Weekend thoughts: Was Nvidia a value stock a year ago?

I had a few discussions about “value” investing this week.

There is always something funny about discussing value investing; I tend to find that investors who are more focused on just marketing / raising assets and less focused on actually outperforming can be much more rigid / dogmatic in defining value investing. “That stock isn’t a value stock; it has negative earnings.” “That stock isn’t a value stock; it doesn’t pay a dividend!”. Etc.

Anyway, the topic of “value investing” came up in a few discussions this week, and there’s a question that’s been tickling the back of my mind that I’ve been wanting to answer:

Was Nvidia a value stock ~a year ago?

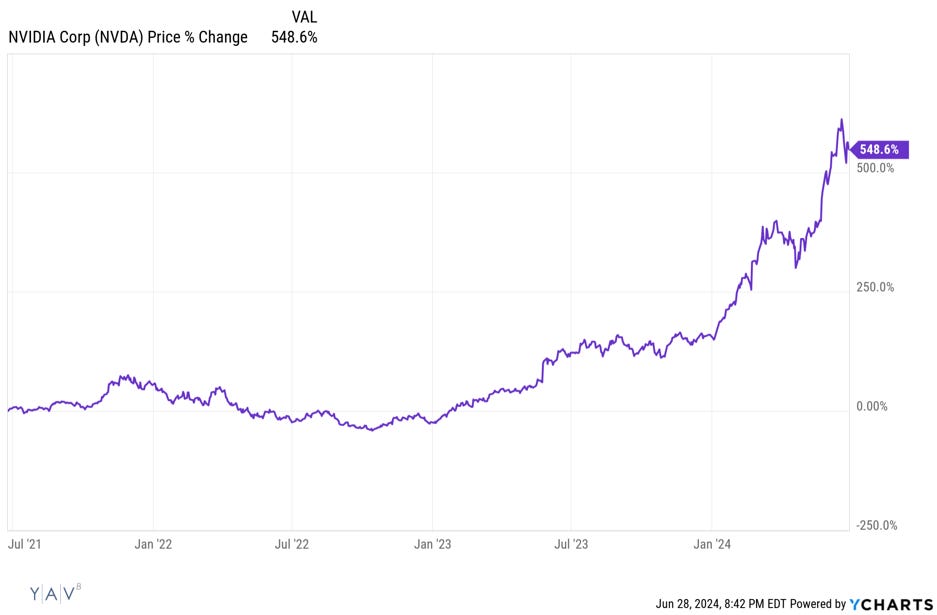

With the benefit of hindsight, I think we can say the answer is clearly yes. NVDA’s stock is up ~5x over the past few years, with most of that coming in the past 6 months. If value investing is buying something for less than it’s worth, than NVDA was clearly a value investment a year ago.

And (again, with the benefit of hindsight), the numbers clearly back up that NBDA was a value investment a few years ago. In January 2023, NVDA’s market cap and EV were both ~$500B. This year, NVDA is getting projected to do ~$80B in EBITDA and ~$60B in FCF, and their revenue is doubling YoY. So if you were buying NVDA around in early 2023, you were buying them for just over 6x EBITDA and 8x free cash flow while their revenue was doubling. Even the deepest of value investors would probably be able to stomach paying a mid-single digit multiple for a business growing 100%/year.

Of course, all of that relies very powerfully on the benefit of hindsight. In late 2022/early 2023, analysts only had NVDA doing ~$17B in EBITDA this year (FY25). So, at $500B EV, it looked like you were paying ~30x two years out forward EBITDA for NVDA….

And analysts were only projecting ~$40B in revenue, which was solid growth off their ~$27B FY23 base but… I mean, the current projections are for $80B in EBITDA on $120B in revenue. Analysts were projecting $40B in revenue just a year and a half ago! That is just absolutely insane; EBITDA is going to come in double the original revenue projections! And that’s all organic; it’s not like NVDA did a huge deal to distort the numbers.

So here’s my question: what would it have taken for someone to have considered NVDA a value stock 18 months ago (outside of a crystal ball)?

I think the answer is incredibly deep industry expertise plus a conviction that AI was inflecting…. but (and I could be wrong) I suspect even the most bullish analysts wouldn’t have seen this coming. They would probably have told you that NVDA was undervalued because it was going to grow faster than projected, and their chips would be more in demand and moat-y than the average analyst thought…. but I don’t think anyone who was buying NVDA at a $500B EV a year or so ago was doing so because they thought they were getting it for a single digit EBITDA multiple!

I think it’s really easy to talk about value like it’s some hard coded metric in a spreadsheet. Something is a bargain because there’s some firm, quantitative number that says it is. This stock is undervalued because it trades for a single digit earnings multiple, or it has a high dividend yield, or it trades below book value.

And there is certainly some appeal to all of that.

But, increasingly, I am more interested in the Nvidia in early 2023 type of value; something that’s a bargain not because the numbers look cheap but because there’s something unique about the business or the assets that you can only understand if you really dig deep. Or that something is a value not because it trades at 90% of book…. but because it trades at 90% of book and book is understated by 50%, or because it trades at 90% of book when it really deserves to trade for 900% of book.

Finding that type of value is hard, but, when you do, it tends to be where the real big bucks are made.

Just a thought that’s been floating around my mind this week. I’d love to hear your thoughts if you think I’m misguided (and, of course, I’d love to hear your thoughts if you know anything that’s NVDA 18 months ago undervalued!).

You have a point. This is a really useful weekend thought post :). Thank you.

I explore this in phenomenon in more detail, drilling down into real numbers and the math behind the investments in two Substack posts that I published recently - my conclusions are similar to yours, essentially "Not All Cheap Stocks Are Cheap, Not All Expensive Stocks Are Expensive":

1. https://rockandturner.substack.com/p/lessons-in-growth-stock-valuation

2. https://rockandturner.substack.com/p/value-investors-are-barking-up-the