Reviewing my three worst mistakes of the year: $QRTEA $I $SYNL $ANGI $IAC

It may be the middle of December, but the year is prepping to wrap up for me. I'm going on my honeymoon this afternoon, and while I have skillfully negotiated with my wife that I will be allowed to work a little during the honeymoon, there are limits to how much a man can negotiate.... Anyway, with the year set to wrap up, I've been trying to take a step back and review the year. What worked in the year? What didn't? How can I improve my process? Things like that. I'll continue to think about them through the year end (after all, I have several international flights to ponder those questions during, and there's only so much Disney Plus a man can watch!), and I suspect I'll have some posts on any conclusion or takeaways in the new year. My early takeaways are it's been a generally good year, and I continue to improve as an investor. However, I'm not sure if I improved as much as I'd like to this year, and a particular focus of mine for next year is going to be continued process improvements. I feel like I'm drowning in things I want to research and can only get around to 25% of them; I want to be better at focusing on individual things and cutting projects off when they're no longer interesting. But that's a story for another day. Today I wanted to review the three worst investments I made this year. I run a relatively concentrated portfolio, with the top 5-7 names making up ~80% of the portfolio. Fortunately, none of my three worst investments came from the "core" names, but the effects of investing mistakes add up: a 50% loss on a 2% position is 1% of your portfolio gone. Equity markets do something like 6-8%/year on average, so a 1% loss might seem small but it's actually a significant amount of your expected annual return from investing. Hopefully next year I'll be reporting no "worst mistakes" for the year. But that's super unlikely: between special situations and other small positions, I make too many investments every year to not have one or two go awry. And, honestly, unless you're practicing an actual punchcard investing style where you only make ten investments over you're entire career, you're probably not taking enough risk if you never have one or two investments go against you. Also, I want to emphasize that I am only talking mistakes of commission (investments I made that I shouldn't have) here. I actually have some rather large mistake of omission (investments that I didn't make that I should have) this year; however, those are much more difficult to judge. If I passed on a company because I thought some risk was too great and it goes up 300% the next day, was that an error or was I probabilistically correct and just would have gotten lucky on that one? Tough to say.... and it certainly doesn't make for an easy to write blog post! So we'll be focusing on the lemons I bought today. Perhaps the diamonds I passed on will come in a future post. Anyway, on to the mistakes! Honorable mention: ANGI

