Some things and ideas: October 2018

Some random thoughts on articles that caught my attention in the last month. Note that I try to write notes on articles immediately after reading them, so there can be a little overlap in themes if an article grabs my attention early in the month and is similar to an article that I like later in the month.

Cable’s entry into wireless

I am a huge cable bull, and I think they are going to take serious share in wireless.

Sprint / T-Mobile filed a think piece on cable’s entry into wireless as part of their merger defense. Is Sprint / T-Mobile talking their own book? Absolutely (they need to make cable seem like a strong competitor to get their deal approved)…. But that doesn’t mean their conclusion (that cable is going to be a serious competitor) is wrong!

Whether you’re interested in the sector or just interested in learning a bit more on the MVNO business, the filing is worth reading.

Tucows’ filing is worthy reading as well.

Some additional thoughts on broadcasters

Thanks to everyone who emailed in response to my post on broadcasters last month.

There are a couple of questions that continue to weigh on my mind with the broadcasters group, and I’ve seen some articles / presentations that touch on those questions, so I thought I’d add a bit more here.

The first question is: long term, do networks really need broadcast affiliates? As we increasingly switch to a streaming / vMVPD world, why are the networks giving the broadcasters a cut? I really don’t know, but the recent news that CBS bypassed Sinclair and struck a deal directly with Hulu should be a big cause for alarm for broadcasters.

To be fair, Sinclair said Hulu wasn’t a big deal to them and the decision is reversible, so maybe I’m reading too much into the CBS / Hulu deal (Below from Sinclair’s CEO at DB Conference earlier this month)

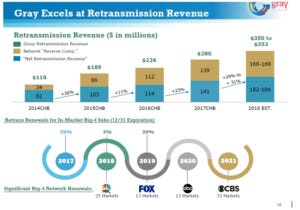

The second question: even if broadcasters are relevant / networks don’t drop them over time, won’t networks take an increasing share of retransmission over time?

If you’re a broadcast bull, your argument is that local news is critically important and has crossover effects for the network programming (i.e. if someone watches local news on their local CBS affiliate, they are more likely to watch CBS programming, CBS late night shows, etc.).

That bull argument does make some sense to me… but the chart below(from Gray’s September 2018 investor presentation) scares me. It shows the network’s share of retrans (“reverse comp”) rising from <30% of retransmission revenue in 2014 to almost 50% by 2017. My worry here is that both retrans and reverse retrans are relatively recent phenomena (the first time I saw retrans broken out in Nexstar’s 10-K was in their 2006 10-K when it accounted for 3% of their revenue (versus ~40% today), and the first time I see reverse comp mentioned in CBS’s 10-k is in 2012), and the quick increase from 30% to 50% of retrans in the slide below could suggest the networks just haven’t fully executed their ability to extract retrans so far. I think the vast majority of a broadcaster’s value comes from their network programming, so what’s to stop the network from receiving the bulk of retransmission fees?

Of course, every risk has a price, and perhaps that risk is priced in at these levels. Broadcasters are cheap. If you’re a broadcast bull, the quote below (from Sinclair’s CEO at the DB Lev Fin conference earlier this month) has to be music to your ears

CVI / CVRR update

I posted update CVI (disclosure: long) here. It’s a small spec position; I think it’s likely to be sold at a nice premium in the near future. Three things jumped out at me this month that make me think a sale is increasingly likely:

Another Icahn controlled subsidiary (American Rail) sold itself earlier this month. Icahn has now sold three of his major holdings (at Q2’18 end, they represented almost 50% of IEP’s NAV!) so far this year. I mentioned in the CVI piece that you can track his fund’s exposure through their commentary on their earnings calls and the fund was net long just 11% at Q2 end; combine selling off most of his controlled holdings with his crazy low net exposure and it’s clear Icahn is a seller in today’s environment. I’d guess he’s a very willing seller of CVR as well. CVR also is, by far, the largest position of IEP at this point, so if Icahn / IEP want to go further to cash selling CVI is really his only option at this point.

Management was pretty direct on the earnings call when talking about why the CVR exchange offer was done and what they think about they company’s valuation.

Management was also very direct that they’re willing to sell the company for the right price, but that price is high

Corepoint update

CorePoint (CPLG; disclosure: long) has pretty much roundtripped since I first wrote it up, driven by a weak earnings / guide in their first earnings report and a generally soft market for all things lodging recently. I think the company is very cheap currently.

A huge piece of the thesis rests on CorePoint deriving significant benefit from the La Quinta brand getting folded into the Wyndham system. Those synergies have taken longer than expected to come through, but they are coming and I think they could be large.

Wyndham’s Q3 earnings call gave a few hints on some of the improvements their system can drive

Proprietary channels (which carry significantly higher margins) continue to outpace OTAs like Expedia and Priceline.

1/3 of Wyndham’s hotel system is routing calls to Wyndham’s global call centers; hotels that do so see a 160 bps lift in ADR plus a 40-50% lift in Rewards enrollment.

Wyndham starts linking all of their brands with the “By Wyndham” banner and has seen a 9% increase in searches for brands that did not carry that endorsement previously.

A quote I liked that I think summed this up best “an independent hotel brand is likely to be worth more as part of a large brand family like Wyndham than on its own.” CorePoint’s historical earnings reflect their results with La Quinta as a standalone brand (as well as some other noise); over the next few years, we should see CorePoint / La Quinta improve performance as they realize the power of the Wyndham system.

While all of those stats apply to the Wyndham system overall, it doesn’t take a lot of imagination to see how La Quinta would benefit from them.

Ok, so maybe those stats don’t hit you over the head. Let’s look at what WH had to say about La Quinta specifically

“The brand had another strong quarter with RevPAR outpacing the industry and its Net Promoter Score is growing by 500 basis points to record highs”

Remember that CorePoint makes up ~a third of the La Quinta chain. If the brand is performing that strongly, CorePoint is set to be a major beneficiary.

Wyndham also provided a bullish update on their La Quinta integration and cost synergies; however, it’s less obvious of those specific initiatives will have any benefits for La Quinta franchisees like CorePoint (of course, some like integrating La Quinta into Wyndham rewards or improving the LA Quinta websites clearly will)

One general piece I wanted to highlight: Wyndham walked through how an independent would generally have an OTA contract 700-800 bps higher than Wyndham’s contract, and a mix shift of ~50% from OTAs versus the Wyndham system in the mid-20s. La Quinta was a decent sized chain, so the difference between Wyndham and La Quinta probably wasn’t as large as that example, but there will clearly be some synergies there that will eventually flow through to CorePoint.

Sports media update: A core tenant of the monthly update: continued highlights of the increasing value of sports rights (mainly because of my love of MSG (disclosure: Long)).

NBA fans can purchase 4th quarters

Interesting experiment with different types of monetization from the NBA. Particularly interesting that they mention a sports betting angle here. I would guess most of the fans / bettors who this appeals to already have league pass, but will be fun to see how this develops.

Interview with Atlanta Braves President (Disclosure: Long BATRA)

New Jersey plans to reveal “stunning” sports betting numbers

Other things I like

Diller says Hollywood Risks Getting Overtaken by Amazon, Netflix

Netflix exploring choose your own ending shows

I mentioned in this post that I thought it was inevitable that TV started doing choose your own adventure shows, and that eventually “TV” companies and video games would see the line between the two of them blur.

T-Mobile filing on HMNOs (cable wireless) (my thoughts here)

The Rise and Fall of the learning company (video game company that eventually bought/released Reader Rabbit, Oregon Trail, Carmen Sandiego, Myst, and many others)