Tegus sponsored deep dive #1: Cable (part 3: fixed wireless)

This is part 3 of my deep dive into cable threats (sponsored by Tegus). This part will dive into the risk fixed wireless poses to cable. If you’re looking for background on what this series is and why I’m doing it, please see part 1 here. You can find part 2 on FTTH risks here.

Before we get to part 3, let me again highlight the three Tegus expert calls I used for the foundation of this series. Most Tegus calls are behind paywall, but for the next year, these links should give you access to the calls even without a Tegus sub, so it’s a great trial even if you’re not a sub! The three calls are:

So, that out the way, let’s dive in…. but actually, before we do that, let me give you my tl;dr version: fixed wireless represents the ultimate bear case for cable… but it’s represented the ultimate bear case for 20+ years, and it’s never come to fruition because simple physics suggests a wired connection to your home / office / wherever you use data most will always be the cheapest, lowest cost, and most reliable way to access the internet. Nothing I’ve learned recently has changed that thought.

So, that out the way, let’s actually dive in now.

First, I want to quickly define fixed wireless. Fixed wireless for our purposes means using a wireless network in order to deliver home broadband. In part 2 of this series, I discussed FTTH and noted that in most markets, you’ll have two competitors for home broadband once FTTH plays out: your cable provider and the fiber provider. Fixed wireless has the potential to change that; anyone with a mobile network could theoretically offer a fixed wireless product in markets they have spectrum / coverage.

So I wanted to save the fixed wireless discussion for after FTTH for two reasons.

T-Mobile is running the hardest at fixed wireless, and they reported earnings Wednesday afternoon (February 2), so waiting till now let me grab any updated nuggets from their earnings call

FTTH competition is the most likely bear case for cable in the near to medium term… but, in the long term, fixed wireless competition represents the uber bear case for cable, so presenting FTTH first and then building to fixed wireless makes sense.

Let me dive into point #2 a little further: at its most extreme, fixed wireless is the uber long term bear case for cable. Why? Well, I detailed in part 2 how the FTTH risk was real but manageable because it involved taking some of cable’s monopoly markets and turning them into duopoly markets that should split 50/50. Basically every market in America has 3 wireless players (T-Mobile, AT&T, Verizon); if fixed wireless was a complete cinch with no limitations then each of those wireless players could roll out nationwide fixed wireless offerings, and suddenly cable would go from having a monopoly or duopoly position in each market to facing 3+ competitors in every market. Even worse, cable is a regional business (the largest cable providers covers ~33% of the U.S.) while cellular is a national one, so cable would be a regional player facing 3 national players in every market (i.e. cable would get out scaled).

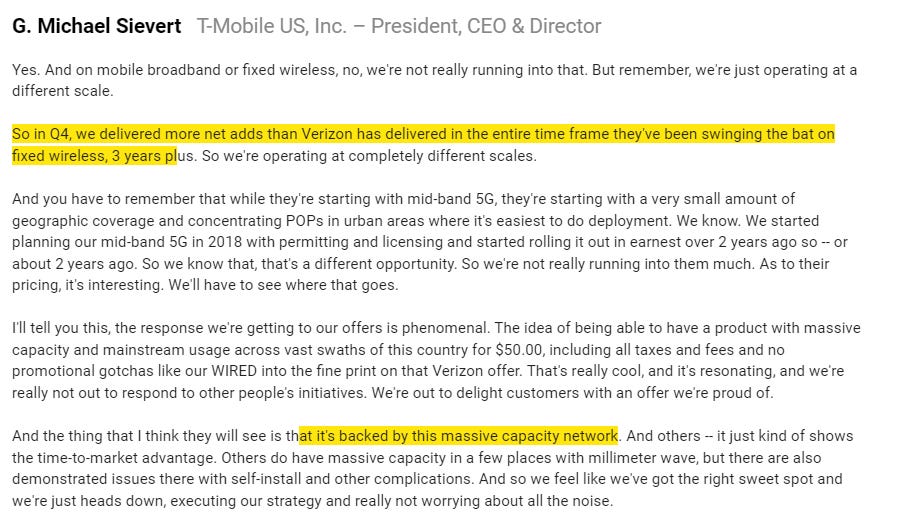

This is a particularly pressing concern now because we’re finally seeing a mobile company make real progress on a fixed wireless roll out. T-Mobile is currently the fastest growing high-speed internet company in America with their fixed wireless product, and they’re clearly planning on leaning into the product in the medium term. The quotes below are from their Q4 earnings call:

