Some things and ideas: September 2018

Some random thoughts on articles that caught my attention in the last month. Note that I try to write notes on articles immediately after reading them, so there can be a little overlap in themes if an article grabs my attention early in the month and is similar to an article that I like later in the month.

Customer Utility / Surplus as a source of hidden value

In last month’s links post I mentioned the “offline to online” advertising trend as a place where I saw the potential to find hidden value. (Here’s another article on online to offline; I particularly like the way Eloquii describes stores as “shoppable billboards”)

Another “hidden value” source that I’ve been thinking about is companies that generate consumer surplus. What got me thinking about this a little bit more is something Warren Buffett said about Apple. Right towards the end of that interview he mentions the enormous consumer surplus from buying an iPhone (the anecdote he uses is an iPhone costs $1k but he would get more utility from it than the $1m he spends on his private plane).

I fully agree with Buffett on that thought (iPhones are underpriced relative to utility), but here’s the issue with using consumer surplus as a source of hidden value: it would suggest you buy almost every consumer focused tech company (and heck, maybe that’s what we all should do; it certainly would have worked out well over the past five years!). At its most simple, the consumer surplus argument makes me think about the popular twitter meme “this website is free.” Basically the consumer surplus thesis is just looking for companies where that twitter meme is applicable and buying them; that seems to simplistic. You could also apply that thesis to just about any product (condoms cost less than $1, but people would pay way more than that for safe sex; do condom manufacturers fit into the “buy them because they create huge consumer surplus” argument?).

What’s the right answer here? I think its finding places where you can monetize that consumer surplus. That seems pretty obvious when you say it, but unfortunately it’s not always obvious in advance how a company will be able to do monetize consumer surplus. Consider video games: for years, it was obvious their consumer surplus was way in excess of their price (you paid ~$50 for a game, and the game could often give you hundreds of hours of game play; the cost per hour of entertainment was insane). It was obvious that the consumer surplus was huge there, but it was never super obvious how the video game companies could capture that surplus (much like Buffett mentions with Apple versus competitors, video game companies’ pricing is somewhat constrained by competition: there’s not that much of a difference between something like Call of Duty versus Battlefield where one of them could jack up their prices and capture that consumer surplus without losing hordes of consumers to the competitor). However, as technology has gotten better, micro transactions and subscriptions have allowed video game companies to begin to capture some of that consumer surplus; I’d guess that trend continues well into the future.

Some potential companies with obvious consumer surplus but questions around how they monetize it: basically every consumer internet company that monetizes through advertising excluding Facebook and Google (Snapchat and Twitter are the obvious two, but there are plenty of others), video games companies (still underpriced versus their entertainment value), Netflix (still massively underpriced versus how much consumers watch), Pandora and Spotify, broadband internet (broadband is ~$50/month, but without it almost everything we’ve talked about here (videogames, Netflix, your phone, etc.) is unusable (yes, you can use your wireless stream for a lot of it, but you’ll run into data caps and other issues really quickly if you try to fully cut broadband (wireless substitution))).

I’m certainly not breaking any new ground here, but just wanted to throw it out there because it’s the first time I think I’ve seen Buffett talk about consumer surplus for Apple and as I’ve started thinking about more consumer facing tech companies the consumer surplus and how to monetize it thought process has been very top of mind.

Asset managers “hiring moats”

I’ve written about the alternative asset managers (KKR, Blackstone, etc.) a few times on here. Honestly, I think you could probably buy any of them and do pretty well from here as the market seems to give all of them no credit for their incentive fee stream. Many of the asset managers (publicly) seem to agree, though the lack of aggressive historical share repurchases is disappointing (particularly given these guys are supposed to be financially sophisticated; if they say their shares are cheap but they don’t repurchase, are we supposed to believe their words or their actions?).

Perhaps my favorite exchange of all time remains this one between Blackstone and an analyst. Blackstone argues they deserve a dividend yield equal to the S&P 500, the analyst responds by asking why they don’t buyback more shares if they are so cheap, and the CFO responds by telling the analyst he is an idiot (more or less).

One thing I think is underrated about the asset managers: they have a “hiring moat”. For top finance talent today, the dream is to go from college to a big IB and work for two years there, and then jump to one of the major PE firms and work for two years there (or, increasingly, skip the IB and go straight to the PE firm). That path creates a huge edge for the major private equity firms: top young talent wants to work there and will favor offers from them over similar offers from smaller private equity firms simply for the resume equity.