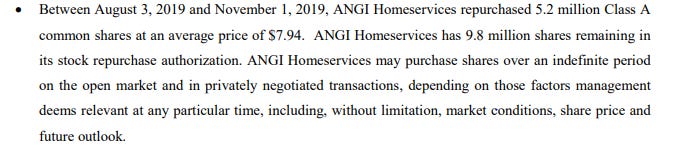

I'm not actually long ANGI directly. However, I do have a large position in IAC (I wrote them up ~2 years ago; my thoughts have evolved since then but mainly in a positive way. Unfortunately, the share price has risen a lot too, so it's not quite the bargain it was!), which effectively gives me a large position in ANGI. ANGI's stock was roughly cut in half this year; given the size of my ANGI position through IAC, that actually makes ANGI my worst performer this year. Why was ANGI down so much? A combination of a bunch of things: Revenue is a little weaker than expected; at the time of the deal, I think they were projecting ~25% annual growth (and I thought the projection made sense), and this year it'll come in under 20% growth. They haven't shown any margin inflection yet; in fact, despite the growth, earnings (using EBITDA as a proxy for growth) will decline YoY. I would sum it up pretty simply with this: the flywheel is taking longer than expected to start spinning. But that doesn't mean it won't spin! Getting local right is hard: ANGI needs to go effectively door to door to all types of local home businesses (plumbers, repairmen, etc.) and get them onto the ANGI platform. Doing that takes a lot of time and money, and I still think all the signs are there that ANGI is slowly cracking that code. If they're successful, the stock is going to be a rocket ship given today's valuation versus the potential upside. So I'm putting ANGI on the honorable mention list. It was my biggest loser of the year even though I didn't lose money directly on it, so I'm not 100% sure it qualifies here. But, more importantly, I think all the signs of a dominant marketplace are still there, and if ANGI succeeds in that this year's dip is going to be quickly forgotten. Let me quickly talk valuation for ANGI. At today's prices, you're paying a bit under 20x EBITDA for ANGI. That EBITDA number includes a decent bit of stock comp, so take it with a grain of salt, but still, for an online marketplace growing double digits that should be pretty capex light long term (and that's investing into a money losing European operation that diluted the headline earnings numbers a bit), that's not crazy expensive. The real trick for ANGI is what the long term margins look like. ANGI's LTM EBITDA margins are currently in the mid to high teens (~16-17%). At deal time, they mentioned a long term margin goal of 35%. I see no reason why they couldn't get their long term; this is an internet business with extremely high incremental margins, so margins should trend higher over time and I've reviewed a bunch of loss comps and most of them generally end up in this ball park (or higher) once they hit scale. If you look out a few years and assume ANGIcan continue growing double digits while expanding margins to 35%, you'd be buying a capital light dominant market place at a low to mid single digit EBITDA multiple at today's prices. Obviously the stock would be much higher if that came to pass, and equally obviously the assumptions of double digit annual revenue growth plus doubling ebitda margins are not exactly super conservative.... but the company thinks they can do it, and I've done a lot of work on it and I'm convinced they can too. I'm very bullish on ANGI. PS- you know who else is bullish ANGI? Their controlling shareholder, IAC. They mention how bullish they are in most of their interviews, and ANGI has bought back a decent bit of their free float at prices around their current price (below from ANGI's Q3'19 earnings)

Loser #3: Qurate QRTEA (disclosure: long)

