Is $TREE set to grow?

Long time readers know that there are two conglomerates I follow extremely closely, have enormous respect for, and talk about all of the time: IAC (in addition to the ~12 articles I've done on them, I did a podcast on them with the Boyar Value Group) and Liberty Media (in addition to their investor day recap podcast I did, they've been mentioned too many times to count on this site!). I try to keep tabs on all of the different pieces of each of their respective empires; the companies are so creative with their thinking that there's generally one or two interesting opportunities inside their conglomerate at any given time, and even if not their thoughts are interesting for evaluating opportunities outside their empire.

So, as a long time follower of Liberty, my ears kind of perked up last month when they announced they were selling their whole stake in LendingTree. The party line has been that Liberty decided to sell because they wanted to make GCI / Liberty Broadband a complete pure play heading into the (soon to close) merger. That's plausible.... but I'm still a little suspicious for a few reasons:

Liberty's cost basis in Lending Tree rounded to zero, and Liberty is literally famous for the lengths they will go to avoid unnecessarily paying taxes. I mean, Liberty bought a freaking professional baseball team just to avoid paying taxes! So for Liberty to decide that they'd rather have $900m of cash and send $100m to the taxman instead of having a $1B of TREE stake is extremely odd.

As recently as two years ago, Liberty was a buyer of TREE stock. They bought ~$50m of TREE shares at prices around today's share price in July 2018. Facts change and people change their minds all of the time (particularly post pandemic!), but it is a little strange for Liberty to have been increasing their stake in TREE two years ago and then today decide "you know what, we want a completely clean cable tracker." Liberty historically has shown absolutely no aversion to creating complex trackers when it's in their interest and/or they think there's an attractive investment opportunity (remember the Liberty Sirius / Formula One / Live nation bail out?). The end game for GLIBA / LBRDA was always a merger that combined the two (and then a subsequent one with Charter); Liberty knew this from the day GLIBA was created. It's just a strange event path if two years ago Liberty was increasing their stake knowing that they'd eventually want to bail out of their stake when they announced the most obvious merger in the history of the stock market (which GLIBA / LBRDA always has been).

Liberty sold out of their TREE entire stake on November 16. Lending Tree presented at Liberty's investor day on November 20. Selling out of their entire stake and then having the company present at their investor day a few days later is.... awkward, to say the least.

Combine all of that, and my gut tells me that Liberty wasn't just selling to clean up their cap structure and make a cleaner cable story going forward. If you want to put some rose colored glasses on, I think you could look at the sale and say Liberty just didn't like the opportunity cost of holding TREE stock versus buying back their shares. There's probably some kernel of truth to that line of thinking.... but I think when you really look at the mosaic it's pretty obvious that Liberty sold their TREE stake because they were at least somewhat bearish on TREE. Given Malone's history of avoiding taxes, I couldn't argue with you if you said they would only sell their TREE stake if they were REALLY bearish on TREE.

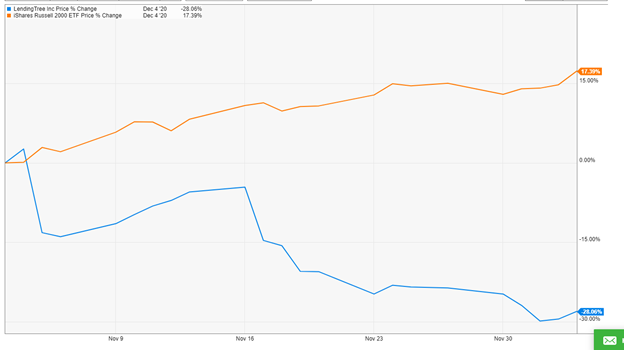

So when Liberty sold their TREE stake, I mentally washed TREE from my mind.... but then the share price did this:

And TREE responded by giving their CEO / founder (Doug) a new employment agreement with stock options with a minimum vesting hurdle that required a ~15% annualized stock price over the next 4.25 years (ending share price of ~$433), and a high end payout that requires a 28.5% return 4.25 years (ending share price ~$696).

If there's one thing I've learned from Mike from Nongaap has taught me, it's that that type of heavily stock price based deal is fertile grounds for searching for alpha opportunities. I've mentioned many times that Mike is my favorite subscription service out there (including mentioning it on our podcast!), so if something reminds me of a "Mike lesson", I instantly send it to the top of my research list (as well as sending a tweet to Mike to see if I can bait him into helping me research it!).

And this TREE deal had "Mike lessons" all over it. Remember, it's not just that TREE gave their founder / CEO a package that required a huge share price increase. It's also that they gave their CEO this deal right after TREE saw their controlling shareholder leave the company in very public and very sudden fashion. And, given Liberty's following, I would guess a ton of TREE's shareholders were in the stock only because Liberty was there.

Put it all together, and I think you could make an easy argument that Doug (TREE's founder / CEO) had TREE completely over a barrel. His employment agreement was set to expire in early January 2021. If he left in the wake of Liberty exiting the stock..... well, you'd have to imagine the company would be in complete free fall. What executive would want to step into a job where the controlling shareholder just dumped their full stake and the founder/CEO left a month later? I can't imagine any would; the writing would be on the wall that the company was broken. And how many employees would see their controlling shareholder leave, the founder leave, and the likely evisceration of the stock price that would follow and not brush up their resume / look to jump ship?