I lifted the slide below from BX’s investor day which I think illustrates the point well (note: this slide could be easily manipulated: they are trying to show exclusivity, but it’s possible they gave out a job offer to every applicant and only 86 accepted their offer. Obviously not what happened, but I wish there was a better way to show desirability!)

I think there are plenty of other sources of competitive advantage that the large players have that aren’t super obvious. The WSJ had an article recently on a data advantage, which I think exists but isn’t huge. A more interesting one to me is a brand advantage. There used to be an old adage “no one ever got fired for hiring IBM” when it came to tech. This was meant to emphasize the career risk if you hired someone other than IBM: hire someone else who is great and you get a pat on the back; hire someone else who is bad and you’re fired. I think something similar exists for big asset allocators (pension funds, sovereign wealth, etc.) when it comes to alternative asset managers: no one ever gets fired for hiring KKR (or Blackstone, Apollo, etc.). Hire some unknown who hits it out of the park and you get a pat on the back; hire an unknown who goes bust and you’re fired. If you’re an employee at one of those asset allocators, best to simply go with a known brand that won’t get you fired no matter how they perform. That same brand name gives the large firms huge legs up when starting / launching new products (more tweets on this here and here).

I also think scale advantages (if you’re looking to sell huge assets, there are only a handful of firms that can play) are real as well (more tweets on this here).

While I’m on the subject of asset managers: I tweeted this out, but I’m perplexed by their obsession with converting to c-corps recently. I get that some of them have seen good share price performance on the heels of conversion, but isn’t this a perfect example of fishing for a short term stock pop at the expense of long term value creation given the conversion increases their tax burden?

One more question while I’m throwing hypotheticals out there: a bunch of externally managed companies pay their managers a fixed % of their equity as a fee stream. Just because we’ve been talking about Blackstone here, I’ll use a Blackstone vehicle as an example: Blackstone manages BXMT, and BXMT pays them 1.5% of equity per year as a fixed management fee (plus 20% of earnings over a 7% hurdle). As interest rates go up, the company’s asset base sees their earnings go up, which should naturally leverage the fixed management fee… so shouldn’t these vehicles see natural share price appreciation simply from that “fixed management fee” leverage? Obviously some of this will be offset by the incentive fee (which becomes easier to hit in a higher interest rate environment), but it’s still interesting to think about.

An example may show this best: say an externally managed company makes plain vanilla loans at 4.5% interest rates and deploys no leverage. Their fixed management fee would eat up 33% of their pre-fee earnings (1.5% / 4.5%). If interest rates go from 4.5% to 5.5%, all of the increase should fall straight through to their shareholders and suddenly the management fee is only taking up ~27% of their pre-fee earnings (1.5% / 5.5%). Obviously a simplified example (particularly because most externally managed companies employ some leverage and lend at higher rates, which decreases the fixed management fee as a % of earnings), but it’s still something interesting to think about. If you have any thoughts on it, I’d be curious.

Spectrum

I’ve said several times on this blog that I spend most of my time on cable / teleco / media and sports, and you can probably see a lot of that focus in the monthly updates.

Anyway, as part of that focus, I’m broadly aware of what’s going on with spectrum, and I have 3 (small) spectrum bets: Dish (disclosure: sadly long a little), Intelsat (I, disclosure: long but sadly not enough!), and one company I don’t want to mention yet.

I just wanted to mention Intelsat for a second because they have semi-ownership of spectrum in the C-Band (3.7-4.2 GHz) and there were two really positive pieces of incremental news on the C-Band I saw this month that didn’t seem to make too many rounds (update: I wrote this on ~September 24; as the Italian auction progressed higher on September 25th, the market did warm up to this).

International auctions of C-Band continue to show super strong demand. Italy is currently auctioning off C-Band spectrum and the prices telecos are bidding for it are blowing through what anyone expected it to raise. This continues a trend of European telecos paying up for access to C-Band spectrum.

I’ve long been a huge bull on cable companies getting into the wireless game. I know people have tons of questions on their vMVNO strategy, but eventually it seems to me they’ll either buy a wireless operator or simply amass some spectrum themselves and build out a network using their infrastructure as a major backbone. With that in mind, C-Band seems like a logical place for them to buy. Here’s what Charter’s (disclosure: long) CFO had to say about C-Band at Bank of America earlier this month, “I don't think we have to buy spectrum over time, but I think there are environments where it could be attractive for us to do so, and we're actively looking at that and we've expressed our interest to the FCC and others. The 3.5 gigahertz spectrum we find very attractive. The 3.7 gigahertz to 4.2 gigahertz, that's often been discussed as well, we think is also very attractive. We're running test on 3.5 gigahertz and we're running tests on 5G and higher band spectrum. And I think its public now that we filed an application to run test in the 3.7 gigahertz to4.2 gigahertz space as well.”

