Kontoor Brands: silly name, silly price? $KTB

Kontoor Brands (KTB; disclosure: long) is a recent spin-off from VF Corp (VFC). At today's prices, I think shares are too cheap, and I expect shares will "snap back" once the typical spin dynamics have played out and the company finds its investor base / announces its first dividend and gets onto dividend investor watch lists. There's a lot to talk about with Kontoor, but let me start with the most obvious. Kontoor is an awful name. I normally don't care about corporate names (even Tronc didn't really bother me), but something about the way Kontoor reads and feels in my mouth when I say it makes my skin crawl. If an activist ran against this board purely on the thesis "they approved naming the company Kontoor", I would vote for the activist. Ok, that very important bit of corporate name shaming out the way, let's turn to the investment thesis. It's actually pretty simple: Kontoor was spun out of VF Corp in late May, with VFC shareholders receiving one share of Kontoor for every 7 shares of VFC they held. VFC shares were trading at ~$85/share when the spin completed, so basically for every ~$600 of VFC an investor held they got 1 share of KTB worth ~$30/share. Spin-offs have been very popular among value and event investors for the past ~decade. The reason is obvious: everyone's read You can be a stock market genius (a book I highly recommend!) and "knows" that spin offs outperform. And the logic for spins outperforming makes sense! Large investors indiscriminately sell small spin shares they hold (often because of index restriction; i.e. a fund benchmarked to the S&P 500 might not want to hold a small spinco that will not be in an index), and spinning a smaller company off can incentivize the spinco management to be a bit more entrepreneurial / invest in the business in a more productive way. Still, I think at some point ~five years ago companies realized there was an investor base that would invest in just about any spin off, and you started seeing companies use spin offs to get their worst assets out of their footprint knowing that there would be a ready investor base to buy any spin (note that's just my opinion and why I've been hesistant on spins recently; there have been plenty that have worked but in general I think spins have been a very disappointing bucket over the past ~5 years). Anyway, I think Kontoor represents some combination of the above factors (both positive and negative). VFC clearly chose to spin KTB because KTB was the "worst" / slowest growth asset in their portfolio. Despite that, I think Kontoor's attractive: it should be a relatively stable business, and I think it shows a lot of traits of a typically successful spin: some more focus from management should let their brands stem their organic declines, and once the "sell the spin" dynamics are over I'd expect shares to rebound higher. Alright, hopefully that gives a broad overview of the spin dynamics around KTB. Let's talk about who KTB is and why I think they're so cheap. Kontoor has three main businesses: Wrangler, Lee, and Other (mainly VF Outlet store revenue). Other is small enough that it can be ignored, so the two big drivers here are Wrangler (which owns the Wrangler brand of jeans) and Lee (which owns the Lee line of jeans). The main appeal of KTB is that these brands are reasonably stable and KTB's shares are quite cheap. Let's start by talking about how cheap KTB is, since it's really the crux of the thesis. At today's share price of ~$27, KTB trades for just ~7.0x EBITDA. Given reasonably low capex requirements (most manufacturing is outsourced), KTB trades for just 8.5x unlevered free cash flow. There's reason to think there's some upside to those numbers: capex has historically come in <$30m/year and is currently elevated by some IT expenses; once those normalize in the next two or three years that would add another $30m in cash flow. In addition, the company has suggested they took $45m in charges prior to the spin that will result in $20-25m in annual cost savings going forward. If you factor in either of those (the cost savings or the lower normalized capex), KTB would look even cheaper.

