms!).