There’s tons of risks to investing in any of the spectrum plays (which has made me hesitant to casually bring them up on the blog as they’re pretty small positions), but I hadn’t seen anyone really comment on who the environment and demand for C-Band appears to continue to improve, and given Intelsat’s leverage that could result in huge upside for their equity.

I’d encourage you to read Kerrisdale’s pieces on Intelsat for more background.

PS- Kerrisdale’s Q2’18 13-F shows them with ~50% of their fund in Intelsat. Shares were trading <$17 then. Shares are up >40% since then (minimum); I would venture that Kerrisdale is having a very nice quarter.

Mea Culpa

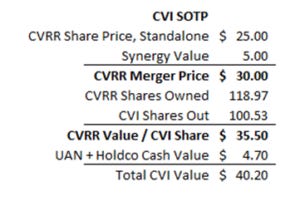

A reader was kind enough to point out that I used the wrong share count in my post on CVR (CVI, disclosure: long). I was using the number of shares from the 10-Q, not the share count post CVR exchange.

Unfortunately, that change takes away a substantial amount of the upside from the thesis. Previously this was an “even on conservative multiples, it looks pretty cheap… particularly in an acquisition” story. The new share count turns it into, “this looks roughly fairly valued, and you probably need a nice premium to do really well here.” The new story actually probably still works out well: Icahn is a great seller, and there’s not a lot up for sale in the sector. But still…. A disappointing change. Mistakes happen, but I’m embarrassed that I didn’t catch it earlier!

An updated SOTP is below:

The Braves (BATRA; disclosure: long) are going to the playoffs

In happier news, the Braves won the N.L. East crown and are playoff bound.

Does making or missing the playoffs dramatically change my investment thesis? Of course not. But it is a nice little cherry on top. Consider:

Strange things can happen in the playoffs. The Braves will likely be underdogs in any and all playoff series, but upsets happen all the time (particularly in baseball). Fivethirtyeight gives them a ~5% chance of winning the World Series, which feels about right.

Advertisers want to be associated with winners. Making the playoffs (and going deep into the playoffs) generally increase renewal rates for a team’s sponsors going forward and lures out sponsors from previously untapped categories (a few years ago, I was looking at Manchester United. After a deep playoff run, they signed up tire companies to be the official tire company of ManU. Maybe if the Braves make a deep run we see the official mattress company of the Atlanta Braves!).

Playoff runs and titles build a team’s story / legacy. That might seem too qualitative for a lot of investors… but it matters to potential buyers of a team and deep playoff runs help build up a team’s fan base (if you’re 10 when your team makes a deep playoff run, that team has likely just converted you into a fan for life). Playoff runs / legacy also factors into Forbes valuations of teams each year (either explicitly through an increased multiple or implicitly through increased revenue).

The Braves own a ton of the real estate around the Braves’ stadium. Playoff runs means playoff games… which translates into extra revenue not just for the Braves team (though that is nice too) but into extra hotel and restaurant revenue for all the buildings around the stadium.

Bottom line: the Braves missing or making the playoffs doesn’t make or break an investment thesis in the Braves, but it will boost their bottom line in the near term and adds to their appeal in the long term.

PS- An underrated part of Sirius (disclosure: long) buying Pandora? It could eventually lead to a whole slew of deals between pieces of the Liberty Empire and Sirius / Pandora; one piece of that could see the Braves getting spun off from their tracking stock into a real company. (PS- I think the Pandora / Sirius deal is a complete homerun).

We all underrated Netflix

A friend sent me Stratechery’s “Netflix and the Conservation of Attractive Profits” from July 2015. It’s really incredible to re-read the piece. The piece was written just three years ago and it’s talking about how highly differentiated content creators retain the largest advantage in the meia ecosystem. Roughly one year later, Time Warner (which owns HBO and Warner Brothers) saw the writing on the wall (that competing with the growing Netflix behemoth was going to require an investment they might not be able to make on their own) and sold to AT&T, and just two and a half years later, Disney (the company with, by far, the most differentiated content) would engage in a bidding war with Comcast (disclosure; long) in a deal “all about defeating Netflix”. Unbelievable how quickly the world has evolved to the point where Netflix’s combination of global scale / distribution and ease of use seems borderline unstoppable.

