Quickie idea / Christmas Gift: Collectors Universe Bumpitrage $CLCT

This post is a special post. It doubles as both my Christmas present to you, and a continuation of my "“quickie” idea" series.

Now, I know what you're thinking. "How thoughtful of Andrew to get me a Christmas present!!!! But man, this is awkward. I didn't get him anything!"

And the good news is I'm here to help you with that problem too! If you've enjoyed this blog and want to get me a Christmas gift, please consider making a donation to Watsi. It's a cause my partner Chris is very passionate about (he's helped 380 patients in 18 countries!), and any donations will be put to great use. I love efficiency, and I find that a few dollars to Watsi (or really any emerging markets focused charity) generally stretches much, much further than many domestic focused charities (that said, if you want a more domestic focused charity, Modest Proposal turned me on to innocence project and institute for justice, and I've become a supporter of both).

So, if you haven't gotten me a gift and are able to, consider donating to Watsi (you can read a little more on Watsi's background and what makes them so efficient here). Thanks! And guilt trip over!

Anyway, this is both a Christmas present and a quickie idea. So what is a quickie idea? It's an investment specific idea that I’ve been mulling over and find interesting, but haven’t dove fully into yet. The hope is to provide the jumping off point for a discussion of an idea I find extremely interesting right now, as I suspect the opportunity could be fleeting.

Today's quickie idea? Buy Collectors Universe (CLCT) in anticipation of either 1) the current buyer group needing to give a "kiss" (a bump to their bid) to get their deal done or 2) a competitive bidder emerging at the last second. As I write this, CLCT is trading for ~$75.25/share. The current bid is priced at $75.25 (~$680m market cap) and set to expire January 19th. So the trade is simple: buy the stock and hope for a kiss / bidding war. If nothing comes, tender your stock in ~a month and break even. Heads, I don't lose; tails, I win.

Why do I think a bump or bidding war is possible here? Collectors Universe provides authentication and grading services for memorabilia (coins, trading cards, etc.). To put it kindly, the business has historically been undermanaged. Over the summer, Alta Fox went public with an activist campaign to, in effect, revitalize the company. This lead to a settlement in September, and eventually a deal to be acquired by an investor group in late November at a 30% premium to the stock's 60 day VWAP.

Pretty standard stuff, right? Activist comes in, demands a shake up, and the board announces a quick sale at a nice premium. Not so fast! The deal was announced November 30 for $75.25/share. CLCT had announced blowout earnings on November 3rd; their stock had traded reasonably range bound between $65-$70/share from earnings announcement until deal close. CLCT closed November 27 at $72.55/share. So, depending on how you look at it, the deal was priced at a 5-10% premium to CLCT's stock price. For the board to highlight a 30% premium to the stock's 60 VWAP is very, very curious. Why does offering a premium to where the stock was trading in October, before the strong earnings report, really matter to me as a shareholder?

There were a lot of different angles and motivations that could be behind that semi-misleading premium highlight, so I was eagerly looking forward to the company filing their tender docs with the background to the merger process. Those docs came out Friday (December 18), and I was not disappointed in the least.

The highlight here happens on page 18. Alta Fox files their 13-D on June 18. On July 1, CLCT hires Houlihan as their investment banker. Six days later, Nat Turner drops out of the Alta Fox board nominee slate; roughly two weeks later Nat would contact the board and Houlihan about acquiring CLCT. As far as I can tell from the background, Houlihan never reached out to a single other acquirer of the company; in fact, Houlihan appears to have repeatedly rebuffed a potential acquirer of the company ("Party E") due to financing concerns.

This repeated rebuffing of Party E is a little strange; Houlihan allows Turner to talk to at least three different groups about joining him / providing equity financing (Party D, D1, and Cohen / CPV). If Houlihan was really concerned about Party E's ability to finance, why not at least let them try to get some credible investors to join their group?

There are tons of other interesting things in the background; for example, on November 6, the stock closes at $71.60 and Turner indicates a $75-$80/share pricing range. Over the next month, there's lots of back and forth over pricing, go-shop provisions, and break fees. Somehow, CLCT gives on basically every one of those provisions, yet they still end up agreeing to a deal at the low end of that indicative range priced at almost no premium to the current stock price. Dilbert would be proud.

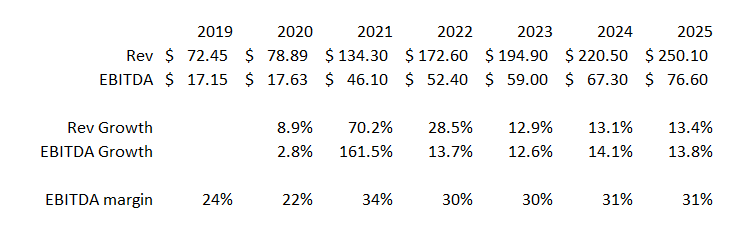

Or consider CLCT's projections on page 38 of the tender; I've pasted them below. Notice anything curious in there?