Those results are kind of crazy. Back in 2018, there was a freak-out among cable investors about Verizon’s fixed wireless offering. That offering has gone basically no where; as TMUS noted, in Q4 TMUS added more fixed wireless subs than VZ has in the >3 years they’ve been operating fixed wireless

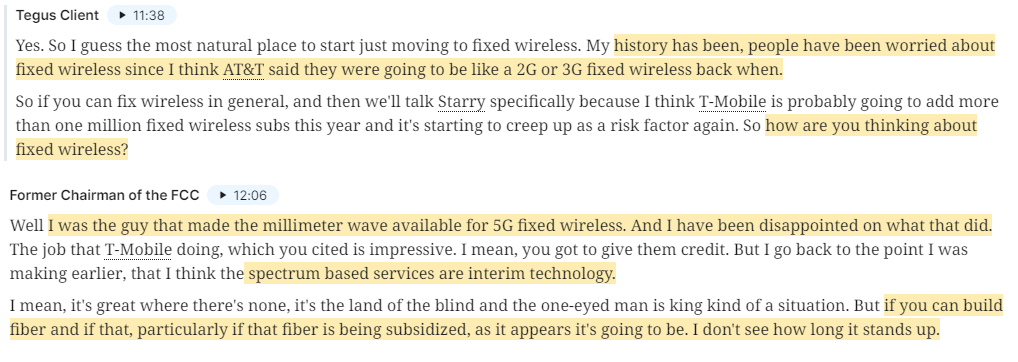

So TMUS’s rapid fixed wireless growth is a new concern… but fortunately for cable bulls, I don’t think that fixed wireless is a real long term threat to cable. There are lots of reasons for that belief, but a core reason is simple belief in physics: cable (and FTTH) have a wire directly into your home / office / the places where most data is consumed. That is always going to be the lowest cost, fastest, and most reliable way to deliver data. I liked how one of the experts framed it:

For years, wireless companies have talked about using their wireless network to attack home broadband (see, for example, AT&T WiMax in 2006 or Verizon Fixed LTE in 2011), but these products can never really take off because consumer demand for data usage continues to grow and wireless networks just can’t keep up with fixed networks. One of the experts had the same point of view in our calls; fixed wireless sounds nice and TMUS has done an impressive job on the initial roll out, but it’s always going to be fighting a losing battle against physical networks like cable or FTTH.

This viewpoint should come as no surprise to long time readers; I did a write up a few years ago on 5G fixed wireless as a threat and dismissed it, and I think that write up stands up well today and is worth revisiting.

In fact, if you revisit that 2018 post and then fast forward to today’s landscape, you’ll notice one critical difference in the landscape, and I think tracking that difference is instructive to fixed wireless today. What is that difference? It’s TMUS’s stance on fixed wireless.

