Ten Predictions for 2021, Part 2: Non-SPAC Edition

This is part 2 of my predictions for 2021. Part 2 centers on my non-SPAC predictions; you can find part 1, which focused on SPACs, here.

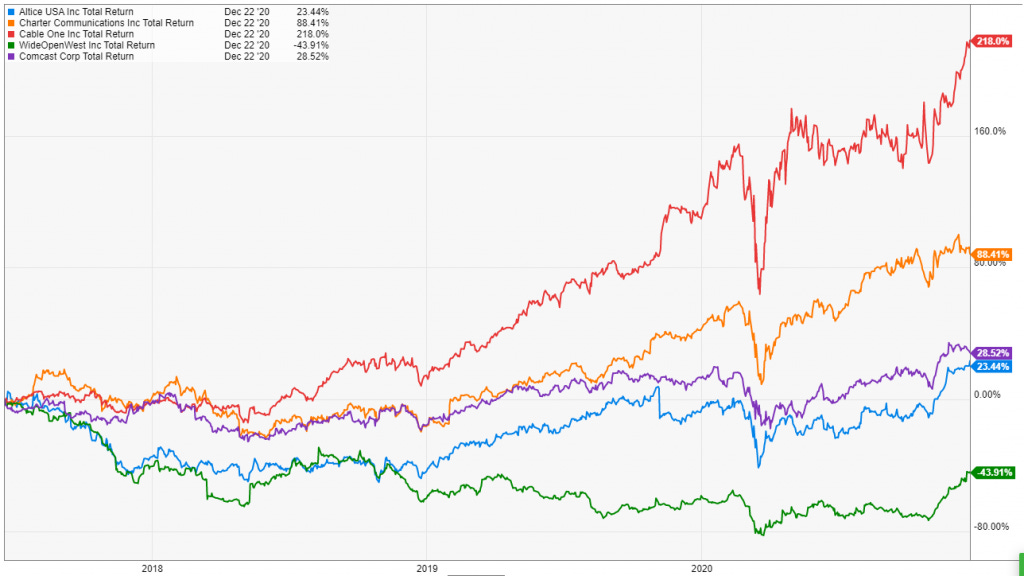

Cable One (CABO) massively underperforms its cable peers

Cruise stocks have a rough 2021

Free Radical media companies finally start to consolidate

All the major movie theaters file for bankruptcy

Hottest sector for M&A? Restaurants and retail

Prediction #6: Cable One (CABO) massively underperforms its cable peers

Long time readers know that I follow the cable industry closely. CABO has been something of an anomaly in the cable industry; no one doubts they have good assets, but they trade for a huge premium to peers no matter how you judge their valuation.

That valuation gap has expanded over time as CABO's stock has massively outperformed peers.

I think that outperformance ends in 2021, likely driven by CABO's multiple compressing a little bit while the other cable companies see their multiples expand significantly (I continue to think that cable is an infrastructure like asset, and should see a correspondingly high EBITDA multiple to match).

Why do I think CABO's multiple compresses? I suspect part of Cable One's huge multiple growth has been the fact that Cable One is the only cable stock that has been investable for small and midcap investors. That's no longer the case; Cable One's market cap is now approaching $14B, which is large enough for Cable One to qualify for large cap industries (including the S&P 500). I suspect that Cable One will start getting dropped from small/midcap indices in 2021, and added to large cap indices, and the resulting turnover will take CABO's multiple down a few pegs.

Maybe it seems crazy to suggest getting added to large cap indices will result in multiple compression. But there's a recent example to point to! Kinsale Capital (KNSL) is a good company that trades at an absolute nosebleed valuation; they saw their stock sell off hard when they got moved from small cap indices into midcap industries earlier this month. I suspect something similar could happen with Cable One; once it gets put into large cap indices, the stock sells off as it no longer dominates a few smaller indices. And then it keeps selling off because it's tough to imagine any large cap investor would prefer buying Cable One to one of their larger peers at anything close to today's prices.

