BMY CVR: an inspection inflection? $BMYRT

Of everything I've ever done, I think the threesome (podcast) I did on Bristol-Meyers CVR has gotten the most engagement / user interaction. And with good reason! At the time of that podcast, the CVR was trading for around $2/share. If successful, the CVR will payout at $9/share by March 2021, so you're talking about a 4.5x return in ~6 months if the CVR is successful (of course, the CVR is zero if it fails, so there is huge risk here and now might be a good time to remind everyone that nothing on this blog is investment advice!). Still, at the time of the pod I think both guests made a convincing argument that the odds of the CVR paying out was at least 50/50 (which would imply a fair value of at least $4.50, making the CVR quite undervalued).

Anyway, I mention this all because yesterday the CVR popped ~15% to $3.13. The pop was almost certainly driven by this tweet from Sheep of Wall Street (Dan, who was on the podcast) (editor's update: he had to take the photo down, but the core info still is out there). On the heels of that pop, I got pinged by a bunch of different investors; a lot of them were skeptical of an anonymous twitter account posting market moving information (which is normally good skepticism!). Given the move, the skepticism, and that I had done a podcast on the CVR, I wanted to provide a brief update. Of course, I started writing this and when I was halfway through I saw Matt (who was also on the podcast) posted a video update on BMY, so it's probably worth watching his update over reading this!

Anyway, let's start by talking about the tweet that drove yesterday's pop. Dan / Sheep got a picture of an FDA team at the liso-cel facility in Washington. I get the photos are grainy and Dan's twitter account is anonymous, which raises a lot of suspicion. Is there a chance Dan made this up? Sure! FWIW, I think Dan's credible and I believe him.

Ok, next question: is an inspection really worth this big of a move? I think the answer is clearly yes; this is one of the best / most actionable pieces of scuttlebutt I've ever seen. Remember, for the CVR to payout, liso-cel needs to be approved by the end of this year and ide-cel needs to be approved by March 2021. Liso-cel has a PDUFA date of November 16th, so as long as it's approved by the PDUFA date that check mark will be hit. The FDA has said they need to inspect the liso-cel facilities before approving, so at this point your big risk around liso-cel seems to be the FDA inspection happening too late for the CVR to pay out or for the inspection to find something bad (as Matt said around minute 41 of the podcast, the fact the FDA needs to inspect is a huge tell that the safety / efficacy data for liso-cel suggests approval).

With the FDA inspecting the WA facility for liso-cel, it seems like approval by the PDUFA date is extremely likely. Still, it's not completely riskless! Remember, the photos are of the FDA inspecting the WA facility, but liso-cel still has a Texas facility that needs to be inspected. And there's always the chance the FDA finds something that causes them to withhold approval! Still, those risks seem low; I'm not sure why the FDA would inspect WA now and not inspect the Texas facility in time for approval, and BMY is a literal gold standard manufacturing company and liso-cel is a high priority drug for them; I'd be very surprised if they weren't extremely prepared for this inspection / if there was an issue they couldn't address in the inspection that caused a CRL for the drug / for the FDA to miss the PDUFA.

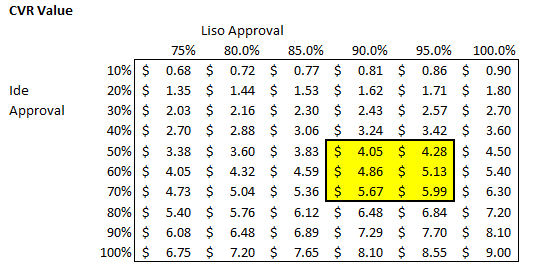

On the podcast, around the 50 minute mark, both Dan and Matt gave liso-cel a ~90% chance of approval by year end. With the inspections happening now, 90% is probably on the low end of approval odds for liso-cel. I've pasted a table below which shows odds of a Liso approval (top row), odds of ide-cel approval (left column), and implied fair value of BMY CVR given those odds. I've also highlighted in yellow where I kind of think fair value is based on the current information we've got.

Anyway, again, nothing on this blog is investing advice, and there's still huge risk here. But I think the CVR may be more undervalued today than it was yesterday or even at the time of the podcast despite the pop. And I think I can explain why: people were already very suspicious of the CVR, and an anonymous twitter account posted one of the best "checks" I've ever seen and no one trusts him. That's fine, but I think he's extremely credible and the CVR represents a really unique opportunity. The stock price starts with a $3 today. By the end of the year, it will either start with a $0 or a $4-$6. I suspect the later is overwhelmingly more likely than the former (though I'll again remind you this is risky and nothing on here is investment advice!).