Premium Post: Not a fit for ETFs, this company is well oversold

A summary given time sensitivity.

Note: I expect to have a longer write up of this idea in the near future; however, the idea is somewhat time sensitive and it’s one of the better forced selling opportunities I’ve ever seen, so I wanted to put something out on it now while it’s at its most timely.

Kontoor Brands (KTB) is a company I’ve followed closely since their spin-off last year; I’d encourage you to read the write up for a fuller background, but the basics are that Kontoor had all the markings of a alpha rich spin: the company had been under-invested in by a larger corporate parent prior to spin, the spinoff was extremely small compared to the spinner (creating some forced selling opportunities), etc.

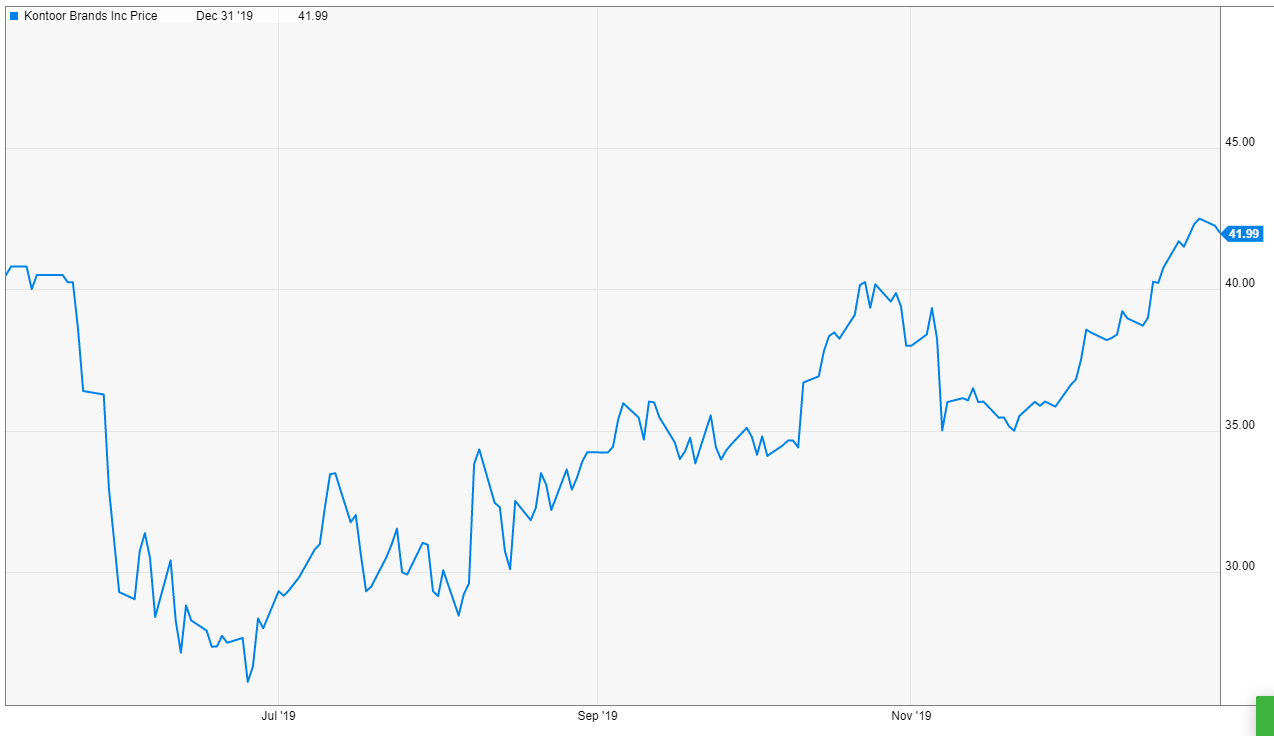

The spin played out about as expected: the initial spin created a bunch of forced selling, sending shares down to the low $20s. After the forced selling and spin dynamics passed, shares traded up to the low $40s by year end, roughly where I would peg fair value.