Along these lines, it's interesting to note that, of the five major cable companies, two of them were aggressively repurchasing shares in 2020 (Altice and Charter) and two of them have a history of share repurchases and have suggested they are eager to repurchase shares once they get leverage down (WOW and Comcast). Cable One is the only company who has actually gone the other way, as they issued shares (at prices well below today's levels!) earlier this year. To be fair, CABO has been able to do more needle moving M&A than their peers, so the share issuance was largely towards funding inorganic growth, but I do think it's telling that their peers with much lower are treating their equity like a precious commodity while CABO seems more than willing to dilute themselves at these levels.

One reason a small cap company might trade at a premium to a large cap company is the small cap company has some acquisition premium built in. CABO would be a natural target for any of the larger players if they ever were put up for sale.... but the multiple discrepancy between the large players and CABO precludes any acquisition for now. Large players would be better served buying back shares at these levels and waiting for the multiple disparity to collapse.

Disclosure: I am short Cable One in very small size, and I am long some of the larger cable companies in very large size. Nothing on this blog is a recommendation, and shorting in particular is risky.

Prediction #7: Cruise stocks have a rough 2021

I'll openly admit to being a little obsessed with cruise lines. Every monthly links post includes a piece on them, and I even went on another podcast and rambled on them for ~15 minutes. I can't help it; ever since BB published the piece on cruising that included customers whose experience getting quarantined for 14 days on a COVID ship "solidified" cruising as a #1 choice for them and customers comparing their addiction to cruising to rats being addicted to cocaine, I've just been endlessly obsessed with how cruising recovers from COVID.

Calling the yearly stock performance of an entire industry is much more macro and short term than I usually do, but given that cruise obsession I'm going to step out of my comfort zone and do it. I think the cruise line stocks are set to have a very rough 2021.

In some ways, I view this as "buy the rumor, sell the news." The back half of this year was about buying the "rumor" of reopening in 2021; 2021 will be selling the "news" of reopening as the companies continue to burn tons of cash and report awful numbers until we're fully vaccinated (and maybe even beyond, as customers and government demand better hygiene and pandemic protection on cruises; increasing expenses and decreasing NPS).

Why do I believe they underperform? Well, cruise lines are generally trading at EVs in line with where they traded at the start of the year (I tweeted this chart in November, and it's still around directionally correct), so you're starting from a place where the market has effectively discounted no change to earnings power from 2019 levels. The first half of 2021 should prove that wrong: the cruise lines are still going to be burning hundreds of millions of dollars every quarter (actually, every month; Carnival, for example, will burn ~$530m/month in Q4'20, but let's be generous). As we get into the back half of the year, we'll increasingly have line of sight into a more normal 2022, but I think cruise ships will reveal a higher cost structure permanently as they put in place new measures to make cruising more hygienic / less likely to spread a pandemic. And I wouldn't be surprised if some of these measures not only increased costs but also took some of the fun of cruising away at the margins, resulting in a lower NPS. All in, I think 2021 sees the cruise lines burn a ton more cash and the "new normal" the market looks forward to in 2022 includes a higher cost structure for a worse product.

Your counter to all this would be: sure, they'll have a rough 2021, but they'll be looking forward to a really bright 2022. Demand will be off the charts as people who love cruising but have been barred from it for 18 months look to return, and cruising could look a lot more interesting as some competitive products (like mom and pop resorts) have gone bankrupt and capacity has come down given ship scrapped / new build delayed. So you could have a scenario where demand is up and competitive supply is down, resulting in some pricing power plus a customer set that is ready to rage once they get on the boat (resulting in huge increases in high margin drink sales on board). I get that bull case, but I just think at this valuations and with the amount of cash these companies are going to burn in 2021, the stock prices are already discounting much too rosy a future.

The "cruise to nowhere" I think is a good example of everything here. It certainly proves demand for cruising is there (Royal Caribbean noted booking 6x higher in October than previously), but if you read through the article and note all of the extra COVID protocols and start thinking about how much worse the experience is for guests (to say nothing of how bad it gets on COVID scares), I think it's going to be very difficult for the cruise companies to make money until we return completely to "Normal" and even then the cruise lines will have done significant damage to their brand equity. The end of the NYT cruise to nowhere article includes the quote "you don't really get to loosen up" from a passenger and the line "fun and relaxation take some planning." I'm not sure that's the combination that leads to happy repeat customers, and cruise ships will be running a bunch of cruises in 2021 under those exact parameters.