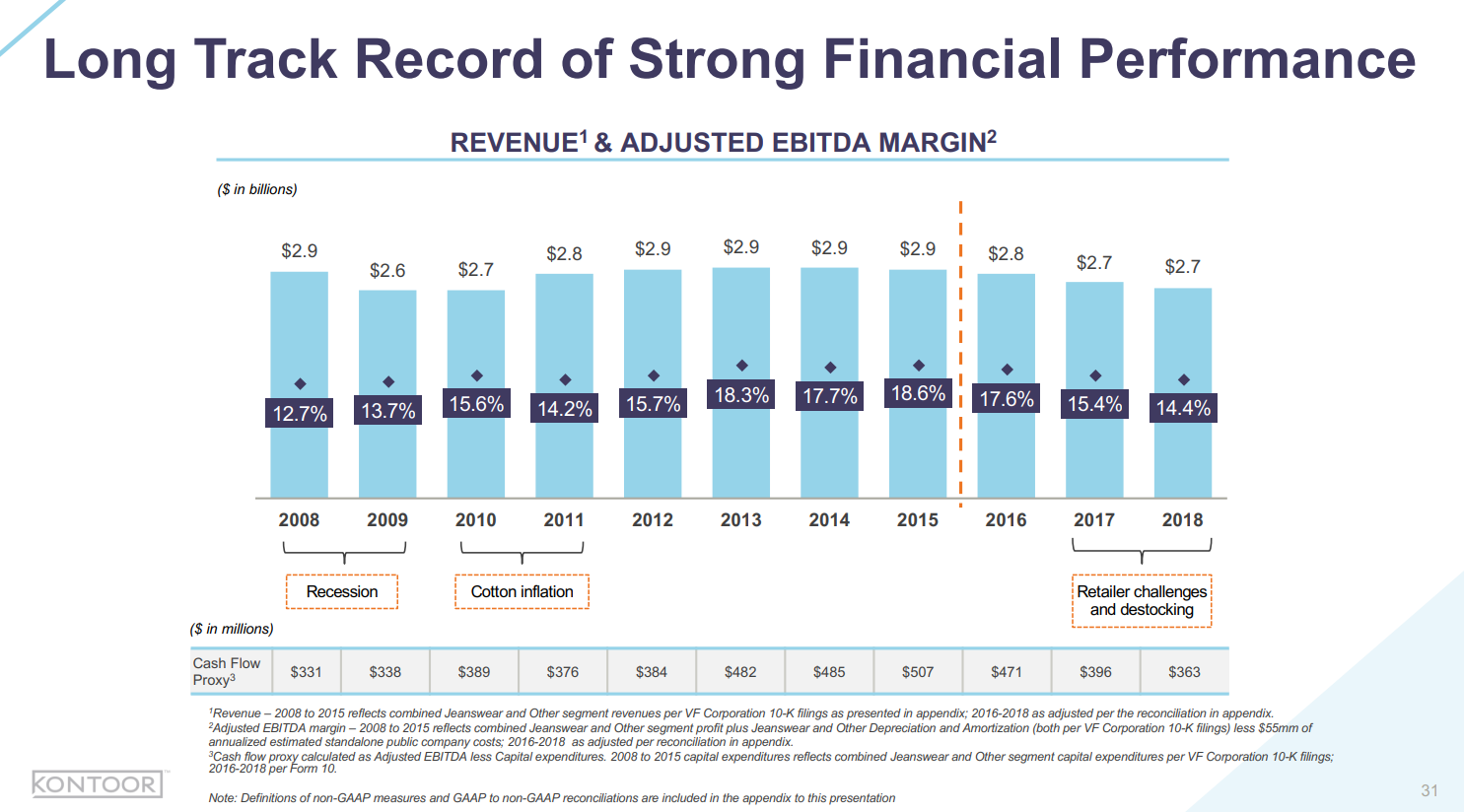

7x EBITDA and 8.5x unlevered free cash flow is quite cheap in the absolute, and it's awfully cheap if you look at KTB relative to some peers. The best peer is probably LEVI, which just IPO'd earlier this year and trades for ~12.5x EBITDA. Now, Levi probably deserves a premium versus KTB: it's growing while KTB is shrinking, and it probably has a better brand, but to sport a multiple >5x higher than KTB's is implying LEVI's brand is in a completely different universe than Wrangler. A 2-3x multiple discrepancy would probably make more sense and would result in a huge boost to KTB's share price (at 9x EBITDA, KTB is worth ~$40/share). The other thing I think is interesting about KTB is the consistency of their financials. The slide below is from the April 2019 spin deck and shows unlevered free cash flow has been above $330m every year for the past ten years. Given the low valuation, if this slide holds shareholders are going to do very well from today's prices.

I think the right hand slide of this slide also points to the possible bear case for KTB. Recent revenues and earnings have been declining, and 2019 will mark multiyear lows for revenues, EBITDA, and their "cash flow proxy" (all down somewhere between mid-single digits to low double digits, per their 2019 guidance). Q2'19 in particular will probably be a disaster; I counted three separate call outs for how bad it would be in their earnings release. This is where I think the spin dynamics could come into play in KTB's benefit: LEVI's has been reporting strong growth recently while KTB has been declining. Sure, Levi's is a better brand than KTB's, but that Levi's growing so strongly while KTB is declining suggests to me that KTB's issues are company specific, not structural issues (i.e. the decline of department stores will forever doom Wranglers. Department stores decline certainly creates near term headwinds, but Levi's continued growth makes me hopeful the brands can grow and survive in a more online world). With the renewed focus from the spin (i.e. the ability to invest in their own brands versus having VFC headquarter allocate the majority of resources to their core brands), KTB should be able to stem the bleeding and, eventually, return to growth. The biggest risk here is that I'm wrong on the ability of KTB to stem the decline. Maybe I'm right that the issue is KTB specific, but I'm wrong that it's fixable (i.e. the brands are just completely wrecked and Levi's is growing because their brand is gobbling up KTB's share and KTB will never be able to come back). I've seen no signs of that these brands are un-salvageable (for example, I did the cursory look at reviews on Amazon and Walmart and so no huge difference between Levi's and Wrangler / Lee) and I don't know of any reason why they would be, but that's probably the worst bear case. There are plenty of other risks here. Walmart is a ~a third of sales, so losing them would be a disaster. Direct to consumer and declining barriers to entry are an interesting risk (and somewhat tied to the "legacy retailers going bankrupt" headwind). It doesn't take much to launch a clothing brand these days, and a start up can micro-target their audience and offer clothing quality that is equivalent or better than legacy brands at equivalent pricing. How do major brands like Wrangler (or Levi's?) look as that trend continues to play out? I'm not sure, but I'd again note that this is a general industry risk so to the extent it hits Kontoor it would be hitting Levi's as well. In addition, there is some upside opportunity here as the world evolves: for example, I guarantee KTB's lowest margin revenue are sales through WMT. Over time, if more of KTB's sales shift online, that could be significantly margin accrettive for KTB. Of course, that assumes that the WMT business doesn't fall off, but I'm just trying to point out that the evolution of the consumer landscape isn't all negative! Other odds and ends

