Another deSPAC value idea: $SKIL

I posted a quick deSPAC idea on Alight (ALIT) on Monday. I got plenty of feedback on that piece, and I’ll probably be posting some follow up thoughts in the near future.

But, before I do that, I wanted to post another deSPAC value idea: Skillsoft (SKIL); SKIL recently deSPACd through a merger with CCX.

I’ve seen Skillsoft written up in two other places (ToffCap and SneakyGrowth), so I’ll refer you to those for some extra background, though I will give a quick overview in a second.

But first, I want to highlight why I think SKIL could be such an interesting value opportunity. Yes, it came public through a SPAC, and that’s always a little concerning… but, in this case, I think a lot of stars align:

Skillsoft had been devastated by COVID; the SPAC cash let them accelerate their restructuring and pursue a value added merger simultaneously

It’s coming at a real discount to peers

Serious investors have put a lot of money to work in the PIPE

The sponsor is reasonably aligned with minority investors and has a track record of making money in similar deals.

The CEO’s comp structure screams “there is a lot of equity upside here.”

So that’s my high levels thoughts. I’m going to highlight how their filings lay all of those bull points out; note that this post is not going to be a full deep dive into Skillsoft. Instead, I wanted to write this post because I think a lot of investors will look at deSPAC’d companies and say “O, that’s a piece of junk; easy pass.” I think that initial instinct is a mistake; while a lot of SPACs are certainly junk and/or pure promotes, there can certainly be value hidden inside some of these, and my goal with this post is to prove that / show how SPAC filings can point to some upside.

Let’s start with that quick overview. Skillsoft emerged from a deSPAC merger with Churchill Capital II (CCX). CCX was Churchill’s second SPAC; Churchill has gotten a lot of buzz as a SPAC sponsor because their fourth SPAC (CCIV) is merging with Lucid in one of the buzziest SPAC deals of all time and their third SPAC merged with Multiplan (MPLN), which was the subject of a short thesis I disagreed with.

However, perhaps more relevant from a SKIL standpoint is Churchill’s first SPAC. That SPAC completed a merger with Clarivate and became CCC in mid-2019. With CCC shares currently trading for ~$29/share (versus an initial $10/share in trust), that deal has been an absolute grand slam.

Why is Clarivate so important for SKIL? Because Churchill intentionally set up SKIL to mirror what they did at CCC.

So I just want that comparison lingering in the back of your mind: Churchill isn’t some fly by night SPAC sponsor. They are one of the best SPAC sponsors out there, and they modeled the Skillsoft deal on one of the best SPAC transactions of all time.

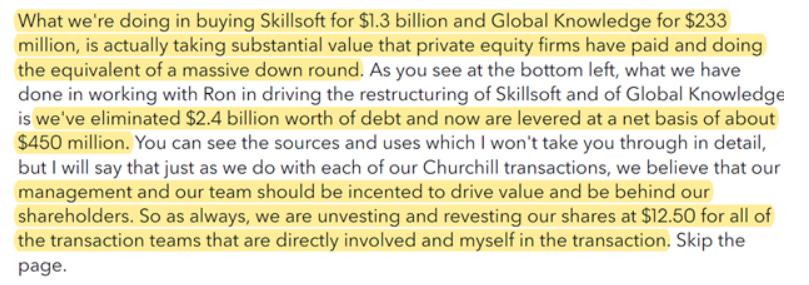

How did they do that? Well, first, they created Skillsoft through a complex transaction. Skillsoft had filled for bankruptcy in June 2020; they emerged in August 2020 (just before the Churchill deal was struck), but the company was still clearly reeling. Churchill used that to swoop in and buy Skillsoft at a cheap valuation while also getting a little bit of a roll up strategy going by concurrently announcing a deal to buy Global Knowledge with Skillsoft.

The Global Knowledge deal is just the start for Churchill; clearly, they want to turn Skillsoft into an edtech roll up.

It’s not just SKIL’s sponsor and M&A playbook that mirror Clarivate; the management team is similar too. Jeff Tarr became SKIL’s CEO once the SPAC deal went through; Jeff was the COO / President of IHS during the financial crisis. His old boss at IHS, Jerre Stead, now runs Clarivate (CCC). So, in Skillsoft, you basically have the same growth playbook, same sponsor, and same management team as you did at Clarivate.

It would be one thing if Churchill had just recruited Jeff as a marketing gimmick (“buy our SPAC; we’re going to rerun Clarivate”.) It would have been simple to do, and Jeff could have demanded a huge cash payout to be associated with CCX. But Jeff seems to really believe in the potential here. Jeff was COO at IHS, and then CEO of Digital Globe for ~6 years until its acquisition by MDA. He could afford to be picky with whatever he wanted his next job to be; pretty much any private equity company would love to have someone with that pedigree running their company. That he chose Skillsoft says something.

But what really speaks here is Jeff’s comp structure. Take a look at the deal he signed to become CEO.