I also think that some consumers will remember the pandemic environment for years and be hesitant to book cruises / go to mass attendance events. I think that's just on the margins, and eventually it goes away, but I could see the most marginal consumer deciding to stay at home or do a lower key / less crowded vacation for several years as the scars from the pandemic linger in everyone's minds.

I somewhat base this call on company behavior as well. It's natural for companies to hoard capital after a near death experience, but I don't think I've ever seen anything like the current combination of the equity market's enthusiasm for cruise stocks and the cruise sectors enthusiasm to raise capital and sell equity. In October, CCL was at a conference and bragging about how they managed to get through the pandemic mostly by raising debt. Things have certainly changed since then; as cruise stocks have rocketed higher, cruise companies have sold shares at a furious pace. CCL completed two ATM programs to raise $2.5B as well as hundreds of millions in convert debt for equity swaps. NCLH did a stock offering in November, and RCL followed an October offering with a December ATM program.

Again, maybe this is just be companies being overly cautious after a near death experience, but I've never seen an industry this desperate for money raise so much money so easily. In general, industries this eager to issue equity do so for a reason, and investors on the other side of that pay the price.

I was very tempted to include some other travel / leisure related plays here; both Six Flags (SIX) and Dave & Busters (PLAY) seem interesting on a bunch of themes similar to the cruise lines, but I haven't done enough work on them.

I'll just quickly highlight SIX here to show what mean. As I write this, their EV is approaching $6B (see cap structure below). Pre-pandemic, SIX was forecasting ~$450m in EBITDA. They think their new baseline earnings level is ~$550m thanks to cost cuts and other change they've made in response to the pandemic. Let's just take them at their word and say that this business will be more profitable post-pandemic, though I have serious doubts; that means the company is trading at ~11x "baseline" EBITDA without giving any credit to cash burn through the rest of 2020 or in 2021 (when they'll be well below operating capacity due to continued COVID restrictions; per Q3'20 call, the company is EBITDA breakeven at ~50% attendance and FCF breakeven at ~70% capacity, the former seems like a stretch for 2021 while the later seems like a pipe dream).

What valuation would make sense for SIX flags? Well, I highlighted in my January links that peer Merlin had been taken out for 11.7x EBITDA. That means, at today's prices, SIX is basically trading on a Merlin level takeout multiple of their "future" baseline earnings level. That seems aggressive to me; again, they'll burn cash until the environment "normalizes", that baseline level incorporates a huge increase from their original 2020 guidance, and they'll be paying increased interest expenses on all the expensive pandemic financing they raised for years. Now, a bull might counter that interest rates are lower today, and SIX is a better business than Merlin so it would get a better takeout multiple. I'd agree with both those arguments, but it just seems that the current stock price is forecasting a borderline perfect bull case scenario of COVID quickly disappearing and SIX instantly ramping up and hitting all of their numbers. That feels too optimistic.

Humorously, I wonder if SIX would be better off private than public right now, simply because they'd be a perfect SPAC target (a brand people know, a recovery play, a credible need to merge with a SPAC for short term liquidity to bridge them to a rosier future, and the ability to project massive increase in EBITDA in a few years). Perhaps that shows how crazy the SPAC market is, perhaps that shows how SPAC crazy I've gone, or maybe some combination!

PS- I consider "mass group" plays like cruises, Six Flags, and PLAY to be the biggest reopening plays, but just about everything travel / leisure falls in here, and I'm seeing a similar dynamic across the board. Consider, for example, hotel companies (HLT, WH, MAR). The market has already looked straight through the current awful results to a rosier future, and all of these stocks are basically back to all time highs. At the same time, basically every hotel company has seen pretty significant insider selling in the past month or two. Maybe that's to be expected: the market sees a rosier future, while insiders see the industry they've devoted their lives to that was on deaths door a few months ago and is still reporting the worst results they've ever seen and they want to take some chips off the table just for their own personal security / sanity. Very possible!!!.... but it sure seems like insiders are screaming "my god our shares are overvalued; get me the heck out of here before this bubble collapses!"

PPS- it didn't get a lot of play at the time, but in June I noted how OSW's management was plundering their shareholders. OSW shares are currently trading for ~$9/share, which means OSW held their shareholders over the fire in order to enrich management and insiders by >$100m in about 6 months. Is that shameful? Yeah, absolutely, but honestly I'm a little awed by their greed and ability to profit from a pandemic / crisis.