Dividend. In general, I'm not a fan of dividends. They're tax ineffiecient and I'd generally rather a company I invest in buyback shares instead of pay a dividend. However, I think Kontoor's dividend does provide an interesting catalyst. From an event standpoint, the dividend will probably help attract an investor base once it starts to get paid (the company is planning on paying out $2.24/share/year, which should attract some dividend investors / indices). From a value investor standpoint, while I would rather them repurchase shares at these price, it's somewhat reassuring to see that management seems very committed to the dividend (center piece of all their slides, mentioned multiple times in their investor presentation, spin docs, and earnings release) because it provides strong comfort that I know what capital allocation is going to look like. A huge question with many spins is what they want to do with their capital: repurchase shares, dividend cash out, or go on an acquisition spree? Most new companies generally lean towards the later with pretty poor results; KTB's commitment to the dividend minimizes capital allocation / deal risk.

Sale candidate: Longer term, I think KTB is a clear sale candidate. Why? VFC had a very low tax basis in these brands, and if VFC had sold KTB outright they would have faced a huge tax bill. By spinning KTB, VFC can dodge that tax at the corporate level. I'd guess once the two year mark passes and the tax liability from a sale is gone, KTB is auctioned to the higher bidder (I would guess private equity makes the most sense (private equity could lever them up to take advantage of the FCF as well as talking themselves into some continued growth avenues from direct to consumer, international, etc.), but you could talk me into some type of branded strategic after a drink or three).

Champion Brands Turnaround: There's a ton of differences here, so take this with a grain of salt, but this article on Champion turning itself around from your high school gym clothes to fashion clothes is really interesting to think about. Not because it's likely the Kontoor / Wrangler / Lee will become fashion icons, but because that type of optionality / brand expansion is the type of thing an acquirer would get excited about when looking at Kontoor and the deep history of their brands, and you're paying nothing for it at today's prices.

I guess another way to frame this investment is as a bet on the brands. We know the brand's history of earnings and what they're currently earning. Buying KTB is a bet that the future for the brands (in terms of how much cash flow they throw off) doesn't look dramatically different than the past, even if they are earning it a different way (perhaps more D2C than traditionally, or perhaps by continuing to grow the brand internationally). Historically, betting on brands has been a pretty good investment. The rise of the internet has changed that a bit as distribution got easier and advertising got more targeted, but I still think there's power to brands with this long of a legacy (both Wrangler and Lee have been around for >100 years).

Another interesting thought is how a clothing brand is different than a food brand. Nike, Lululemon, and a bunch of fashion brands have (seemingly) stronger moats than they've ever had, while most of the CPG companies (like Kraft Heinz) have seen their brands erode, and most of the retailers that tried to have some brand (Gap, J. Crew, etc.) are struggling as well. Why are the former thriving while the later struggle. I've got a bunch of different jumbled thoughts, but nothing differentiated enough to make an investment thesis on. An investment in KTB is much more an investment in cheap stock + interesting situation than it is a bet on the brand; I'm just throwing all these thoughts in here because I think they're interesting.

Investment in a company versus a situation: Ok, last thing and then I'll start writing (I feel like I'm entering into "word vomit" territory in this section). In the last paragraph I said "an investment in KTB is much more an investment in cheap stock + interesting situation." I don't think the KTB thesis is fully fleshed out but that's ok. The way I like to run my portfolio is with five core holdings that I understand extremely well and think will safely "compound" over time (things like KKR or the cable companies, often combined with some type of complexity that makes them screen poorly) with a bunch of smaller positions in things like KTB; situations that are obviously cheap and have some weird structure to them that (hopefully temporarily) keeps them from trading at fair value.