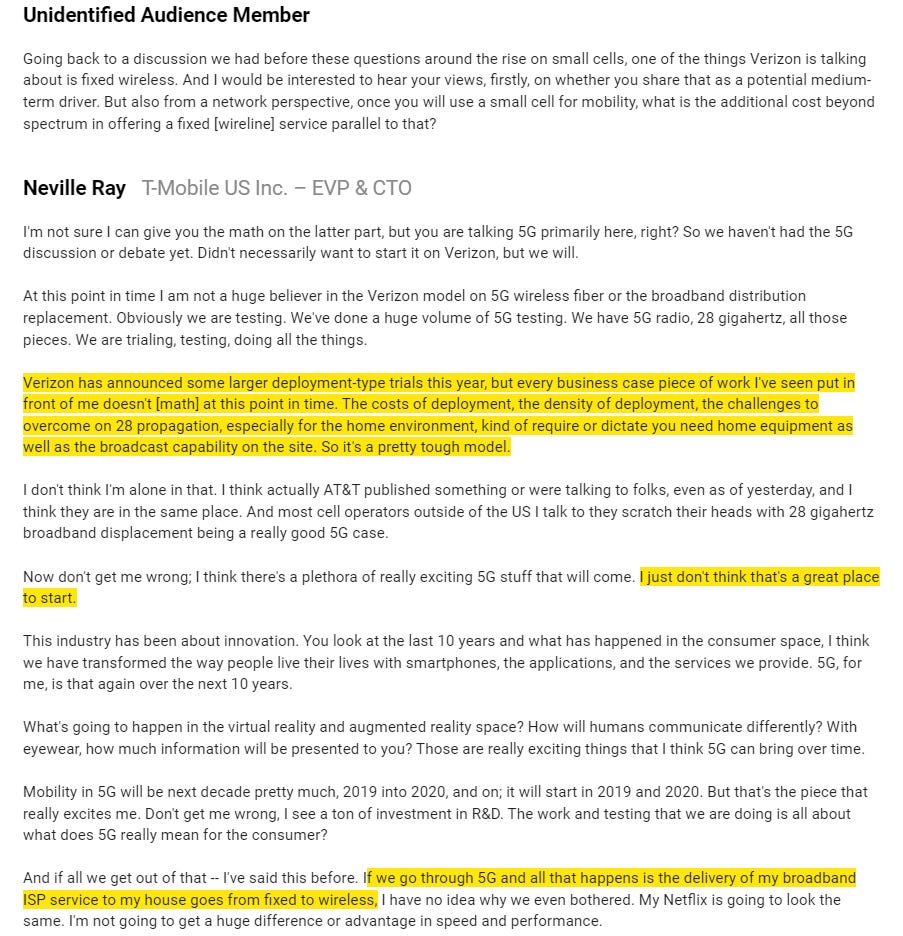

Back in 2018, Verizon was “alone” in rolling out fixed wireless over 5G, and both T and TMUS were downplaying the potential of 5G to support fixed wireless products. Today, TMUS is full speed ahead on a fixed wireless product (I mentioned in part 1 how TMUS added more high speed internet customers than Charter did in Q4’21). Verizon is still rolling out fixed wireless (though they’re a bit less gung-ho about it IMO), while T is still thinks fixed wireless generally doesn’t make sense (I’ll come back to that later).

I think tracking TMUS’s statements and evolution on fixed wireless is really interesting and can help illustrate why I don’t think fixed wireless is really a competitor for cable broadband.

So let’s go back to what TMUS was saying about in 2017 and how they were downplaying fixed wireless. Here’s their CTO talking at a conference back in 2017

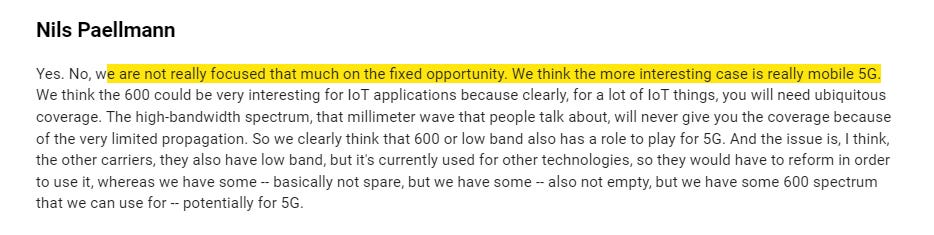

Here’s TMUS saying they’re not focused on fixed wireless as a 5G product later in 2017:

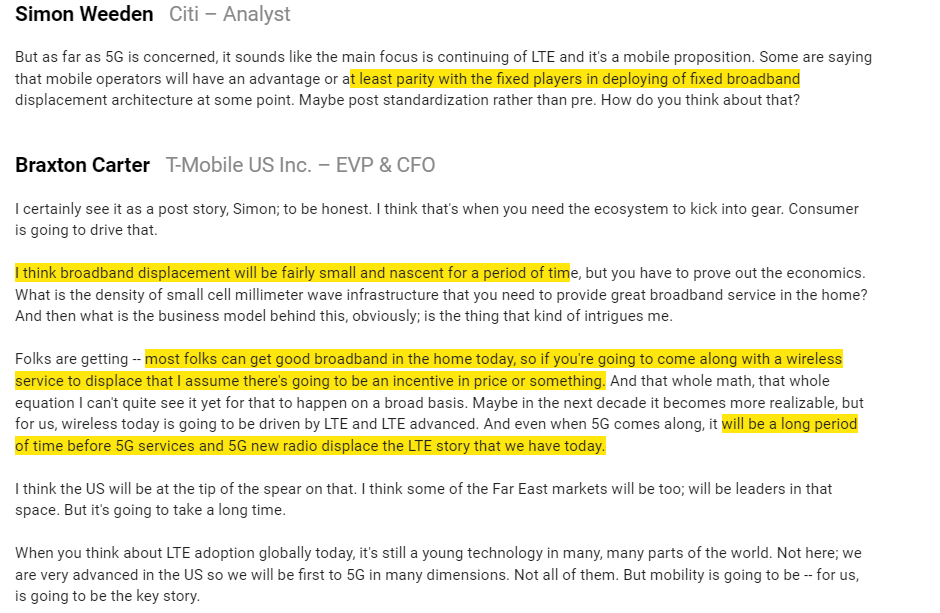

And here’s their CFO discussing how unexciting fixed wireless is for 5G given most people already have good broadband.

So in 2017 TMUS and T are pretty much joined at the hip in saying fixed wireless isn’t a great use case for 5G and that Verizon’s attempts to roll out fixed wireless are silly. I think that proved prescient; it took Verizon about three years to begin to see traction with their fixed wireless business, and even with that headstart they’re currently reporting lower fixed wireless adds than TMUS.

In 2018, TMUS announces a merger with Sprint. This is a huge deal for TMUS; it takes the wireless industry from 4 to 3 players and gives TMUS an enormous amount of excess spectrum. TMUS needs to sell regulators that a 4 to 3 merger (generally a no-no in antitrust; remember regulators blocked the T / TMUS merger earlier last decade) is ok, and they also need to figure out a way to quickly utilize all that excess spectrum. The solution is easy: fixed wireless broadband. Rolling that product out will please regulators (it adds a competitor to cable) and it chews up a lot of excess spectrum.

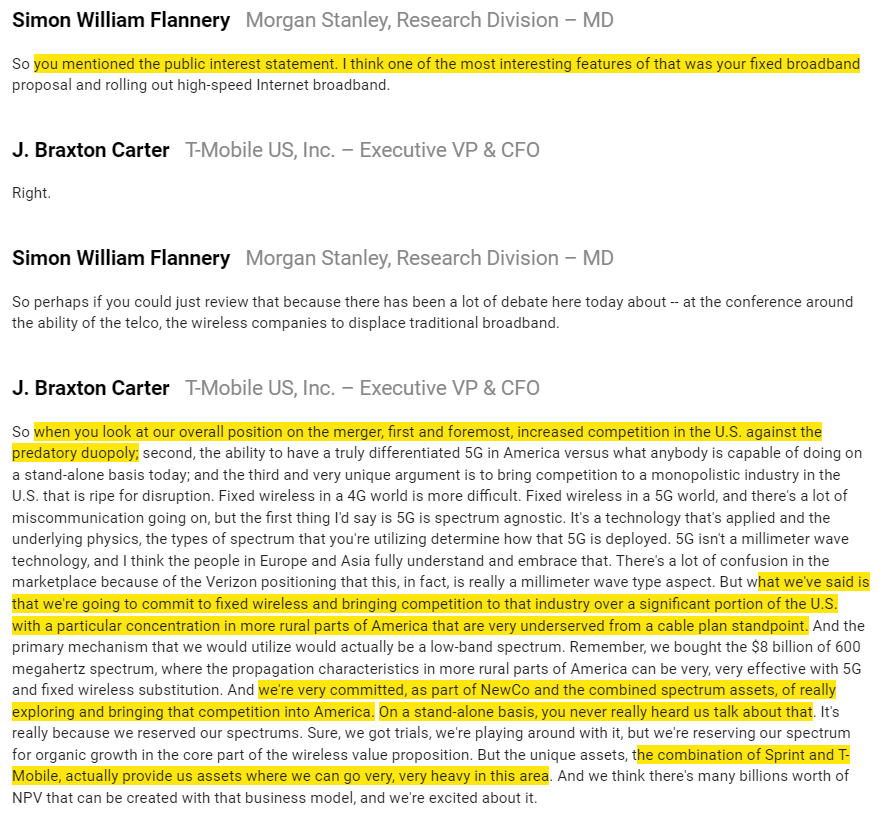

So compare the 2017 quotes above to how TMUS starts talking about their fixed wireless plans post merger (and note in particular that the first time they really start hammering that home is in their public interest statement (the thing you file with regulators for why they should let your merger go through)).