I wanted to highlight it because 1) again, it didn't get much play at the time, but with hindsight it's both a breathtaking investment and a breathtaking display of insiders abusing minority shareholders and 2) investors should probably expect some value leakage to insiders across the board at travel / leisure plays as boards look to reward management teams who steered their companies through the crisis. Certainly nothing on the OSW level, but I'd bet you see some pretty generous bonuses and stock grants in the next few years.

Prediction #8: Free Radical media companies finally start to consolidate in 2021

A few years ago, John Malone talked about the need for the "free radicals" of smaller, independent media companies to consolidate to prepare for the direct to consumer future. While we've seen some M&A since then (Discovery buying Scripps, Lionsgate merging with Starz, CBS remerging with Viacom, Fox and Disney), I've been surprised by how many of the free radicals have remained independent.

The most obvious free radical candidates are Lionsgate (which owns Lionsgate and Starz), AMC Networks (self explanatory), and MGM (owns MGM studios and EPIX), but there are a few others. Honestly, given the size and scale of Netflix and Disney, and the balance sheet of Amazon and Apple, I think even really large players like Discovery and Fox (Fox News and Fox Network) would qualify as free radicals at this point.

I suspect that a large reason the free radicals have been so frozen is timing related. DIS + Fox and TimeWarner / AT&T were mammoth deals that kind of froze the industry landscape.... and right on the heels of those deals closing and getting integrated we got the pandemic that basically froze movie production and deal making for the rest of the year.

My prediction: 2021 is going to see a wave of free radicals getting scooped up by larger players. Why do I think now's the time?

Well, on the buyer side, the larger players should be relatively integrated at this point, and all of them will be rolling out their D2C plays. By the summer, HBO Max, Peacock, and CBS All Access (soon to be Paramount+) will all be able to look a their numbers and their results and say, "Ok, we've got the tech down, we've got at least six months of fully marketing this thing down, and we've got the majority of our assets on here." I suspect when they do that, they're going to look at their numbers versus Disney+ and Netflix and say, "O Damn, we are getting slaughtered." There will be a bunch of reasons for that, but I think they'll talk themselves into a big reason being they don't have enough compelling programming, and that the solution to that is M&A.

On the seller side, MGM is currently exploring a sale. With that process running, I think a lot of the smaller players are going to look at their own assets and the future and realize that the best time to sell is now, and that if they don't their assets will get smaller and less relevant over time, resulting in lower value in the future. And while MGM if the only company explicitly exploring a sale; I've noticed language at a lot of the other smaller companies that suggest valuation and multiples are certainly on their mind. For example, over the past few months, I've seen Lionsgate (LGF) harp about the value of their library several times. Now, they've always done that, but I just feel like they've been much more explicit and frequent with the discussion recently.

So I think all the stars align for M&A in 2021. On the buyer side, their balance sheets will be in order, their legacy integrations will be finished, and they'll be looking at their current set of assets and realizing they need more content to compete. On the seller side, they all seem to be coming to a place where they realize they're too small to compete and nothing will change that. If MGM actually sells, I think that's the first domino that sets off a wave of M&A as sellers say "I better sell before it's too late" and buyers look at the landscape and say "I better buy before there's nothing left to buy."

There are really only 7 major studios with movie libraries out there: Disney and all of their subs, Columbia (owned by Sony), Universal (NBC / Comcast), Paramount (CBS), Warner Bros (TimeWarner/AT&T), MGM, and Lionsgate. If MGM gets bought, suddenly you could see a lot of people with streaming dreams look at the landscape and realize they could be stuck subscale without anything to buy or a movie studio to anchor their catalogue. Apple was rumored to be in talks with MGM in 2018, does the current sales process lead to that deal finally happening? If so, suddenly anyone with dreams of getting bigger could look at that landscape and see Lionsgate as the only company with a substantial movie catalogue that could realistically be purchased, and Lionsgate could look at that landscape and realize that their assets will dwindle in value without proper distribution.