Jeff’s getting $750k/year in salary and up to $1.5m/year in bonus. That’s nice, but it’s not needle moving for him. At IHS, he was pulling in ~$500k/year in salary and another ~$2-3m in bonus (see p. 52). As CEO of Digital Globe, he was making ~$710k in salary and he was getting another ~$3m/year in bonus (see page 35). It looks like his golden parachute at Digital Globe was worth ~$16m in the MDA merger, and I think he owned another ~$20m of stock (see p. 122). He also gets paid $75k/year + $125k in options for his work on board at SATS. So yes, Jeff’s salary and bonus at SKIL is nice, but he’s making less here than he was getting at his old CEO job three years ago. I don’t think he’s doing this for the salary / bonus.

Why is he doing this? Equity upside. As part of his CEO deal, Jeff is getting 1m private placement warrants (strike price of $11.50/share), 2m RSUs, and 1m stock options struck at ~$10/share. If this is Clarivate 2.0 and CCX / Skillsoft hits $30/share in the next few years, Jeff’s equity package is worth ~$100m. If Skillsoft stalls out, he’ll still make good money, but the opportunity cost of having taken this job versus something else will be enormous.

Bottom line: I think Jeff could afford to be very picky with his jobs. The man was set for life if he never wanted to work another day. For him to take this job with a package this heavily weighted to stock appreciation suggests he sees huge upside in the company, and given I think he could be picky in choosing jobs I think it’s a hugely bullish sign that Jeff chose to “shoot his shot” with this company. That Churchill did this roll up strategy before with Clarivate is a cherry on top.

Churchill is also reasonably committed to success here. Churchill structures all of their deals so they receive banking fees for getting a merger done, so their commitment isn’t quite as ironclad as they make it seem, but there’s no doubt that the real upside for Churchill doesn’t happen without the stock performing well.

Bottom line, I think you’ve got a reasonably aligned sponsor and CEO. Let’s chat valuation.

Just an interesting upfront tidbit: CCX bought Skilsoft / Global Knowledge for less than the value of the debt each had going into bankruptcy. Obviously you file bankruptcy because business isn’t going well, but I wanted to highlight that since it shows some of the potential upside.

Aside from that, Churchill / Skillsoft argue they are coming public at a big discount to peers.

Of course, basically every SPAC argues something similar, but I do think there’s a little bit more weight to Skillsoft’s arguments. Skillsoft isn’t arguing they trade for a massive discount to peers on a 2030 basis; they are projecting modest EBITDA growth (and basically flat revenue) from 2020 to 2022 and saying they trade at a discount to peers based on those reasonable assumptions (IMO).

One interesting comp here is Pluralsight (PS). Below are a few quotes from Skillsoft on their valuation / business versus Pluralsight:

Why am I focusing on Pluralsight so hard? Well, first, I think they’re a reasonably loose comp. But I’m mainly focusing on them because Vista agreed to buy them in December 2020, and they had to bump their offer by ~11% in order to get the deal through. That offer was priced at >7x PS’s 2021 revenue estimate (see p. 66 of the proxy); at current prices, CCX is trading for ~2x revenues, so there is a really large valuation gap there.

PS (and yes, that’s a pun; Pluralsight’s ticker was PS)- the Pluralsight deal is interesting as it relates to SKIL in another way. SKIL’s new CEO, Jeff Tarr, has some history with Vista; he signed on to be CEO of Vista’s portfolio company Audatex in May 2019 and left the company in November 2019. That’s really strange, and I’m not sure what happened there. It’s certainly a mini-red flag for Jeff. At the same time, that Vista wanted him for one of their other portfolio companies and then bought a competitor certainly suggests that Jeff’s skills are a good fit for the assets Vista looks at / suggests he’ll be a good fit at SKIL.

There’s also real money coming into the PIPE here. Prosus initially committed to $100m in the Skillsoft PIPE, and they raised that to $500m in total in November. That’s a very hefty check from an investor who is very experienced in the space, and it was written at prices above today’s levels (and the price was agreed in November; equity valuations have run pretty hard since then, and Skillsoft has reported numbers that were generally better than projected, so you’re buying at a discount despite valuations across the board increasing and the company outperforming).

Let me make a very awkward transition here before I wrap this post up. Take it with a grain of salt, but it’s interesting that a sponsor that lead two home runs in Lucid and CCC is calling Skillsoft “the single best opportunity” they’ve found.

Anyway, I’m not pounding the table that SKIL is the greatest value in the history of the stock market. But I do see a lot of positives here:

Sponsor with a good track record who is reasonably aligned with shareholders

At current prices (~$9/share), you’re buying SKIL below where a knowledgeable investor (Prosus) injected half a billion dollars

Management has a track record of creating value with this type of company and is very aligned with shareholders given their equity package

The company is coming at a reasonable valuation and a pretty big discount to peers (who I think you could argue are inferior)

Put it all together, and I think Skillsoft is pretty interesting at these prices. A lot of investors will look at SKIL, see that it used to be a SPAC, and assume it’s a piece of junk and pass on it. My goal with this post was to show how that initial instinct is likely a mistake; I hope I’ve done that!

Would love to get an update on your current thoughts on $SKIL.

Another interesting tell sign - M Klein's brother invested 10M along with Prosus as well. I talked about and invested in CCX/SKIL months ago. https://seekingalpha.com/article/4399602-churchill-capital-corp-ii-leading-elearning-business-hides-behind-undervalued-spac