The bottom line of all these deals and the lessons from them: great distribution beats great content. Let me use an example to show this: Mercedes gets rave critical reviews, is based on a popular Stephen King novel, is written / produced by David Kelley (Big Little Lies, Boston Public, a ton of other popular series), and stars an Emmy winner. If great content was all that mattered, that show would be a huge hit. I’m guessing you’ve never heard of it (I have, but only because they plastered NYC with ads for it… and even then, I didn’t even know what network it’s on until I thought of them for this article (apparently it’s on an AT&T network; as an AT&T sub, I had no idea this even existed!)). Compare Mr. Mercedes to The OA on Netflix; it got generally ok to good reviews, didn’t have much star power, and wasn’t based on any pre-existing IP…. Yet I knows tons of people who watched the OA, and I’d guess a decent number of people could at least recognize the show and the network if you asked them. Quality of content certainly still matters…. But what matters more in today’s world is having a platform that consumers actually know about / have access to / subscribe to.

That said… Disney making TV shows for their streaming service based on secondary movie characters (Loki, Scarlet Witch, etc.) is a pretty powerful calling card for their new service (and just highlights how next level Disney’s IP is)! Still, outside of Disney’s Marvel and Star Wars universe, what other properties have characters that could immediately draw people to launch a service (a better way of putting this may be: what IP is widely popular enough that you could launch a theme park with)? WB is trying it with the DC Universe, but that’s noticeably separate from the movie universe (and I don’t think any but the most diehard fans would really care if they launched a DC Movie Universe TV spinoff given how badly that has been bungled!). The only other IP I could think of that would have that much drawing power is the Harry Potter Universe, but you’d probably need to get all of the original actors back in some form, which would be hugely costly and tricky (HBO could eventually do this with Game of Thrones, but it remains to be seen if there’s enough demand for the various spin-offs as there are for the current stories).

Follow up: after I tweeted that out, some people responded with Amazon / Lord of the Rings and CBS / Star Trek. Both are great examples, but I also think they both highlight just how next world Disney’s IP is. CBS has had success with All Access, but the service’s subscription numbers still pales in comparison to Netflix despite being the exclusive home of Star Trek (and I believe most of All Access’ subs are not actually “direct” subs but people who sign up from add-ons through Hulu or Amazon, which is a bit of a different game given Amazon takes up to 50% of the revenue if a sub signs up from them and maintains the relationship and data on the sub). Lord of the Rings on Amazon is going to be really interesting, but I think it has similar questions as the Game of Thrones spins (people love the core series / stories, but it’s unproven how much demand there is for these worlds outside of the core stuff. There’s the potential for “Solo” risk here where people love the Universe but it becomes increasingly difficult to tell new stories within that universe while keeping with the limitations set from the core stories). Series set in the Twilight or Hunger Games Universes could be interesting as well; those have huge fanbases and the world history is pretty deep.

Let me use another example to make my point: the best fantasy book I’ve ever read is The KingKiller Chronicles. Showtime has a deal to turn those novels into a TV Show, and Lin-Manuel Miranda will executive produce and compose music for the series (music is a huge piece of the books).That project is about as A-list as it gets, and I couldn’t be more pumped. But that’s a direct recreation of the novels; would I be super excited and sign up for the service if they weren’t doing the KingKiller story itself but something just set in the same world (a “shared universe” story)? I’d give it a chance, but it wouldn’t be “must have” for me, and what these services really need are must have properties that immediately drive troves of subs. I think of the LoTR spins Amazon in a similar bucket to the hypothetical “Kingkiller shared universe”; people will give it a chance but outside of the most hardcore fan no one will sign up on day one just for that story. Disney doing Marvel movie characters is clearly better than LoTR spins in this regard: fans outside of the super hardcore will consider it must have / sign up day one no matter what.