A bonus prediction: if we start seeing a wave of media M&A, I would not be surprised to see the people who miss out on the first wave of M&A look to explore more tangential ways to grab IP. Let's just make up a future and say Discovery buys MGM and Apple buys Lionsgate. If you're Amazon, you probably look at that future and see your streaming dreams falling behind. You don't really have must have IP (though maybe the new Lord of the Rings show will qualify!, and you don't have a library of movies or anything. Wouldn't looking at something like Hasbro or Mattel make a lot of sense? No one could exploit their IP like Amazon could; they'd have insane data on what toys people order to turn into movies, and they could use peoples viewing habits on movies to pitch them shows.

This relates to the whole M&A angle, but I think the synergies between a large player buying an elite piece of IP continue to go up. The strength of Star Wars alone has been enough to propel Disney+ for a year. Lionsgate owns Hunger Games, Twilight, and John Wick; isn't there enough in each of those universes that a potential acquirer could buy them and use that IP to create a bunch of new shows a la Disney with Mando and all of its spins that could take a streaming service to the next level?

Or maybe Amazon aims a little higher if they miss out on MGM and LGF; VIAC assets always seemed like they made more sense inside a larger company. Could Amazon look to buy VIAC? The synergies would be huge: merchandise from the NICK side, better exploitation of Star Trek given Amazons resources, and a boost to Amazons sports efforts given CBS's relationship the the NCAA / NFL / golf / etc. The counter to this is buying CBS would include the headaches of having to deal with a legacy cable broadcaster and possibly attacks on the cbs newsdesk (something I'm sure Bezos is familiar with thanks to the Washington Post!). That's why I think LGF is such an attractive acquisition target: you get a major movie catalogue plus one of the few major streaming services without the headache of legacy cable channels.

Just to wrap this up because I feel like I wasn't explicit enough in this: great content has value, but distribution is more valuable. And, without distribution, great content's value will start to diminish over time. So if you're one of the smaller players: your content's value is at its peak right now, when it is both most relevant and all of the larger players are still trying to find their tentpole franchises. Hunger Games and Twilight have value, sure.... but they would have had more value ten years ago if Lionsgate had sold them when they were most culturally relevant. If Lionsgate waits another ten years to sell them, they'll become less culturally relevant, less able to launch tentpole movies / tv shows / world build, and therefore less valuable. The time for small media players to sell is now.

Pretty much any video game company would be an obvious play here too; Netflix had great success with the Witcher and is looking to follow that up with Elder Scrolls. Again, the synergies Amazon would have with buying a gaming studio and turning their IP into TV shows while selling merch and everything on the side would be massive, and Amazon has made nascent efforts to get into video games before....

Prediction #9: All the major movie theaters file for bankruptcy

Recently, there's been a little excitement for movie theater stocks and about 2021 box office. IMAX, for example, talked about the "embarrassment of riches" for the 2021 slate. I think that hype gives way to a much bleaker reality: the box office is going to be decimated in the front half of 2021, movie theaters are going to have almost no leverage in negotiations with studios, and I think all of the major theaters go bankrupt and/or have to restructure in some form.

As we go through 2021, movie studios are going to have a choice with all of their films: release them into socially distanced movie theaters to small box office numbers given the capacity limitations, or put them immediately onto your streaming service to try to drive subs. That's an easy choice; studios are going to increasingly prioritize their streaming service, and once that genie is out of the bottle there's no going back. Movie theaters can whine about it all they want, but their complaints won't really matter. Disney and Netflix have seen their valuations go multiples beyond what any movie studio has ever dreamed of achieving by focusing on their streaming service, and every media company is going to have dreams of doing something similar. Even pre-pandemic, it increasingly only made sense for movie studios to release the super tentpole movies (the superhero movies) into theaters given the marketing and distribution costs, and the pandemic has only accelerated that math.

As we hit the back half of 2021, theaters are going to be desperate for content to put on their screens. Movie studios will have that content, but the only content that will make sense to release is the tentpole movies. And that's going to give movie studios insane leverage when negotiating film splits with the theaters. On one hand, you have movie studios that can just put movies on their streaming service to drive subs; on the other hand, you have theaters that are bleeding millions in cash and desperate for content. Combine months of cash burn absolutely no leverage in their negotiations, and it's going to become increasingly clear that movie theaters are not viable in their current form. All of them will need to file for bankruptcy to reset their cost structure and lower both their interest burden and rent expense.

