Premium Post: Backing some litigation

The most dangerous words in investing are “this time is different”. For years, one company has been something of the widow-maker trade for smaller event driven investors…. But I think this time is different.

The most dangerous words in investing are “this time is different”. For years, one company has been something of the widow-maker trade for smaller event driven investors…. But I think this time is different.

Why do I think this time is different? Well, the price is much lower, and the catalyst is much closer. By this time next year, I expect the company will have collected >$2B in lawsuit proceeds from their major lawsuit, and as a result shares should trade significantly higher.

The company? Ambac (AMBC). I’m going to start with a summary of the thesis, then some background / overview of the company and sector, and then move into the different parts.

Thesis summary

Today, Ambac trades for ~$14.50/share. Ambac has $10.06/share of unencumbered cash and investments at their holding company (“AFG”; the bulk of which is just straight cash). That cash represents significant downside protection; even if everything else with Ambac turns out to be a zero, that cash could be dividended to shareholders tomorrow. So, at current prices, about two-thirds of your investment goes into a cash shell and the other third goes into buying an option that legacy Ambac’s operations will have significant value.

That’s a very good bet. Legacy Ambac (“AAC”) currently has a book value of almost $10/share, so looking through the $10/share at the holding company, you’re buying legacy Ambac for ~50% of book value (($14.50/share less $10/share holdco cash)/($10/share legacy Ambac book). However, the real kicker is that legacy Ambac has significant claims against banks (in particular, Bank of America / Countrywide) that are dramatically understated on their books. Based on historical precedents and how long the claims have been outstanding, I think AMBC could see at least $1B in gains when they finally settle these cases. That would result in per share book value gains of ~$20/share, and it would all be in cash. Ambac could then use that cash to accelerate the wind down of the rest of their liabilities (likely by paying AGO to assume responsibility of the liabilities, something that several of the other legacy guarantors have done to great success in the past), dividend the remaining equity up to the holding company, and then return cash to shareholders or (unfortunately, more likely) look to take advantage of their tax assets by using the cash to buy a new business. Either way, a year or three from now Ambac should have line of sight to >$30/share in cash at the holding company plus significant tax assets (over $1B in NOLs at the holding company plus ~$2.5B at AAC). Today, you’re buying that for $14.50/share. Even if the eventual acquisition Ambac makes isn’t great, you’re buying at such a huge discount that as long as the acquisition isn’t a complete disaster shareholders should do very well (again, the holdco has over $1B of tax assets, so the acquisition would have to be an absolutely epic disaster to really destroy value).

Why does the opportunity exist? Well, Corona has caused Ambac’s court cases to get pushed back significantly, and the disaster that is municipal finances (in particular, Puerto Rico finances!) has caused Ambac’s legacy liabilities to look significantly worse than they did a year ago. That combo, plus small event investors fleeing the scene, has left Ambac’s stock for dead. But with the long overdue court case finally scheduled to happen early next year and a stock price that barely trades above Ambac’s cash value, I think now’s the perfect time for AMBC.

Background / Overview

Before the financial crisis, financial guarantors were all the rage. They initially started out as focused almost exclusively on insuring municipal bonds, but over time they came to insure everything under the sun. Of course, that ended with almost every financial insurer blowing up in relatively spectacular fashion during the financial crisis. Today, the financial insurers are effectively zombies or husks of their former selves. Syncora (SYCRF) liquidated in 2019, and, while MBI and Ambac continue to trade, they trade for a fraction of their book value and are each in a various state of run-off / liquidation (neither writes guarantees anymore; at some point they will eventually take their cash and buy a new business to pivot, or they will simply liquidate as their liabilities run off). Only Assured Guaranty (AGO) continues to operate as a functioning business, and they trade for a fraction of a fraction of book value (I wrote up the bear case and bull case for AGO earlier this year; feel free to read it for more background on financial guarantors).

Today, Ambac exists to do three things: mitigate the losses from their legacy guarantees (on a risk adjusted basis, Puerto Rico is the largest exposure), maximize their legal recoveries on realized losses (mainly by suing the banks who underwrote all the loans that went bust on them in the financial crisis; this is where their BoA litigation upside comes from), and eventually buying a new business that will “generate long-term shareholder value creation.”