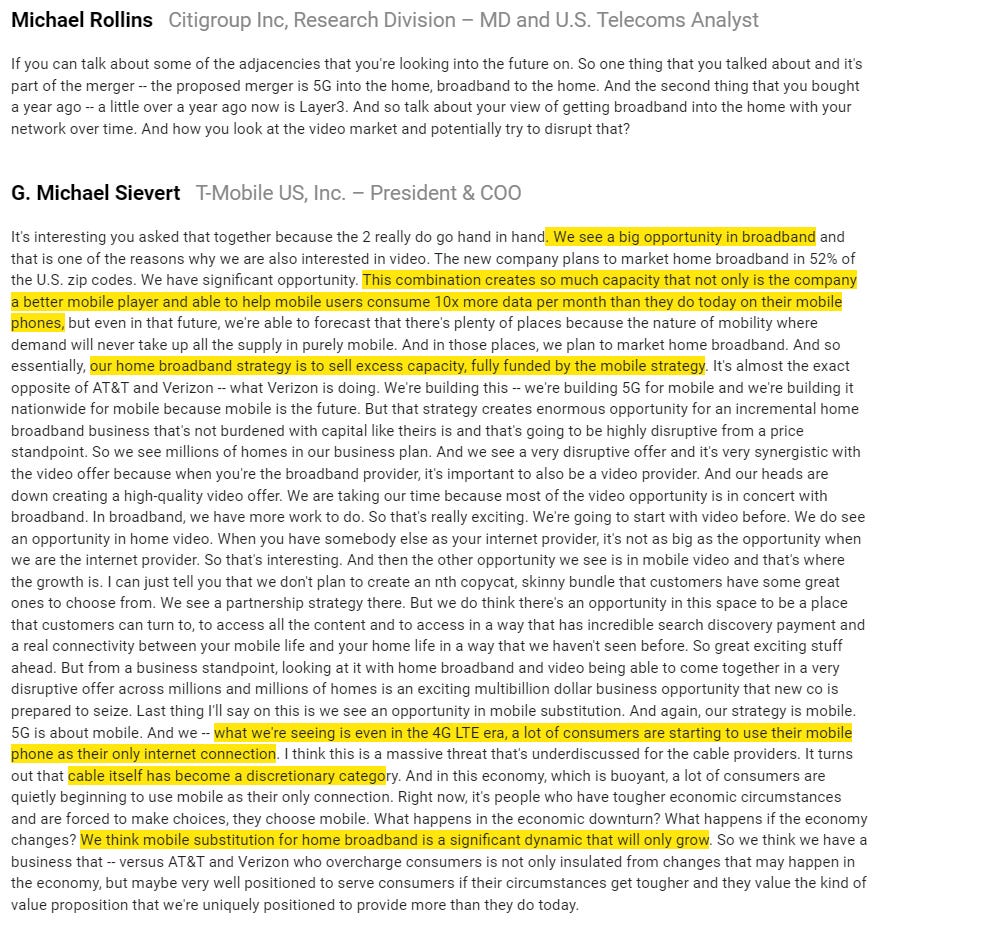

Or here’s another quote from 2019 on what TMUS sees for the broadband opportunity (note the “plans to market home broadband in 52% of the country; that’ll come up in a second).

So I think it’s pretty clear that TMUS’s tone on fixed wireless changes as soon as they announce the Sprint merger. Skeptics like me would suggest they are doing that just to get regulators to bless the merger and to make use of all the excess capacity they’ll have once they buy Sprint. I think cable bears would say, “hey, maybe T-Mobile was skeptical pre-Sprint, but the Sprint merger gave them so much excess capacity that it actually did unlock this fixed wireless opportunity that was unavailable / silly to them before.”

Why do I think I’m right and the cable bears are wrong?

Well, first the Tegus experts seemed to agree with me that TMUS only made this fixed wireless plans because it helped them get their merger through.