Bulls are going to say there's demand for a movie experience. WW1984 launched on Christmas day and did $16.7m at the box office (the best opening since the pandemic started) despite releasing on HBOMAx the same day, continued social distancing restrictions at theaters, and most theaters in major markets (NYC, LA, etc.) being closed. I saw one analysis that the WW1984 opening was equivalent to a $110-120m opening in normal times, a bit bigger than the original WW did at the box office. I'm not super arguing with any of those points; I think demand remains for a variety of in-person experiences, including movie going. But I do think that the theaters lost a huge amount of negotiating leverage during the pandemic; allowing films to release day and date on streaming services was Pandora's box and now that it's open there's no going back. The fundamental point remains: Studios are going to take larger and larger cuts of whatever box office is left given both their negotiating leverage and ability to throw movies onto their streaming service as an alternative, and theaters need to restructure their cost structure lower to adapt to that new normal.

Note that this trend will only get accelerated if the free radicals consolidate (prediction #8 above). If someone with streaming ambitions buys MGM and/or Lionsgate, I'm sure a few more of their movies will go to straight to streaming going forward. That's a few fewer movies going to theaters, and a little more negotiating leverage for the remaining studios with their remaining film slate.

Prediction #10: Hottest sector for M&A? Restaurants and retail

It's a weird time to be a restaurant. With indoor dining closed, some restaurants are reporting sales that round to roughly zero. But others are seeing sales boom; Chipotle is posting >8% SSS increases, and all of the pizza companies are doing incredible business (DPZ did 17.5% SSS increases in Q3). So on one hand you've got a weird bifurcation in the market where some companies are doing insanely well while others are on death's door. Then there's the huge and rapid changes to how restaurants interact with customers, as digital and delivery pull forward ten years worth of sales growth in a month. Add to both of those consolidation among the delivery players, with uber buying postmates and grubhub getting bought by justeat, and I think you've got a trifecta that sets up for a ton of M&A in the space.

The rationale is pretty simple: restaurant M&A allows for tech synergies (increasingly important as digital becomes a focus!) and increased negotiating leverage with the delivery players. I think we see a wave of smaller / medium plaers getting gobbled up by larger players over the next few years.

I think these companies need to be integrated pretty tightly, which might make them a little different than traditional M&A in the space. For example, consider YUM, which owns KFC + Taco Bell + Pizza Hut. The integration between those brands appears to be pretty limited, which makes sense given they're largely franchised. I think an M&A wave would make sense focusing on tighter integration to lure people into an ecosystem. It would look something like this: Shake Shack and Chipotle own all of their stores. What if the two of them merged? They could combine loyalty programs to try to nudge incremental orders into their system, and they could use their combined heft to push for significantly better terms from delivery players. (I'm not saying those two will merge; just using it as an example)

I wonder if a big tech player would get into the restaurant space. Amazon would be the most likely player. Imagine if they bought Starbucks; suddenly they'd have a daily touchpoint with millions of Americans. Wouldn't there be some pretty interesting synergies? Amazon could use Starbucks for pick up spots, which would drive increased business for the Starbucks will also increasing Amazon's number of pick up spots.

Antitrust and/or politics probably precludes it, but it's a fun thought!

It also might apply better to Amazon buying C-Stores like 7/11; they would function as perfect posts for Amazon's last mile of delivery, and they'd enable Amazon to touch a huge swath of people daily as they filed up on gas or grabbed their morning coffee (though Amazon might not want the environmental headache of owning gas stations!).

I'll be honest: I am not a restaurant industry expert, so it's possible I'm just completely off here for some reason. But I wanted to hit ten predictions, and the combination of industry in turmoil + key supplier base consolidating generally leads to consolidation, so I figured I'd step out of my comfort zone a little with this prediction,

Notice that the prediction included restaurants and retail, and I've focused on restaurants so far. All of the same arguments apply for retail; in fact, a lot of the logic applies more to retail than restaurants. So I think we will see a good amount of M&A in retail as well, though the mergers probably work out a little less well than restaurants as I think the majority of that sector is just in too much trouble for anything to really change their dynamic.