That’s actually a really strange combination. Ambac’s value proposition to shareholders is basically, “hey, we’ve got a big pile of assets right now, and we know we owe some people money. We’re going to minimize how much we have to pay those people, sue other people to increase our pile, and then go buy a new business that you’ll love. Trust us!” It’s strange for a bunch of reasons, but in particular it’s strange because each of those three pillars (buying a new business, restructuring legacy liabilities, suing banks for money they owe you) involves a completely different skill set and a completely different risk/reward profile. That makes Ambac a wildly difficult stock to own.

Traditionally, Ambac has been owned by smaller event investors for a simple reason: the upside from Ambac’s litigation was so large and so likely that the near term return from a successful settlement dwarfed the tail risks of Ambac making a poor acquisition or seeing their legacy liabilities balloon. Then COVID happened, and Ambac’s stock got hit with a triple whammy: the likelihood of harsh payments on their legacy liabilities shot up (their legacy liabilities are mainly tied to municipal finances, particularly Puerto Rico’s, and COVID has devastated municipal finances), COVID shut down the New York court system (pushing back the timeline for Ambac winning/settling their case against the banks), and the volatility in March caused a ton of smaller event investors to flee Ambac’s stock and never come back. As a result, the stock has languished so far this year (though the November blue wave boom has helped it come back slightly!)

At this point, hopefully I’ve driven home three things:

The cash (and tax assets) at the Ambac holdco provide significant downside protection, as they make up the majority of today’s share price.

The complexity of Ambac’s financials and the death of small event funds post-Covid has created opportunity at Ambac.

Legacy Ambac (AAC) has $10/share of book value; however, that book value should increase significantly if and when the company wins their case against BoA, and I expect that win to drive shares higher.

I’m going to spend the rest of this article diving further into point #3 and why I think Ambac is so likely to see a gain here.

Ambac’s claim against BoA dates back to the financial crisis; financial guarantors guaranteed a ton mortgage backed securities that eventually went bust. The guarantors had to make huge payments in response, and they turned around and sued the banks who underwrote those mortgages for a variety of things (breach of contract, fraudulent inducement, breach of reps and warranties, etc.). The basics of the suits were “these mortgages were awful, and if you had disclosed how awful, we would have never insured them, so you should pay us for them.”

Normally, I would be hesitant to bet on a thesis where all of the potential upside rested on a successful legal outcome. However, at this point, we have a long history of guarantors suing banks for pre-crisis mortgages, and the financial guarantors are batting 1000 in their suits. If we just look at BoA’s history, they settled with AGO in 2011, Syncora in 2012, MBI in 2013, and FGIC in 2014 (they’ve also settled similar suits with Freddie / Fannie in 2011 and AIG in 2014, among others). However, it’s not just BoA that has settled a bunch of suits; across a variety of insurers and banks, we can see a history of big payouts from the banks to the insurers. For example, JPM / AGO in 2013, UBS / AGO in 2013, JPM / Syncora in 2014, Credit Suisse / AGO in 2014, JPM / Ambac in 2016, and Syncora / Greenpoint in 2018. In fact, I cannot find a single example of one of these lawsuits that did not settle. The bottom line here is that banks do not want these suits to go to trial; they have settled every single suit I can find for huge payouts in favor of the guarantor.

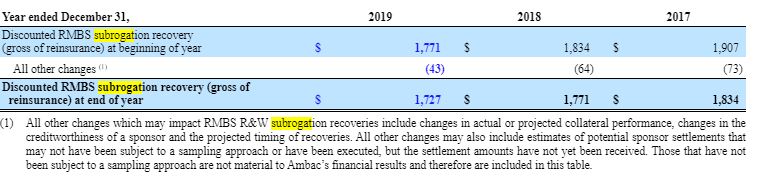

That’s nice; however, a huge payout here does not guarantee that Ambac posts a huge gain. Ambac already has an asset on their book to account for the amount they expect to recover from their claims (their “discounted RMBS subrogation recovery” asset). I pulled the table below from AMBC’s 10-k (p. 94). You can see that they have an asset of ~$1.7B from expected recoveries. So the key question is not “will they eventually get paid hundreds of millions from their suit with BoA?” as, given the history of these cases, the answer there is almost certainly yes. The key question is “will their settlement with BoA significantly exceed the asset they already have on their books?”