But diving deeper we can look a little closer at what TMUS is saying about fixed wireless now that their merger has been approved. Here they are at a conference in November 2021:

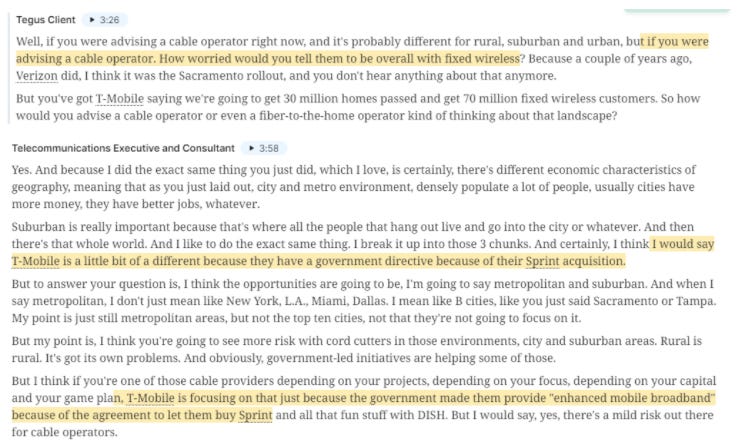

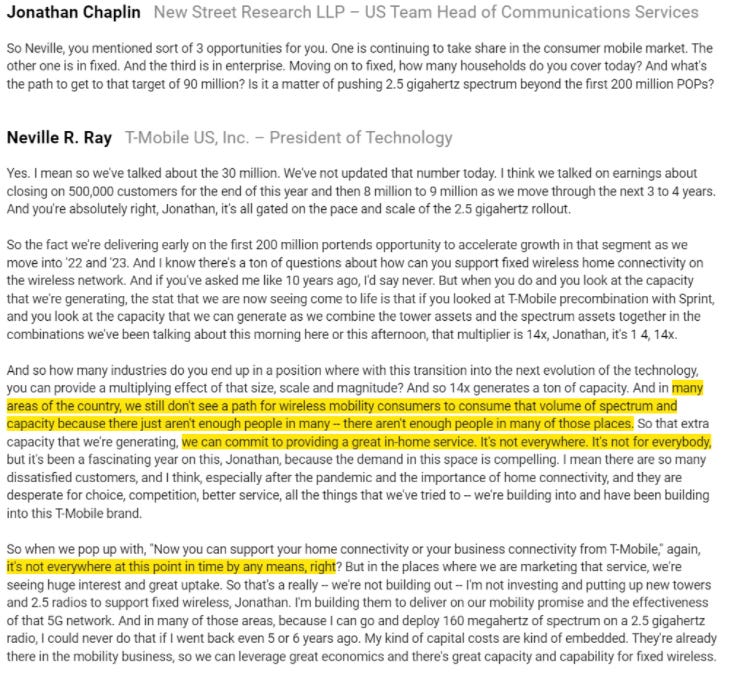

Well that’s a little different than what they were saying before their merger closed! When they were trying to get their merger approved, they were going to cover 52% of American zip codes with fixed wireless. Now the merger’s closed, and suddenly we’re talking about attacking 30m in the medium term and approaching 90m homes over time? And read that third paragraph closely; he’s basically saying “we have so much excess capacity after the Sprint deal, and in some places there aren’t enough people to consume it, and in those places we’ll provide home internet solution, but it’s really not for everyone”.

Or consider this quote from this conference:

Again, this isn’t the “we’re going to attack broadband everywhere” speech we were hearing from TMUS when the merger was under review. Suddenly this is, “we’ll offer this service strategically in places where we have excess capacity, and we’re planning to get single-digit penetration of our market.” Again, these quotes aren’t exactly brimming with confidence in TMUS’s fixed wireless plans.

We can also look at the actions of wireless companies instead of taking them at their word, and I think doing so reveals that they know the importance of local fixed infrastructure like cable.

Domestically, remember that Verizon tried to buy Charter back in 2017 (right before Verizon launched their fixed wireless product).

Over in Europe, there are lots of examples of wireless players buying cable players in order to compete in the broadband market and to leverage cable’s infrastructure to improve the wireless’s companies mobile offering. These deals always happen at a big multiple for cable because wireless companies know cable is in command and the cable assets are critical to any broadband future. My personal favorite example of this is T-Mobile Austria buying cable assets in late 2017. Why? Because it illustrates that T-Mobile knows that having deep, local fiber (like cable or FTTH has) is the key to the future telecom network.

But there’s one more really interesting place we can look: T-Mobile in Manhattan. Guess what they’re rolling out there for their broadband offering? Not fixed wireless…. they’re renting out fiber lines and rolling out a fiber service!

Bottom line: If you look at the actions and consider the motivations of the wireless companies, I think they’re telling you that they know fixed infrastructure like cable will remain the key way consumers will access the internet.