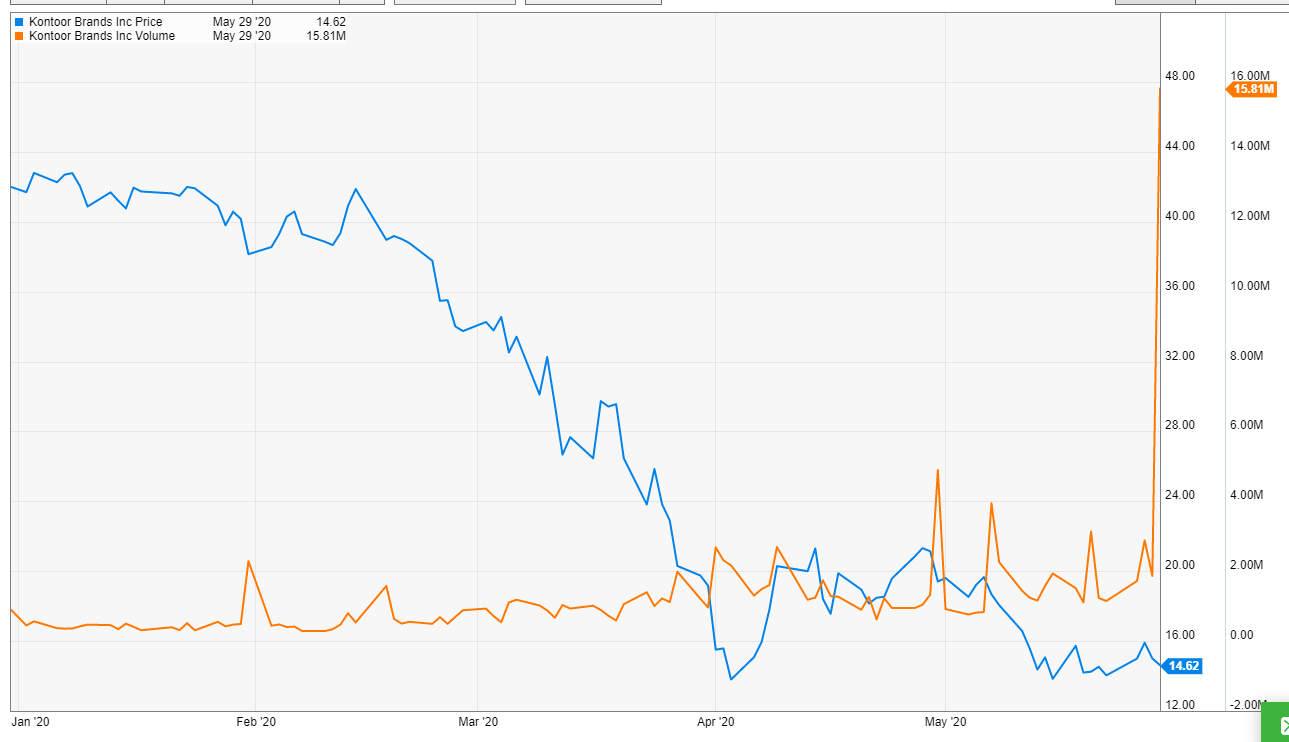

Let’s fast forward to today. Shares have been absolutely hammered so far this year, falling by ~66% (from ~$41 to ~$14). In fact, KTB is one of the few stocks yet to recover from the lows of March, with KTB’s shares retesting the March lows several times this month.

What gives? Well, notice the chart above includes both share price and volume (the orange line), and KTB’s volume has absolutely spiked over the past few days, culminating in a mammoth ~16m shares traded last Friday. That’s an enormous amount; KTB has just 58m shares outstanding, so on Friday alone more than 25% of the company traded hands.

That’s an enormous amount of volume, and there’s a reason for it. The S&P Dividend ETF (SDY) owned just shy of 20% of KTB. In response to Corona, KTB cut their dividend, and the dividend cut meant SDY needed to sell all of their KTB shares.

Plenty of people knew SDY would be a forced seller and likely front ran that selling, creating pressure on KTB’s shares (here is one example) of someone speculating a “short KTB in front of SDY” trade.

With SDY now out of the stock, I’d expect the selling pressure to have fully subsided, and over the next few days/weeks/months KTB’s shares can trade more normally.

What is “normal trading” for KTB? Well, if you believe their normalized earnings a few years out look something similar to what they earned in 2019, this is a ~$50/share stock. That could be conservative; KTB’s 2019 earnings were hamstrung by the bankruptcy of Sears. While there will be plenty of retailers going bankrupt in the short term, KTB was also gaining some retail distribution (likely because the company was much more focused out of a larger corporate umbrella).

