Introducing the "Why the low multiple" series

I mentioned in my 2024 vision and outlook that I wanted to start infrequently doing a series where I just took a company or, preferably, an entire sector that’s trading at a really low multiple and asked “What’s going on here?” with the hope of sparking a conversation and maybe learning a little bit more.

At any given time, there are normally plenty of companies that are trading at a low multiple (I generally think of low multiple as less than 5x earnings and that’s how I’ll loosely use it through this series). In general, companies trade at a low multiple when the market doubts the sustainability of their earnings for some reason. If you have a P/E of 2x (which equates to a 50% earnings yield), it’s generally not because the market thinks you’re going to grow your earnings! After all, if your earnings just flatlined at that level and you sent all your cash back to shareholders, your shareholders would make a 50% return every year from that multiple, which would quickly make them the greatest investor of all time! So most of the time you’ll see companies trading at really low P/Es because the market doubts the sustainability of their earnings. For example, chemical companies are famously cyclical; they’ll earn a billion when things are hot one year and then lose five hundred million the next as the cycle turns against them. In the year that they’re earning a billion, the market will trade them for like a four billion market cap (or a 4x P/E) because the market is looking through the temporary windfall in earnings and trying to value the business on what it will earn through the whole cycle.

But a low multiple makes for a really interesting deal, because if the peak pricing lasts for just a little bit longer than the market thinks, then the company can earn a huge portion of their market cap quickly. In the chemical example above, if the peak earnings last for two years instead of ending instantly, then the company will have earned half its market cap at that pricing (they trade for a 4x P/E and they earn that amount for two years, thus half their market cap!)…. or if the market gets just a little hotter and earnings actually go up even more, it’s entirely possible for a cyclical company to earn their entire market cap in a year or two. Consider nat gas in europe; I guarantee you any nat gas play would have been trading for a very low multiple in late 2021 as market doubted the sustainability of ~$30 nat gas…. only to see nat gas briefly touch $300 just a few months later! There’s no reason windfall pricing can’t get even more windfall-y!

An example might show how powerful the combination of a low multiple and earnings not falling off a cliff can be. Long time readers will remember I got a little obsessed with cyclical companies a few years ago. Like almost every business, cyclicals were coming off a banner 2021 as the economy rebounded from covid, and they had generally used the banner year to completely clean up their balance sheet. With now pristine balance sheets, they were trading for low multiples as the market doubted the sustainability of their earnings. The company I mentioned as a particularly interesting example was X (U.S. Steel, not the company formerly known as Twitter), which was trading for around 1.5x LTM EBITDA and had used their cash gush to completely transform their balance sheet. I also found it interesting that their CEO had just been granted some RSUs that didn’t fully vest unless the stock hit $55.

I wish I had just taken my own advice / interest seriously, because less than two years later X found itself subject to a bidding war that saw them sell themselves for (surprise, surprise) $55/share (yes, the exact number that maxed the CEO’s RSUs, though I suspect he would have been made whole on a change of control anyway), generating outstanding returns over the hypothetical two year hold period from that post.