So I think Doug had a crazy amount of leverage with the board ("I leave and you're going to have insane employee turnover, you'll never find a quality exec to step into the CEO role, and the stock will crater"). Of course, the board had some leverage over Doug ("You own 2.2m shares of stock worth ~$500m; if you leave, what happens to that?"), but I tend to think the power dynamics of the board once Liberty left give the vast majority of the leverage to Doug.

Given Doug's leverage, that makes the share grant and the strike prices even more interesting; if he was bearish TREE, he could have asked for a huge cash bonus to stay with the company. He didn't do that. Instead, he took a contract that required borderline epic stock performance for him to hit the high end of the payout.

I don't think Doug takes this deal unless he has good line of sight into the company's trajectory and thinks the high end share price targets are pretty easily attainable. Obviously, anything can happen in 4.5 years, but given Doug's negotiating leverage, I think he takes this particular package having good line of sight into product launch / guidance / visibility that TREE's intrinsic value will be materially higher than the high end share price.

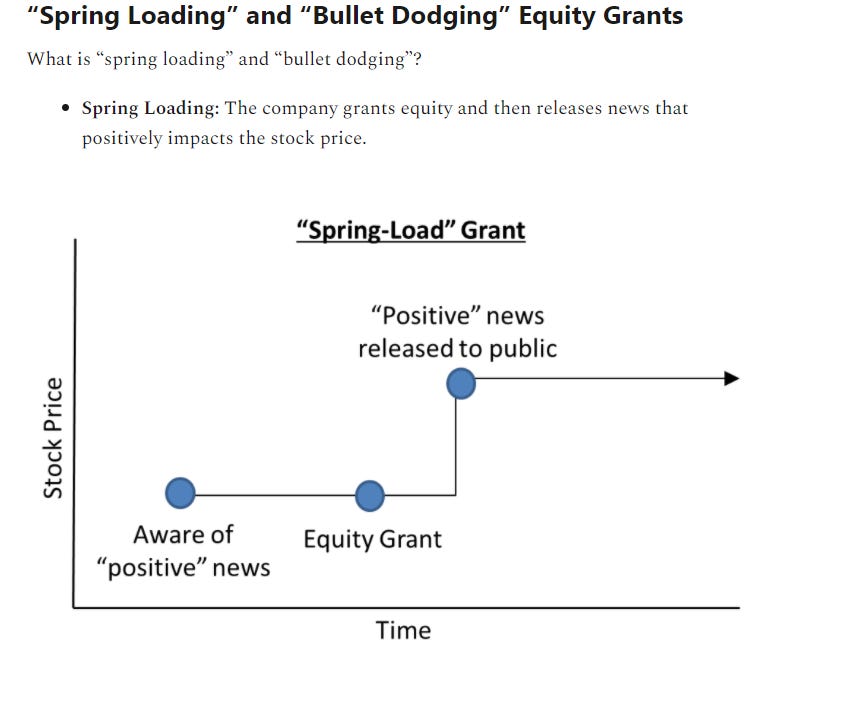

How could he have that much confidence? Mike introduced the concept of "Spring loading", where a company gives insiders equity grants right before good news hits.

It feels like that's close to what is happening here. If you look historically, LendingTree has provided year ahead guidance in early December. For example, here's their 2020 guidance in December 2019, and here's their 2019 guidance in December 2018.

I'm not sure if TREE is providing 2021 guidance this year; they generally do so ahead of an analyst / investor day, and I'm not sure if they're having one this year (they haven't announced one that I can see). Plenty of investor days have been cancelled because of COVID, and a lot of companies are scared to give guidance because of COVID.

So I'm not saying TREE is giving out advantageous stock grants now and will announce blow out guidance tomorrow. What I am saying is that historical precedent says TREE has clearly done all of their annual / year ahead budgeting by this time of the year, so Doug and the board negotiated his comp package knowing exactly what they were forecasting for 2021.

If you believe that Doug had the leverage to get a very favorable equity package, and he chose to take a package with these share price requirements while knowing what they're budgeting for 2021 numbers.... well, I'd guess those 2021 numbers look very, very good versus the consensus or whatever is factored into the stock price.

If you wanted to take a crazy bullish view, LendingTree is currently trying to juice the "my LendingTree" product. It's basically a way to increase customer LTV, improve share of wallet, and avoid having to pay the google tax multiple times on the same customer. Your super bullish view here is Doug can see internal KPI that my lendingtree is accelerating the business, and he's taking a bunch of stock here because a year from now TREE will have levelled up from pure Google SEO arb into a company that actually controls consumer's wallets and owns their customer relationship (that's a much, much higher value business).

BTW, this would not be the first time insiders at LendingTree have played games to enrich themselves when the stock price was depressed. Hat tip to Christian for pointing this out, but at the depths of the financial crisis the company entered into an agreement with Doug to sell him 935k shares at $3.91/share. With the stock currently trading over $200/share, that $4m investment has netted him well over $200m in profit in ~11 years. Not bad! (Image below from their 2010 proxy).

I've still got a lot of work to do on TREE. I'm familiar with the story and can see both the bull and bear cases pretty clearly. I'm not sure if I'll ever get comfortable enough with the bull case to invest here (clearly Liberty couldn't!).

But the timing of that equity grant is absolutely screaming "insiders believe Lending Tree's stock is going significantly higher and are trying to get a piece of it."

It's tough to ignore a signal like that.