The good news is that the answer is, again, almost certainly yes. The history of these settlements is that they produce mammoth gains for the financial guarantors. For example, AGO settled their BoA suit for $1.1B in 2011; if you look at p. 36 of their next 10-Q, you can see that settlement resulted in a ~$334m gain. MBI’s BoA settlement in 2013 appears to have resulted in a ~$200m gain (look at the loss adjustment line in their income statement). More recently, Syncora’s settlement with Greenpoint produced a $285m gain. If we look at Ambac, their $1B settlement with JPM in 2016 produced ~$272m in gains (quote below from their Q4’15 earnings call).

There’s a reason these settlements result in such large gains, and it’s a function of GAAP (accounting). Take another look at the RMBS table I pulled from AMBC’s 10-k. Notice that the subrogation asset balance only goes down, never up. In the real world, these claims increase in value over time because they accrue statutory interest as time goes on and the lawsuit remains outstanding. So, by the time an insurer and bank reach a settlement, the potential damages are often hundreds of millions of dollars more than the initial claims because of statutory interest, and the settlement generally reflects that.

An example might show this best: say an insurer sues a bank for $1B today, and statutory interest is 5%. If they settle for the full claim next year, the bank would pay $1.05B. However, the insurer would not have accrued statutory interest on their claim over that year, so they’d book a $50m gain when they reached settlement. Note that the actual gain would likely be larger; insurers need to discount their claims for a variety of reasons (like the chances their suit is unsuccessful).

Given the limitations of GAAP and the history of settlements, I expect that the eventual BoA / Ambac settlement will produce a mammoth gain. Ambac’s suits were filed in New York, where the statutory interest rate is 9%, and their suits date back to 2010 and 2014. At this point, the statutory interest on those claims is worth hundreds of millions of dollars, and all of it is an asset sitting off of Ambac’s books.

Bottom line: if and when Ambac and BoA eventually settle their suit, I expect that Ambac will report a massive gain on the settlement. The range of gains is pretty wide, but my expectation is that Ambac will settle for a $3B payment and a gain of over $1B.

The other key piece to the Ambac investment thesis is that the trial is fast approaching; the Ambac / BoA case was originally scheduled to start on July 13, 2020; however, COVID caused them to delay the trial until February 2021. It is possible the trial is delayed again, either because COVID continues to cause the court system headaches or because BoA continues to delay the trial (to date, BoA has run a strategy of dragging this trial out as long as possible, possibly because they believe doing so will force Ambac’s hand to reach a disadvantageous settlement). AMBC expressed cautious optimism that the case would start as currently scheduled in their most recent earnings call:

So, at this point, it appears we are reaching the end game, and the trial is on course to start in February. That’s big news for Ambac: most of the guarantor suits have been settled in the days immediately preceding the trial’s start, so if the trial start date holds for February, we could be looking at a settlement in the next three months. If and when that happens, I expect AMBC to realize hundreds of millions in gains, and the stock to rerate appropriately.

The other piece to AMBC that is worth considering is their legacy liabilities. These are the guarantees that they wrote before they effectively went into run off. The headliner here is AMBC’s Puerto Rico exposure, as of Q3’20, AMBC was still on the hook for ~$2.5B in net principle + interest of Puerto Rico guarantees. However, there’s plenty of others; as of Q3’20, Ambac insured $14B of adversely classified credits.

I think the most important thing about these liabilities is that they are coming down rapidly. Current conditions, with 0% interest rates and the world awash in liquidity, are enabling even the most marginal of municipal credits to refi debt at lower rates; as those munis refi debt, AMBC’s legacy liabilities continue to come down. You can see the results of this over the past few years in the slide below. Management commentary indicates that they expect continued momentum here, which is great for the thesis as it allows AMBC to realize more of the upside from the eventual BoA settlement.

