The "broken market", evolving your process, and Munger's self-pity

The older I get, the more respect I have for Charlie Munger (and I was starting from a pretty high respect level!).

I realize I’m not exactly in a contrarian on respecting / admiring Munger, but my respect went up just a tad when I saw this quote from Munger on self-pity1:

Generally speaking, envy, resentment, revenge, and self-pity are disastrous modes of thought. Self-pity can get pretty close to paranoia. Paranoia is one of the very hardest things to reverse. You do not want to drift into self-pity. I had a friend who carried a thick stack of linen-based cards. When somebody would make a comment that reflected self-pity, he would slowly and portentously pull out his huge stack of cards, take the top one, and hand it to the person. The card said, “Your story has touched my heart. Never have I heard of anyone with as many misfortunes as you.”

Remember that Munger lost both an eye and his 9-year old son; those are absolutely devastating hits. It would have been very easy for Munger to get one of those self-pity cards and feel like he actually deserved it!

Anyway, I saw that Munger quote right around the time a friend sent a series of tweets out about market structure. Basically, the tweets asked “how much do you think market structure has changed over the past few years” and “how much have you attempted to iterate your process in light of market structure changes?” My friend’s answer was “market structure has changed a lot” and “my process has changed and should probably change a bit more.”

Why did that tweet make me think of Munger and self-pity?

Because the markets are a competitive, dynamic place that are always evolving. A strategy that worked 100 years ago probably won’t work today, because any easy winning strategy in a competitive game will get arbitraged away.

I think a sports analogy will actually illustrate my point well. Moneyball is a really well known story thanks to the Michael Lewis book; it’s got lots of interesting anecdotes but the high level of the book2 could be summed up like this: in the 2000s, a wave of mathematically minded GMs came into baseball. To them, baseball was an excel spreadsheet. A lot of old school managers mocked the new math; sometimes the excel spreadsheet would say that the fat, slow first baseman was a better player than the handsome, chiseled short stop… surely the mathematicians were joking!

Of course, the mathematicians were generally correct, and soon the mathematically minded teams were destroying the old school GMs. The old school GMs had two choices: adapt or die (metaphorically!).

Basketball might illustrate this point even better. In the late 2000s and early 2010s, there was an explosion in the 3 point game as teams increasingly discovered the simple math of “three is greater than two.” Old school GMs, coaches, and players decried this trend, perhaps most famously when legendary coach Phil Jackson made a tweet during the playoffs mocking the three point game / focused teams. But the math and results were clear: players and coaches could either adapt to the trend (shooting more threes), or their teams would lose (the 25 most efficient offensive seasons of all time have all happened within the past 5 years, with basically all of the top 10 coming this season or last. Good luck competing with that offensive explosion using old school strategies!) and they would be out of the league.

To bring this back to investing, the game (i.e. the market) has evolved. In baseball ~30 years ago, you might get an edge by saying “hey, we really care about players getting on base, no matter how they get there. What if we value players with on base percentage instead of batting average?” because almost no one was doing that! Similarly, when Ben Graham wrote Securities Analysis ~100 years ago, almost no one was doing fundamental analysis; simply using basic fundamental tools (like calculating book value or price to earnings) was an enormous edge! Today, there are hundreds of billions of dollars devoted to quantitative models trading on fundamentals; an investor pulling up a 10-K, cracking open excel, simply calculating the price to earnings of a company, and saying “this is really cheap; I’ll buy it” is no longer enough to generate a competitive edge / alpha in the long run.

There are two possible approaches an investor can take to the market evolving: the anti-Charlie Munger approach, or the evolutionary approach.

The first approach you can take to the market evolving / getting more competitive is the anti-Charlie Munger approach. It’s one I see on Twitter frequently (or, if I’m honest, I’ll see it in myself sometimes!). It’s a self pity approach where you loudly complain that passive / index investing has broken the market and turned it into a casino. With this approach, you basically yell “market is BORKEN” as loud as you can nonstop while sticking to the exact same investing strategies that worked in the 90s and 2000s and constantly underperforming.