It’s interesting to consider all of the IP properties that don’t fit here. No one on my Twitter feed mentioned Avatar, the movie with the biggest box office of all time, and Avatar almost seems custom built for this type of world building: you could explore the history of the planet it’s set on, what’s happening at Earth while the movies are taking place, the history of the people/creatures who live on Pandora, etc, but I’m not sure people care enough about the universe to make a service “must subscribe” just on having a TV show set in it (I am sure Disney will test that assumption at some point once the Fox merger closes! It’s also worth noting Disney has already built an Avatar / Pandora section of a theme park). The Jurassic Park series has some of the biggest movies of all time, but it doesn’t seem like there are any stories to tell outside of the core movie world that could drive a streaming service (though they did build a park at Universal around it, so maybe it does qualify!). Same with Fast and Furious (do people care about the world outside the core characters? Almost certainly not Give me the Rock or don’t bother). James Bond and Indiana Jones are two huge franchises, but outside of the main characters does anyone really care about those worlds? Again, probably not.

Of course, these worlds can be built over time with proper investment: Harry Potter didn’t exist ~25 years ago, and the Marvel Cinematic Universe was generally considered to be using their “second tier” characters until Disney turned them into a juggernaut. Someday soon Netflix’s Stranger Things may qualify as this type of IP if they can successfully spin some new shows out of the main universe (one set in the present day? Ones exploring the other numbers?). I’m just pointing out there’s not a lot of this broad, super popular IP.

AMC’s plans to expand the Walking Dead Universe were also pointed out. Good luck to AMC, but I don’t think the series / brand comes anywhere close to the brand dynamics I’m talking about above. There’s lots of things to back that thought up, but I’d note that Walking Dead ratings (while still great) are well down recently and Fear the Walking Dead (Walking Dead’s spin off) hasn’t come close to the ratings of Walking Dead.

Speaking of AMC- I have no position in them but I think being long them is a VERY tough slog. Yes, they’re cheap and buying back shares, but as the Walking Dead continues to age and with all of the logical buyers tied up in deals, I think the next few rounds of cable negotiations are going to be very difficult for them. I think they’re another great example of the “great distribution beats great content” example; tons of their shows are extremely highly rated (Preacher, Into The Badlands, etc.) but have had trouble finding audiences and are getting ratings low enough to warrant cancellation.

So I think the Walking Dead Universe is a long shot. What TV series could have the “pull” to get people in? I can’t think of any that are anywhere close to the pull of Marvel or Game of Thrones, which just highlights how rare and valuable this type of elite IP is! The best one (outside of Stranger Things, mentioned above) I could think of was rebooting Lost, and spinning off a bunch of shows exploring that universe. I think that fits all of the things you need here: great IP with tons of corners to explore (more on the Island’s history, different timelines, more Dharma Initiative, etc.), it was on a big 4 network and had a huge audience (there’s plenty of great shows from smaller cable networks, but you need something that’s going to grab a lot of people for the type of pull I’m talking about), recent enough that people still remember it but far enough away that people have some nostalgia for it, etc. I think the Buffy reboot has some interesting universe potential to, and it certainly had a rabid fanbase, but again, probably not enough pull to singlehandedly launch a network or theme park.

The most interesting place for untapped potential here is probably video games, which often have huge fanbases and worlds rich with characters and back story. Netflix’s The Witcher and Showtime’s Halo will be interesting ones to watch there, but there’s tons of other amazing IP out there (Warcraft, Zelda, and Final Fantasy to name just a few of the franchises that seem custom built for this). I’d guess we’re still a little too early for a standalone video game to be the full “theme park” type draw (you need people who grew up with video games to age up a bit so that a video game park can appeal to a wide swath of ages), but it’s yet another reason why I continue to think legacy media and video game companies will see the line between them blur completely over time (and I think video game companies will have a huge leg up).

Note: I wrote all of this before this huge interview w/ DIS CEO Bob Iger came out. It’s interesting, and obviously him and I have different views of the world: he is still driving a narrative that content wins in the end, while I think content matters but in many ways distribution is more important in today’s world (as I tried to show w/ Mr. Mercedes).

An interesting and underrated piece “culture moat” working in Netflix’s favor- it simply seems easier to product TV shows there. Consider the “At Netflix, Speed is Key” article, which discusses how Netflix is able to get shows made much faster than a typical broadcast network timeline (the example used in the article, Dear White People, has a full season on Netflix in the time it would have taken a broadcast network to develop and produce a single test episode). Yes, Netflix takes a bit of elevated financial risk on each individual project, but as a whole I would guess Netflix’s approach is well worth it. It turns Netflix into a much friendlier place for people to work (this article mentions that Warner Brothers offered the creator of Blackish more money than Netflix did, but he went with Netflix because of their “artist first” mantra), and I wonder if Netflix actually takes on that much increased financial risk once you adjust for all of the failed pilots that the broadcast networks fund but never pick up.