You can do a lot of work on AMBC’s individual credits if you want to, but my bottom line always comes back to this: I think the upside from the BoA case more than outweighs even the tail downsides of their legacy exposures. Your biggest risk is obviously AMBC’s Puerto Rico exposure, and none of the insurers are completely clear on how they mark their exposure to Puerto Rico, but Ambac’s exposure is manageable and I believe their marks are more conservative than their peers.

I’m happy to talk more about AMBC’s legacy exposure offline if anyone is interested, but I don’t think that’s where the edge here is. Again, I think AMBC has the most conservative accounting of their peers, and I think they are much further along to cleaning up their legacy liabilities. The edge for AMBC is all the work on the history of settlements and how large the gain on settlement is likely to be. If I’m right there, the gain from the lawsuit settlement will swamp any reasonable downside from the legacy liabilities.

So how do I think this plays out? I expect that trial date will remain in February. Again, it might get moved, but I’m hopefully that it will stay that date. As the trial approaches, I expect AMBC and BoA will settle, and the settlement will cause a huge gain for AMBC. At that point, buying AMBC will be a bet on a successful future acquisition and resolving legacy liabilities; and I’ll have to reassess the investment thesis…. but we’ll be assessing with AMBC’s stock price significantly higher than today’s.

Odds and ends

Peers trade at a fraction of book argument: A frequent pushback to the AMBC pitch is, “well, AGO and MBI trade for a fraction of adjusted book value. Why should AMBC see a lot of upside even if they settle and get a huge gain?” I think that’s good push back, but I think it’s misguided. AMBC’s holdco has much more value than MBI or AGO’s (both of those rely much more on their subsidiaries for their value), and post settlement AMBC’s book will be lightyears closer to “clean” than either peer (clean being a point where they can see line of sight to wrapping up their book, likely through having AGO reinsure it). Basically, AMBC’s book value will be much cleaner / more cash / less assumption reliant than their peers, which should command a significantly higher multiple.

Gain on settlement- I ended this article with the line “we’ll be assessing with AMBC’s stock price significantly higher than today’s.” An open question is how much higher the stock will be. In the past, insurer stocks have popped anywhere from 20-50% on big settlement announcements. The most recent settlement announcement was Syncora in early 2018, which drove their stock from ~$2.40/share to ~$3.40/share. I’m a little hesitant to draw conclusions from “past pops”, as many of these were when the outcomes of the litigation were still in doubt or (in Syncora’s case) for extremely small cap stocks with not much attention. Ambac today doesn’t hit any of those boxes. Still, I suspect history will rhyme here; at this point, investors have been discussing a BoA settlement as an AMBC catalyst for over five years, and AMBC’s shares have performed in line with AGO / MBI YTD. Given how much of AMBC’s value is baked into the BoA upside (while peers get none of their value from it), I think it’s safe to say the market is putting a huge discount on AMBC’s litigation value and any settlement will be met with a large pop. It certainly depends on how good the settlement is and how large the gains are, but if the AMBC settlement is within my estimates ($3B headline number; >$1B in gains), I think AMBC will easily be a >$20 stock.

Accounting complexity creates opportunity- I’m not sure I drove this home in the write up, but Ambac’s accounting is complex. A quick glance at Ambac’s financials does not show ~$10/share in unencumbered cash at the holding company; in fact, a quick glance at Ambac’s financials would make you think they are insanely levered and a slight change in assumptions would zero out the whole company. I think that complexity is a big reason this opportunity exists; without a lot of digging, it’s not easy to see how much downside protection Ambac has. Most investors, at a glance, would think Ambac is simply a bet on a successful BoA settlement, and without that Ambac would be a zero. That’s simply not true: Ambac is a significantly downside protected bet on a BoA settlement.

Other settlement opportunities: BoA/Countrywide is the headliner here, but Ambac also has outstanding cases against First Franklin and Nomura. I expect these will produce gains for similar reasons to the BoA case, but the cases are much smaller so they’re not a huge driver.

Warrants- AMBC does have a set of warrants outstanding. These have a strike of $16.67 and expire in 2023. I actually prefer the equity to the warrants given the equity benefits from the downside protection of the holdco cash; however, if you’re looking to bet on a really big settlement with BoA, the warrants are obviously an interesting way to do so!

Other write ups on AMBC worth reading