Obviously, I’m not a big fan of that strategy…. but I’d like to note that, whether the people who are yelling at the market realize it or not, it is a strategy! If you’re yelling about the market being broken and sticking to the same stocks / strategies that worked decades ago, you’re effectively betting that the current market structure is a bubble / wrong, and will unwind in time. And there is precedent for that strategy working; a lot of today’s famous value investors made their name in the late 90s / early 2000s by being long deep value stuff that was getting ignored in favor of growthier dotcom stuff. When the dotcom bubble unwound, the indices suffered for years because the dotcom stuff had become such a large percentage of the index, and a lot of value investors smashed the indices as their unloved / beaten down value stocks gained while the indices were destroyed.

Heck, you don’t even have to look back that far to see some evidence this strategy can work; in 2022, all of the indices got destroyed as growthier stuff was hammered, but a lot of “hard asset” investors performed really well as energy and coal and some other cyclical stuff had banner years.

So that “woe is me” strategy can work…. but I again wanted to emphasis that investing like that is a conscious choice and a strategy. Screaming “market is broken” and only investing in stocks trading under 5x P/E is making a conscious choice that the market will revert at some point. After all, if you think the markets are broken and will be forever, you could generate easy alpha by going with the flow and just buying the things that benefit the most from passive flows! Again, if the market is permanently broken, then you would have yourself a winning strategy there! By continuing to invest the “old school” way that is not working, you’re betting that the market will correct at some point and that correction creates an alpha opportunity to stick with what isn’t working!

The second approach an investor can take is an evolutionary approach. In this approach, I think an investor maintains their principles (i.e. I am a value investor trying to buy undervalued businesses) but updates their strategies to apply those principles in a way that works for the modern market.

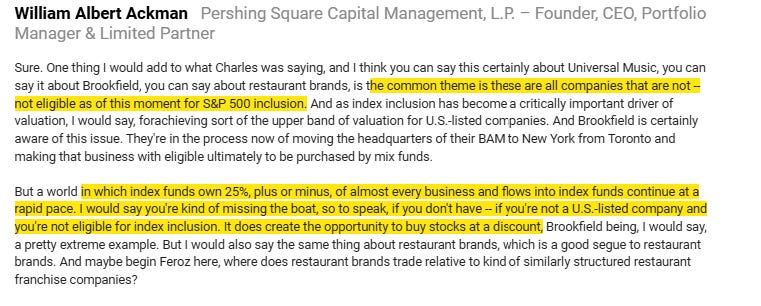

For a very simple example of this evolution, consider this line from Pershing Square’s Q3 earnings call:

Ackman could complain “all of the index stocks are perma-bid and way overvalued.” He could complain “all of my stocks never catch a bid because they’re not in the index.” And perhaps he is doing a bit of that….. but he’s also working with what the index is giving him: he’s buying stocks that are cheap because they are not in the index, and then looking to grab a catalyst / multiple tailwind when they join an index. What’s interesting is that, given Ackman’s size, he has a few ways to get a company into an index3: the company can chose to do so on their own, Ackman can buy a stake and convince the company to do so, or Ackman can own enough / exert enough control that he can force the company to relist (like he’s doing with UMG).

Of course, that’s just one example of taking the current market environment and using it to create opportunity, and there are plenty of other ways to try to use the new market structure to create opportunity. For example, U.S. listed stocks tend to trade at much stronger / higher multiples than international stocks; rather than bemoan that fact, a popular strategy among some of the best international investors I know is buying cheap international stocks that have large domestic businesses and working with them to relist to the U.S. in order to capture that value multiple (A perfect example of this is Voss Capital’s thesis / strategy on CRH I mentioned in this post).

And the conclusions on how to take advantage of the current market structure don’t have to be the same investor to investor. In fact, looking at the same information, many investors will come to different conclusions on what works in today’s market. For example, I know some investors who think investing in something with a hard catalyst is more important than ever in today’s market…. while I know others who think that anything with a potential catalyst gets picked over / bid up, and the most alpha is in buying things that don’t have a visible catalyst because real catalysts often come out of nowhere and things without visible catalysts trade much, much cheaper than things with a catalyst.