PS- As mentioned above, I subscribe to Stratechery and really enjoy it; I’d recommend it if you’re interested in tech and media and don’t subscribe (of course, it’s not exactly a secret the site is awesome at this point). So I’m not pointing out the old article to “dunk” on the analysis; rather, just using the article to highlight how even smart and forward thinking analysts underestimated the strength of what Netflix was building.

Goofy proxy inclusions

This pitch for Wingstop (WING, disclosure: short, but in very small size) made me look at them a little further. The first thing I pulled out was their proxy, which includes all of their board members’ favorite wing flavors.

Honestly, I’m too amused by this idea. Why can’t I know the favorite item for every consumer facing board member?

Shouldn’t I know how many Hanesbrands’ board members prefer boxers to briefs?

If a bunch of Netflix directors start listing Adam Sandler movies as their favorite things on Netflix, can’t I use that as a red flag quality is headed way downhill?

If one of Coke’s directors is trying to pass Mello Yello off as their favorite soft drink, isn’t that a clue that they are either 1) braindead, 2) not actually trying any of Coke’s products or 3) both?

If Wingstop’s CEO favorite flavor changes from “Atomic” to “Hickory Smoked BBQ” one year, is that a sign the company’s risk profile is changing? Or if they add a new director whose favorite flavor is “Spicy Korean Q”, is that a sign the company is prepping for international expansion? The possibilities are endless. Forget proxy access; this is the hard hitting stuff I want the SEC focused on.

Sports media

NFL executives acknowledge TV Rights Near an “Inflection Point” With Tech Giants waiting in Wings

CBS undercuts Sinclair in battle with Hulu

Wasn’t sure if I should throw this link here or in the other things I like segment, but this is the type of stuff that makes me worry about broadcasters / affiliates.

Discovery chief says Facebook sports play more about marketing

Fox warns viewers blackout nears on Altice’s Optimum

I mentioned in my post on broadcasters I was worried about the “inflection point” Charlie Ergen (CEO of Dish; disclosure: sadly long a small amount) thought we had hit where the price of content was just too high and cable companies were more willing to black out content providers. Fox / Altice (FKA cablevision) have had blackouts before, so I don’t want to make this too hyperbolic, but if this dispute did come to a blackout during the middle of both the MLB postseason and football season, it would certainly lend some support to that “inflection point” theory.

Other things I like

NYC needs to create its own transit future—and ferries aren’t it

“Fun” look at the disaster that is NYC transit and why the city is opening so many ferries.

Spotify and music

Netflix and TV Streaming

With DC Universe, Warner Brothers looks to turn a valuable brand into a viable platform

“I will tell you that I was brought into a media company after I left Viacom to ask me some opinions about how to explain strategy to the Street. Their head of cable distribution said to me, “We’re going to push off one of the cable deals, because this Netflix is offering us $70 million, and they’re not going to be around in a couple of years.”…. So Netflix was also misunderstood in terms of they would see what they were spending on a show when they went in there, and they’d said, “Oh, my God. No network spends on that.” If Netflix is going to spend $8 billion on content, I believe that’s four billion less than Charter spends. They were spending to be the video experience. This is the greatest land grab in the history of media ever. It happened because those guys are brilliant and they ultimately figured out and made great shows, and they did like any other media business, which is they started out curating other people’s stuff. But really, they also succeeded because of the laziness and this silly laughter out of the people that were licensing stuff from them”

“It wouldn’t surprise me if Amazon bought CBS. You know, you get access to football. I’m not saying it’s not going to be done. I think a company like Netflix looks at that and says, “We see problems and we could scale faster and do okay on our own,” and ... Here’s what I will say. It’s like a Rube Goldberg. The minute one falls, the whole contraption starts to go. So if Lionsgate gets sold, let’s say to Google, there is no way that MGM doesn’t go into play because everyone is going to start running for catalog. You look at what Apple’s done. They hired these two Sony guys. They have the money to get the executives, they have the money to get the talent, and they don’t need the infrastructure of a studio. That’s fine for them. I’m not saying it’s not going to go. I think it will ultimately be whoever takes the first plunge and buys, that’s when media gets consolidated into tech.”

a16z Podcast: Why paid marketing sucks, Network effects, Viral Growth, and more

Bruce Flatt “Durable Principles for Real Asset Investing” (Talks at Google)

Why Google Fiber is High Speed Internet’s most successful failure