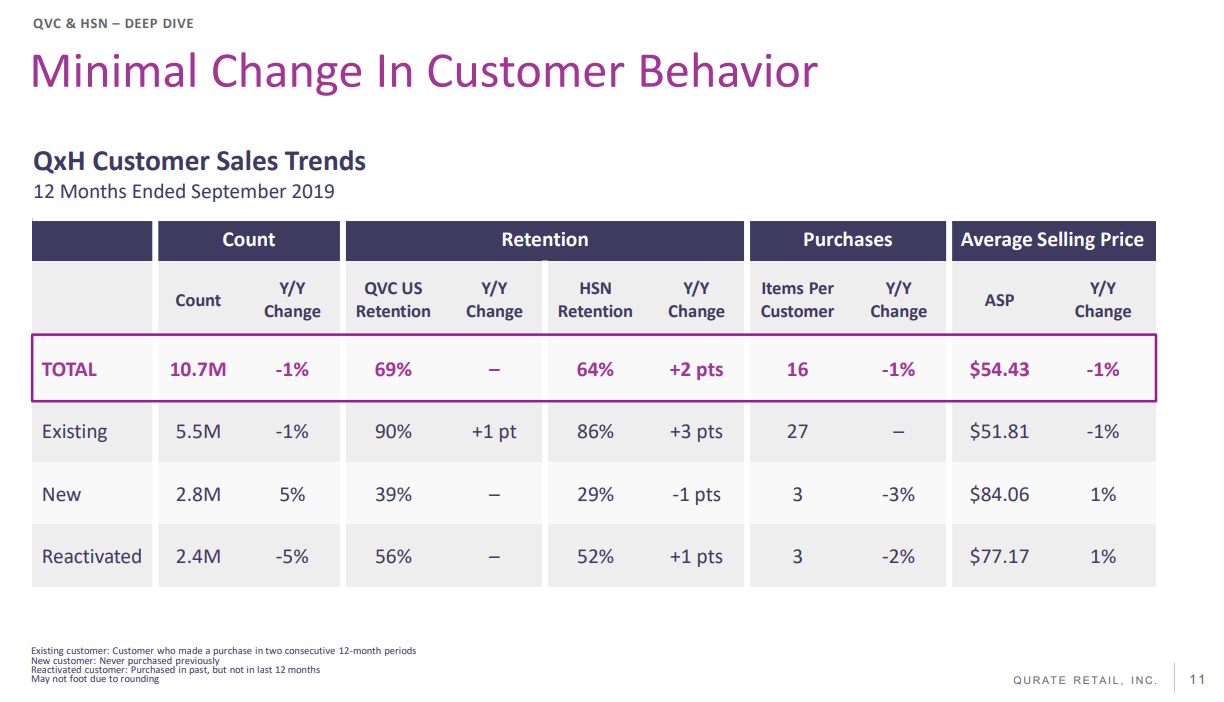

The story with QRTEA (formerly QVC) is really simple: the stock was really cheap (mid to high single digits on both an EBITDA and cash flow to equity basis), they were controlled by Liberty, they had just completed an accrettive deal to merge HSN and QVC, and they bought back shares aggressively. While some of the headline numbers (like revenue) looked weak, I thought you could paint a pretty solid picture that QRTEA had a defensible moat and that there were lots of underlying KPIs that suggested the business was ok. I would look at things like the slide below (from the Liberty 2019 investor day) and think "wow; the underlying user behavior doesn't look that bad! I'm buying this really cheap, they buy back shares, and earnings will inflect up as the get their HSN synergies. This is a great bet on a levered cash flow model."

Turns out it wasn't a great bet, and the company's financial metrics continue to deteriorate. I think the most telling thing about how bad QRTEA's current performance is can be seen in the change in share repurchases recently. In each of the past three years (FY16-18), QRTEA repurchased roughly 5% of their shares outstanding at >$20/share. Today, shares are trading for <$9/share, and QRTEA seems to have shut off the share repurchase machine in favor of managing their debt. Yikes. What's the lesson? Look, I love levered cash flow stories and share buybacks at low multiples. But you have to be very careful what business you apply the levered buyback stories to. It's one of the reasons I'm so worried about the broadcasters today; sure, they look cheap, and they spit off cash they can buyback shares with. But earnings at these companies can drop really quickly (margins are high and most costs are fixed, so a small decline in revenue can have outsized impacts on earnings / cash flow), and suddenly those share buybacks look like they were done at way too high of prices. Gamestop (GME) has been a really popular pitch among the deep value community recently; it spits off cash flow and it buys back tons of shares while trading at a very low multiple. It could be a good pitch... but I doubt that business is around in ~5 years. I'd be very cautious as a potential investor! #2 Intelsat (I; disclosure: long)

I've briefly touched on Intelsat in passing in the past on the blog. I had a small position in them based on the belief a private auction for their C-Band spectrum was the fastest and most rational outcome for the current process, and the private auction would result in a significant windfall for Intelsat. The basics of my thesis were pretty simple: the C-Band spectrum is the center piece of most other nation's 5G plans, and Intelsat and the other satellite companies controlled C-Band in the U.S. Rationally, the best thing for the country would be to do everything possible to get C-Band into wireless players hands as quickly as possible. I thought the FCC and the relevant political players would face huge pressure to free up the C-Band quickly for a few reasons

Most of the major telecom players are desperate to get their hands on C-Band, and the major telecom players have huge political sway.

The Trump admin plan to nationalize 5g included specific callouts to the C-Band spectrum (see p. 9). Nationalizing the nation's telecom infrastructure had few supporters, but I thought getting movement done on C-Band would play a small but crucial roll in keeping someone from getting a crazy thought into Trump's head.

The three key questions with the spectrum were

Would the FCC allow a private auction?

How much would the C-band owners be allowed to keep of the proceeds?

How much would C-band spectrum go for?