Take a look at the Adjusted EBITDA growth versus revenue. I've laid it out in the table below; I've also taken the liberty of adding FY19 & FY20 to the table to make it a little more explicit (note that the company didn't provide Adjusted EBITDA for those years, so I calculated it as EBIT + impairment + D&A).

Well, that's interesting, isn't it? The company is forecasting huge growth in FY21, and that huge growth leads to significant operating leverage as EBITDA margins go from ~22% to ~34%. The future forecasts includes continued huge revenue growth; almost 30% in 2022 followed by continued low teen growth in the out years.... but, somehow, the huge growth starts leading to negative operating leverage, as EBITDA margins drop from ~34% to ~30% in those years.

Curious.

While I'm here, one more bonus point: I have traditionally estimated the cost of being a public company at ~$1m/year. In last month's quickie idea, I noted Alaska (ALSK) was putting the cost at $4-5m/year. CLCT is projecting <$50m in EBITDA in 2021, so the potential savings from going private are pretty significant to CLCT regardless of if the actual costs are closer to my numbers or Alaska's.

Anyway, what I'm driving at is this: when I read this proxy, I don't read the background of a company that was trying to maximize price / shareholder value. What I read is the proxy of a company and management team that had an activist come at them, got spooked, immediately wanted to sell to the friendliest bidder group the could find, and then rushed a negotiation and put together sloppy and sandbagged financials to justify the bid.

So I think the play here is to buy CLCT around deal price and wait to see if shareholders can push back enough to either force a bump or attract a competing bid (we've already seen some shareholders come out against; I'd really encourage you to read that letter as it has a lot of details on future growth opportunities that the current bid gives no value to). If you asked me to put odds on it, I'd say there's a ~10% chance of a competing bid, a 20% chance of shareholder's pushing back enough to get a bump, and a 70% chance the deal goes through as is. At current prices, you're paying nothing for that optionality.

Rational parties may ask: why would a topping bidder emerge now? CLCT's background makes clear they ran processes in the past at much lower prices without engaging in a sale, and surely bidders could have seen Alta's 13-D as a sign to reach out about a deal. So why is there a shot of a bidder now given no one has bid in the past / since the deal announcement?

I think a few reasons.

We now have an announced deal backed by sophisticated investors. That tends to perk people's ears up a lot more than a simple 13-D.

CLCT has now publicly filed their projections; potential bidders can use those to see what levels of revenue growth and profits CLCT is forecasting and use that to inform their bid.

CLCT is something of a trophy asset. Trophy assets don't trade frequently. Potential bidders have a roughly one month window between now and deal close to lob in a bid. If they don't do it now, they may never get another chance.

I want to dive into point #3 a little further. Owning CLCT gives you the #1 coin and collectible authenticator. There is trophy value to that asset. Plenty of people were big into collecting coins or sports cards growing up; if you buy all of CLCT, you're basically buying your way into becoming the biggest figure in sports cards and coins. You'll be invited to be the key note speaker at basically every conference in those industries going forward.

If you're not a collector, you might scoff at that. But if you're someone who is passionate about collecting who is now a multibillionaire, wouldn't spending $1B (over $100/share) to buy CLCT make sense? At that price and just using CLCT's projections for unlevered free cash flow (which I think are understated), you'd get a 4-5% yield on your investment every year plus the intangible benefits of being the center of a world you're passionate about. Better than bond yields plus growth plus ego benefits? That's the type of combo that can yield pretty big acquisition bids.

I don't want to oversell that ego aspect; you could paint strategic angles to wanting to own CLCT. If you're a big coin or card collector, owning CLCT would likely give you a huge informational edge on what cards are available to buy/sell in addition to that ego bump.

You could even paint a vision that CLCT has untapped marketplace opportunities. StockX, which resells consumer sneakers, just raised money at an almost $3B valuation. CLCT has a platform (collectorscorner.com), but it's small and dated. If you're a buyer passionate about the industry, couldn't you talk yourself into turbocharging CLCT's coin/collectibles platform with the right team and vision and turning it into a multi-billion dollar marketplace?

I'm not sure. Maybe it's a stretch. But all it takes is one investor having dreams of being a keynote speaker or turning CLCT into a multi-billion dollar platform to create some bidding tension here. At current prices, you're paying nothing for any of that upside.

One last thing before wrapping this up (Christmas gift pun semi-intentional)- a big question is what happens with Alta Fox. I do not know what Alta Fox is likely to do; I've seen some speculation that their settlement precludes them from opposing the tender. I don't know. What I do know is:

Connor (Alta's founder), if you're reading this, you should really come on the podcast at some point

Alta Fox's work here has been outstanding; whether they tender into the deal and move on to greener pastures or decide to fight the bid, their work here was great and they deserve all the fruits of their labor

A bump or bidding war is substantially more likely if Alta Fox does come out against the deal.

We'll see in the New Year. Until then, Happy Holidays.