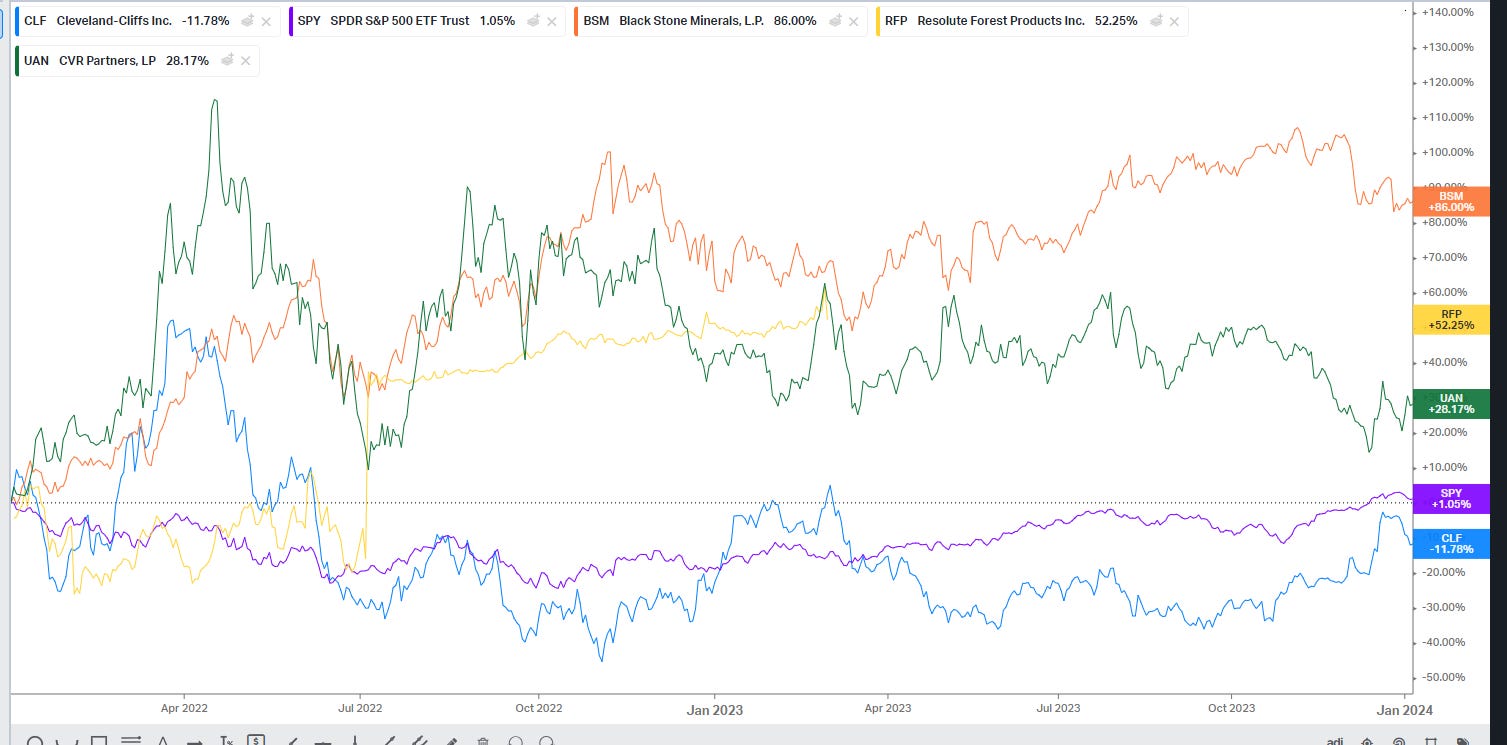

That’s obviously an n = 1 situation, and the high takeout price was in part the result of a bidding war… but I mentioned four other low multiple cyclicals as interesting in that article (UAN, RFP, BSM, CLF) ; none of them performed quite as well as X, but another (RFP) was taken out at a nice premium and on the whole the basket would have smashed the market.

Again, this look back is somewhat resulting. We could have gone into an immediate huge recession and all of these could have gone bankrupt or into distress or something (though distress / bankruptcy would have been tough; again, they had just used their record profits to completely clean up their balance sheet!). And in the same article I mentioned I thought retailers also looked interesting given how low of a multiple they traded for; buying those turned out to be a disaster. But the low multiple / cyclicals trade is just a nice example to show how powerful the returns can be when the market gives something a low multiple on the assumption that earnings are going to drop and them earnings don’t quite nosedive.

Of course, there are plenty of reasons other than cyclicality a company might trade for a really low multiple. For example, the real sin stocks like tobacco and coal tend to trade at low multiples because the market suspects they have no terminal value (i.e. the market doubts anyone will be burning coal or buying cigarettes in 2040).

But even stocks with no terminal value can create plenty of value between now and their “inevitable” demise (and I use inevitable demise loosely; this article on gasoline demand rising through predictions of its peak is a good reminder that we’re often early to call the end!); the nice thing about a dying industry is margins tend to be high because no one in their right mind wants to launch a competitor so you can just run them for huge cash flow given limited competition (I quoted this in my piece on refiners, but I love how one owner of a potentially dying business noted, “it’s a sunset industry, but it’s going to be a beautiful sunset”), and most management teams of “dying” industries have no choice but to return capital to shareholders because they can’t with a straight face argue it would make sense to go out and add capacity / invest into the business.