Again, I thought the incentives would push the FCC to a private auction run by Intelsat and the other satellite players. Doing so was the best way to get the spectrum into telecom players hands quickly. I was a bit more bearish than most on how much C-band would go for, but I still thought it would be worth tens of billions of dollars. I know that it might be a tough pill for politicians to swallow to see tens of billions go to satellite companies when the U.S. treasury could have some claim to those proceeds, but getting the spectrum to market even a few months faster would result in increased economic growth / taxes that would more than make up for that loss. So I figured rationality would prevail over easy soundbites / politics as usual. Unfortunately, I was wrong. Some politicians pushed that it was crazy that the money would go to the satellite companies instead of the U.S. treasury. It now looks like the FCC will run a public auction, and the satellite companies will get much less money than they would have under the private auction. The treasury is set to take in billions of dollars from this, which is nice.... but my guess is the spectrum ultimately hits the market at least two years later than it would have if the satellite companies had run a private auction, and I suspect that the lost revenue from that delay more than outweighs the money from the spectrum auction. What I learned: Don't bet on politics doing the rational thing... but if you are going to bet on it, make sure the bet is really small! #1 Synalloy (SYNL; disclosure: long)

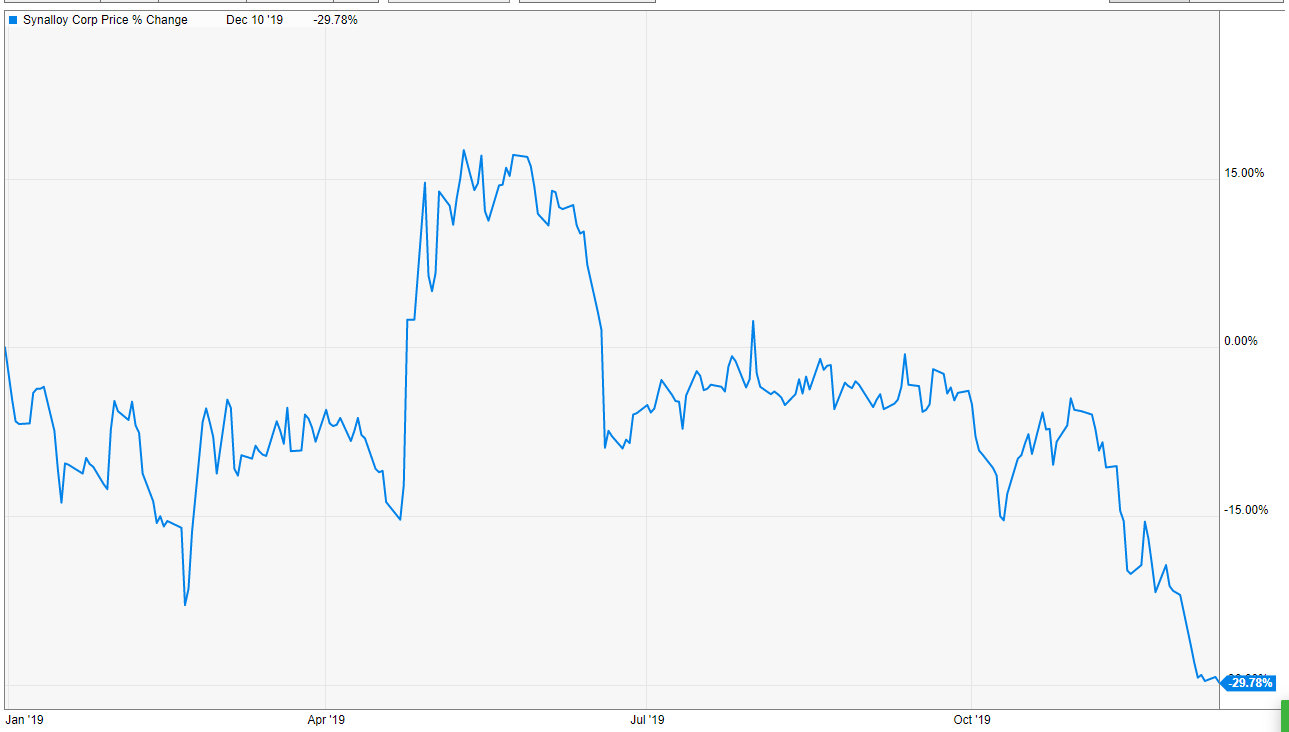

Synalloy was my biggest mistake of the year; while it wasn't down as much on a percentage basis as Intelsat or QRTEA, it was a bigger position for me, and I bought it close to the highs. The combo makes it my biggest loser of the year. I purchased SYNL (and wrote it up) in May after Privet made an offer to buy them out. The company arrogantly rejected that offer.... only to subsequently lower their guidance. When Privet came back with a slightly reduced offer after Synalloy reduced their guidance, Synalloy again arrogantly rejected that offer.... only to have to further reduce guidance as business conditions continued to weaken. I realize saying that the rejection offers were arrogant make me sound like a bitter bagholder (which I suppose I am), but seriously, go check the letters out and tell me they aren't arrogant! What I learned: I never loved the Synalloy business. I thought it was cheap, but it was cyclical and commoditized. I didn't like the management team either. What I loved was the situation. Privet had made offers to buy two of its portfolio companies previously, and each had resulted in bidding wars. I suspected Privet would at least bump their SYNL bid, or in a bull case you'd see an open auction and a little bidding war. Synalloy was a reminder to me that it's ok to take positions in companies where you love the situation more than the business.... but those positions must be much smaller. If you don't love the business, your margin of safety is much lower because if the situation fizzles out, you don't have the benefit of profitable growth at the business to support