Let’s now zoom out: why is fixed infrastructure so important / why won’t fixed wireless work long term?

The answer is simple: broadband and data usage continues to explode upward, and that puts a huge strain on networks. Wireless networks don’t maintain extra spectrum / capacity for long because data usage continues to explode and it’s all they can do to keep enough capacity to keep their normal wireless operations running, much less start adding the huge data load that fixed wireless demands. I’ll refer you to one of the expert quotes I started this call with:

TMUS is in a unique spot here; their Sprint merger gave them a ton of excess capacity for now. They can use that to support a fixed wireless service (again, for now), but as data usage continues to grow the fixed wireless component is going to be less and less relevant.

The cable companies have frequently pointed this out. For example, Charter’s talked about how wireless companies are going to face a trade off between using their scarce resources (spectrum) to support either a fixed wireless product or add mobile subs.

Comcast says something similar; wireless companies are going to need to start making trade-offs between fixed wireless and their mobile business as data usage grows and the wireless networks fill up.

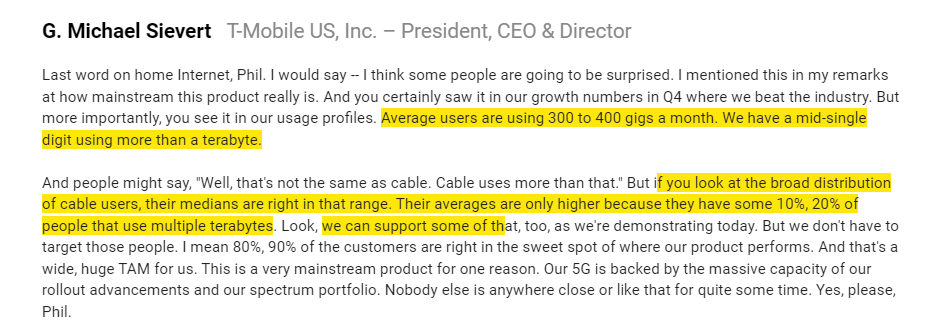

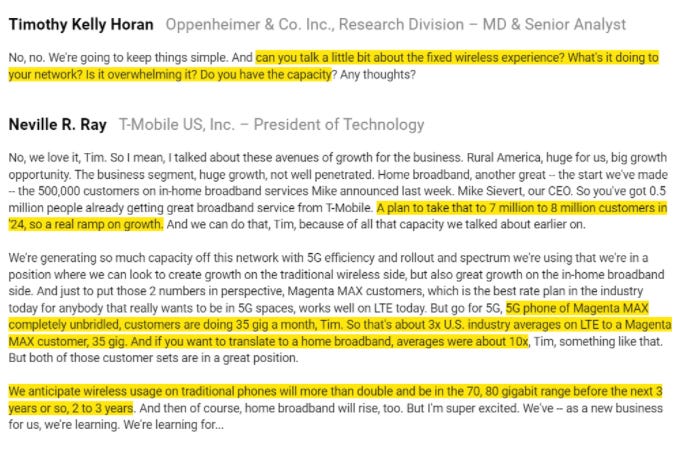

What is this trade off the cable companies are talking about? Well, the average mobile user consumes maybe 10 gigs of data a month, with high end users consuming ~35 gigs. That’s growing rapidly; TMUS expects the average user will consume ~70 gigs in a few years.

That’s a lot… but it pales in comparison to broadband users. TMUS in the quote above notes the average broadband user is consuming ~350 gigs, and it gets even higher for broadband users who stream video. Charter notes that the average non-video broadband user consumes 700 gigs a month, with 25% of users consumer more than a terabyte.

The price of a mobile line and a home broadband connection are roughly the same, but the broadband user consumes 10x or more the data. As data usage continues to grow and wireless networks continue to try to keep up, wireless networks will need to ask themselves one thing: do we really want to use our scarce spectrum resources to support one more fixed wireless user when we could instead use the same spectrum to support 10 wireless users (and generate 10x the revenue in the process)? This is the exact argument cable companies have been making against fixed wireless since Verizon first launched back in 2018:

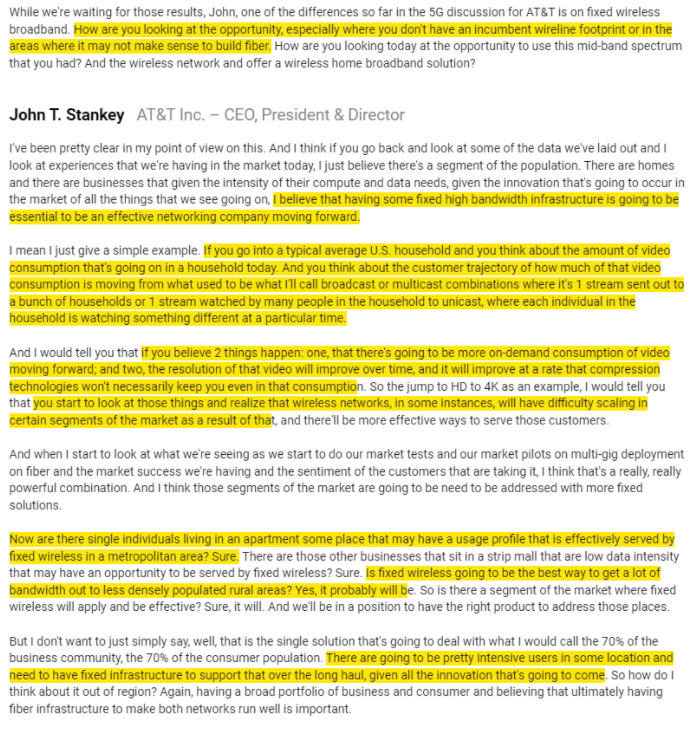

It’s not just the cable companies saying that. Check out the quote from AT&T below; everything they’re saying jives with what I’m talking about above. There’s a place for fixed wireless, but it’s really for places where you’ve got tons of excess capacity (mainly rural locations). Everywhere else, you need fixed infrastructure to handle broadband demands because data usage continues to explode and wireless companies will have their hands tied keeping up with the demands on their mobile network.

Humorously, AT&T seems to back this talk up with their marketing. When I googled “fixed wireless” this week, look what the top result was: AT&T “fixed wireless internet for rural households.”

What would make me wrong and suggest fixed wireless was a real competitive threat to home broadband over time? A couple of things would have to break right, but the main one is that for fixed wireless to really work you’d need to believe that consumers’ demand for internet data stops going up. I think that’s a really, really bad bet: our world is getting more connected, not less, as every device in our home increasingly has a smart or wireless component. And as things like 4k video or AR becomes more mainstream, data usage is only going to continue to go up.

I think you can see hints of where data usage is going in the CHTR “25% of our customers use more than a terrabyte” discussion above, but just to quantify how fast data usage continues to grow let’s check out what ATUS discloses.

In Q4’19 the average ATUS household consumed more than 300 gigs/month, up 20% YoY.

Fast forward to Q2’21, and the average ATUS customer is doing 445 gigs/month, with broadband-only customers consuming 600 gigs.

That’s explosive growth, and (again) I don’t see that slowing any time soon.

I want to wrap this post up here, but there are two things I didn’t hit perfectly above that I want to hammer home.

A lot of this analysis presupposes that wireless networks don’t have insane amounts of excess capacity lying around where they could just randomly handle a huge influx of data usage that fixed wireless would entail. I don’t have any great quotes that prove that (shockingly, wireless executives don’t go to conferences and say “our network is hanging on by a thread! Please, everyone, stop downloading so many cat videos!”), but I think it’s pretty evident. Wireless networks will throttle you down if you consume too much data, and every time spectrum comes for sale the wireless companies trip over themselves to spend billions to snatch it up. Those aren’t the actions of companies swimming in excess capacity.

A wireless network is basically a huge amount of fiber that runs to a big tower and then broadcasts to your phone. A cable network is basically a huge amount of fiber that runs close to your home, then connects via coax to a wifi router that broadcasts to your phone. Eventually, these worlds will converge; the critical thing to have is tons of fiber super close to the consumer. And cable is in pole position with that.

Anyway, this post ran crazy long, but I hope it was helpful in assessing what’s going on with fixed wireless and why it won’t be a huge concern for cable in the long term. As always, my inbox and DMs are open if you think I missed something / I’m misreading something.

I’m looking forward to seeing you next week for the final parts of this series (discussing Starry, Starlink, and some closing thoughts).

Fantastic and helpful as always

Hi my card was charged although I did not want to subscribe, can you please refund the charge.