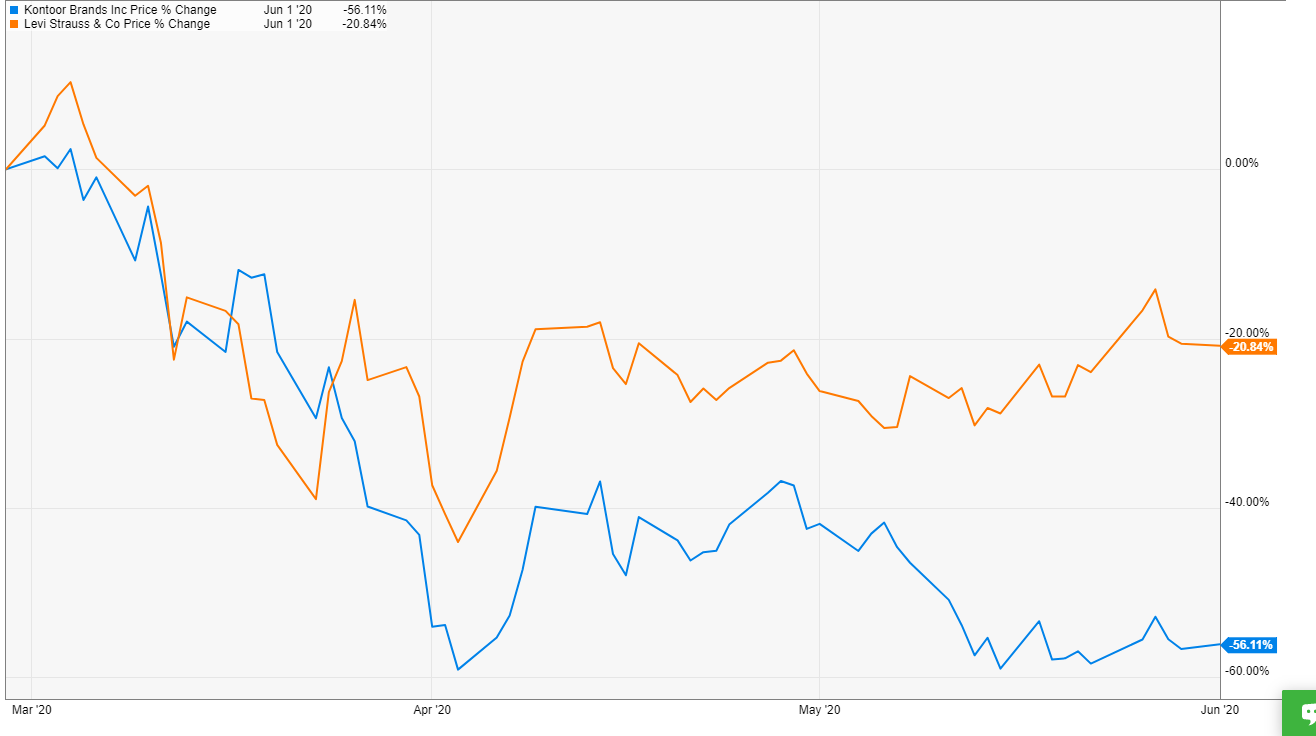

LEVI isn’t a perfect peer for KTB, but it’s close. KTB has underperformed LEVI by ~35% over the past few months. I can’t see of any reason why; LEVI actually reports off cycle so we have more up to date information for KTB than LEVI (and KTB continually discussed green shoots on their earnings call). If you think KTB should have traded roughly in line with LEVI, this is a >$25/share stock in the near term.

So, in the super short term, I think there’s a catalyst from KTB losing all the selling pressure from people front running the divdend ETFs. In the longer term, I think there’s a catalyst from KTB’s sales/earnings normalizing. There’s also a medium term catalyst here: dividend reinstatement.

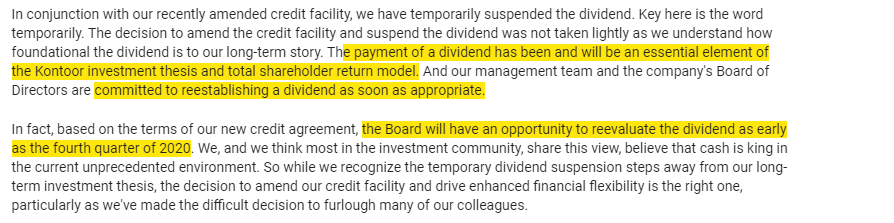

KTB has consistently made clear they are a dividend focused company. When discussing the dividend cut, the company explicitly stated they planned on turning the dividend back on as soon as they could, and suggested that could be as soon as Q4 (below quote from their Q1'20 earnings call).

I’m generally pretty dividend agnostic, but the restablishment of a dividend could create a catalyst on the back end. Once KTB re-estabilishes the dividend, a lot of the funds that were forced to sell this month will likely re-add KTB, creating some buying pressure that could send shares higher.

Again, I’ll have a more fully fleshed write up posted in the next few days. But I actually thought the dividend ETF would bleed out their shares throughout the month of June, not dump all of their shares at once, so I wanted to post something now while the idea is at its (likely) most timely.

PS- one last note. There was a small insider buy in mid-May. It’s only one director and it’s nothing crazy, but figured it was worth pointing out given it’s a somewhat nice size and it was purchased post dividend cut.