your thesis. An example might illustrate this best: say you bought Berkshire betting on a pending breakup. Even if that catalyst never came to pass, you'd do fine in Berkshire because you're buying it at a reasonable multiple and the underlying intrinsic value is likely to grow over time. Management is also likely to do rational things that continue to create value. With Synalloy, I bought at a reasonable multiple, but the business was volatile (so I took cycle risk) and management was poor (so I took the risk that management misallocated capital in some form). This is actually the second time I've learned this lesson. I took a decent sized loss on Lifetime Brands a few years ago when a major shareholder offered to buy them out. Lifetime went a different, management entrenching direction and did an awful deal that absolutely vaporized shareholder value. I didn't love Lifetime's business, and I really disliked the management team, but I really liked the situation. In the end, the business and management team "won" over the situation, and I took a loss similar to the one I'm looking at with Synalloy. A costly lesson to relearn, but hopefully one I won't make again. One last thing: bagholding As I wrote this, it struck me that I'm still long my all three of my biggest losers for the year (all the stocks just mentioned). That feels inefficient, as I'm not capturing tax losses. The company I'm particularly thinking of here is Intelsat; with QRTEA, at least I can point out it's still really cheap and they're likely to buyback stock in the future (even if they aren't currently) and with SYNL, Privet's still there so there's still a chance of some type of bid / process (plus the company is trading around at asset value now, which provides a lot more valuation protection). But the Intelsat private auction thesis is completely dead, yet I still hold the stock. Why? Well, partly it's because Intelsat is super levered, and if the C-Band auction goes well it's not hard to see the stock doing really well assuming they can get paid something for their role in speeding up the transition. It's also partly cause I don't believe in tax loss selling in December. If you're tempted to sell a loser in December.... there's a good chance just about everyone else in the stock is as well. I find a lot of these bounce back in the new year once the "forced" selling abates. (This is far from a unique insight; the January effect for losers is well documented) But I think I'm mostly not selling because I'm bagholding. I'm anchored to the price I bought Intelsat at, and I'm simply hoping it gets back there at some point. And because I'm bagholding on Intelsat, I can't help but wonder if I'm doing the same with SYNL and QRTEA and any of the other losers in my portfolio (fortunately there aren't a ton more currently than the ones I mentioned, but they certainly exist!). It's something I'm going to think about more. I wouldn't be surprised if I don't own Intelsat (or SYNL or QRTEA) in the near future. But I'll be thinking about it from somewhere in Asia. Hopefully with a drink or three in me (do they have White Claws in Asia yet?). Have a fantastic holidays, and I can't wait to talk to you in the new year.