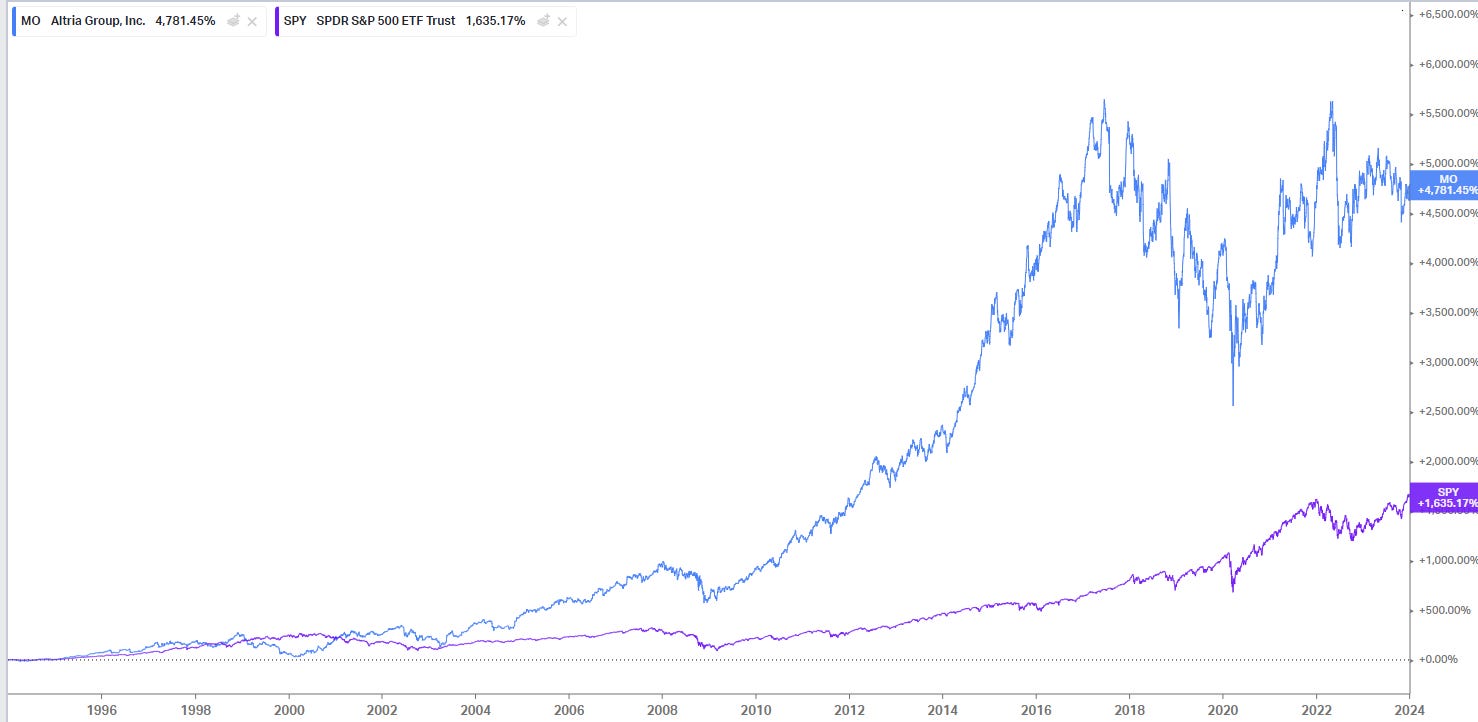

And, as sunsets go, tobacco and coal have certainly had beautiful sunsets.

Tobacco giant Altria’s (MO) up a casual 3x on the index over the past 30 years (and more if you go back even further; if you had bought a few thousand shares of MO stock in the 70s you’re likely reading this post from your own private island)…..

While coal has made a lot of people very rich over the past few years (including a very passionate and somewhat degenerate fintwit crowd, many of whom I’m friends with so I do say “degenerate” with love).

Anyway, there are all sorts of reasons a company might trade for a cheap multiple, and I’m not saying to go out and just YOLO every company trading for 1x earnings (I’d never seriously say to YOLO anything; I’ll go ahead and include a link to the legal disclaimer to remind you not to YOLO!).

But companies trading for low multiples make for a very fertile fishing ground; if you can correctly find ones that trade for super low multiples and will have their earnings hold up just a bit longer than the market expects, you can make a fantastic amount of alpha.

So that’s the why of the series. As far as what industries the series will cover and how I’ll write the series…. well, you’ll just have to wait for the first post in the series to come out later this week!

See ya then.

I found this recently with banks. Until a few weeks ago there were some regionals with stunning earnings growth and conservative asset-to-equity ratios with PEs of 5. There are still many at 8, which is still an attractive ratio to me. I think a lot of investors are still scared after the SVB fallout, and maybe to a lesser extent 2008.

Any good books you would recommend on investing in cyclicals?