So every investor does not have to come to the same conclusion on how to compete and evolve in today’s market. What I think is most important is being flexible and making sure your evolution matches your principles / skill sets. As I write this (November 25), the stock market is clearly having a bit of euphoria for AI and crypto plays. If you’ve been a deep value guy for 10 years, it would be weird to suddenly become a momentum based day trader. That’s gambling, not evolving your process while sticking to your principles! But I think it’s entirely consistent with evolving / adapting to the market to say “hey, I’ve been a deep value guys for years…. but my best performers have had some type of catalyst, so I need to focus a little more on things with a catalyst” or “I’ve sold my winners the moment they stopped being deep value, and in hindsight my performance would have been better if I hadn’t been rigorously married to selling things the second they weren’t dirt cheap; maybe I need to give my winners a bit of a longer rope”.

The unfortunate fact is that any game worth playing is always going to be evolving / getting harder. And, with literally trillions of dollars on the line, the market is the ultimate evolutionary game where you have to evolve and adapt your strategy or you will get left behind. It’s easy to fall into self-pity…. but I think a better approach is to continue to adapt, evolve, and find new ways to try to outperform the market.

Do you have any ways that you’re evolving / improving your approach to respond to the market? I’d love to hear them if you do (you can leave a comment and/or shoot me a note)!

PS- One of my biggest concerns as a fundamental / human investor is that AI will eventually replace all of us the same way computers / factor investing has largely replaced the breed of investors who used to outperform by simply buying net nets or things that were quantitively cheap. So I’m always looking for ways to think about AI in investing, how to incorporate it into my process, and how to take advantage of any opportunities or blind spots it creates. I’ll have a little more to say on it later this week, but I’m going to the AlphaSense “How AI is Revolutionizing the Investment Landscape” conference next week; if you’re headed there, shoot me a DM and let’s meet up (and, if you’re not in NYC, the event will be livestreamed for free if you’re interested).

PPS- It’s not a clean fit, and there were obviously a lot of other things it had going for it…. but I find Buffett / Berkshire’s evolution with technolgoy investing really interesting when thinking about this self-pity mantra. Buffett / Berkshire’s first big tech investment (at least that I can recall) was IBM, and it was a disaster…. but that didn’t stop Berkshire from buying Apple a few years later, and that’s been one of the most successful investments of all time! Again, not a perfect fit to this, but I do think there are lessons on evolving / sticking to your principles in Buffett growing into a “tech investor.”

PPPS- My friend concluded his tweet on market structure with his belief that “The market had changed a lot” and his process “had changed somewhat but needed to change more.” My answer would be the market has changed quite a bit, but moderate changes to the process are probably the right answer (in fact, I think saying “I’ve changed a bit but I probably need to change just a bit more” is probably right around optimal!). Again, you need to evolve, but you want to make sure you stick you your core principles, and wholesale changes probably veer too close to “changing your principles” versus “evolving your process.”

This quote made its round on social media; I apologize I cannot find the original tweet that I saw it in!

I’ll admit I read the book like 15 years ago, so it’s possible my memory is fuzzy but I feel directionally correct!

I’m assuming the company is of sufficient size and everything already, and is included from the index for some other reason (i.e. international headquarters). Obviously Ackman can’t jam a $100m company into the S&P 500 through pure force of will!

Well written and thought provoking article. The market is changing faster than it used to. Just like a lot of other things good and bad. You are correct that adaptation is key. On a separate note, I wonder how AI will impact things including swing trading. I expect it will make dinosaurs out of a lot of people's strategies including some I use now. Happy Turkey Day! I look forward to reading your posts in 2025.

Hi Andrew great piece! I am currently struggling with this situation right now but your writing encouraged me to move away from dogma-like thinking which eventually leads to self-pity when things don't go your way. Charlie Munger once said that "all investing is value investing" and you your articles explains this well. Looking for value in different ways doesn't make you less of a value investor, instead we are trying to understand and analyze a company in various lenses.