Multiplan, Part 2: Debunking the short thesis $MPLN

This is the second part in a series on Multiplan (MPLN, disclosure: long). Part one (which you can find here) talked about the potential for a short squeeze in Multiplan. Today's post is going to dive into the weakness I see in the short thesis.

To start, you can find Muddy Water's (MW) full short thesis here. There are a lot of risks presented in the note; the largest / most credible is the risk of losing UNH's business to a competitor, Naviguard. I'll discuss that risk at the end of this write up, but I want to hit on some of the more explosive charges and themes in the short report before I get there.

The first note I'd have is that a lot of the thesis is clearly designed around one thing: SPACs are silly "money grabs".. And I generally agree; I called them the most ludicrous bubble we'll ever see over the summer! A SPAC is simply a financial buyer of a company; they generally win deals because they are the high bidder for a company. Public shareholders get diluted significantly in a SPAC by the founder's shares; that dilution generally amounts to ~20% of the equity value of a company. So a public SPAC shareholder who holds through a deal has, in general, paid a 20% premium to the high bid for a company (because the SPAC was a high bidder to "win" the deal); in general, paying 20% more than the high bid is not a path to riches. There are some caveats to this simplification (for example, the dilution occurs on the equity level, but because SPAC deals generally come with some leverage, the actual dilution is lower and the premium to the high bid is smaller), but directionally this is correct.

Anyway, back to Multiplan: a large piece of the short thesis is "SPACs are silly" versus "MPLN is a zero". That's fine, but "SPACs are silly" has limits as a short thesis. Consider the premium analysis I showed: if the simple argument is that SPACs are taking businesses public at too high a price, eventually that can be solved. MPLN today is trading for ~$7/share; the "deal price" for the SPAC was $10/share and a bunch of sophisticated investors bumped in $1.3B into MPLN at $10/share as part of the de-SPACing process. The difference between $7 and $10/share is a pretty big difference given the huge amount of equity that came in around there; it's worth ~$2B of equity value and ~2.5x turns of EBITDA. If a large part of your thesis is "SPACs are silly and overpay", I would suggest that MPLN's current share price has basically solved that issue!

The SPACs are silly line draws throughout a lot of MW's presentation, but MW does specifically attack MPLN / Churchill in their presentation. P. 12 of their report quotes "former MPLN Executive B" saying that they figured H&F would be "stuck" with MPLN and that H&F had tried to flip MPLN several times to no avail.

I don't think H&F having tried to sell MPLN before Churchill struck the merger with them would really impact the thesis, but it's possible that's true. Churchill hosted an analyst day in August (before they had even finished the de-SPACing process), and even then they were messaging that H&F had not tried to sell the business prior to this (Churchill / MPLN suggested this deal was a mutual thing born out of a desire to accelerate growth at MPLN and do a strategic acquisition). Maybe they're telling the truth; maybe the lady doth protest too much. But MW's claim that H&F has been trying to sell MPLN is certainly not a new claim, and I don't think it materially changes the underlying fundamentals of MPLN's business. Remember, at ~$7 today, we're paying substantially less than trust value, so even if Churchill was the high bidder (or only bidder) for MPLN, we're getting a big discount to that price. Also note that Churchill had raised their SPAC in ~Feb. and had 24 months to reach a deal; while all SPACs face pressure to reach a deal (or else forfeit their founders' shares) at some point, Churchill certainly had no time crunch to make a deal. Again, doesn't mean the deal is a good or bad one, but I tend to be a lot more skeptical of SPACs that reach deals a month before they liquidate than SPACs that have a long runway and can be a little more picky in what deals they pursue.

Another big part of MW's thesis is MPLN's private equity history. The opening paragraph of the short thesis notes that H&F (the PE firm that controlled MPLN before the SPAC process and remains the largest shareholder) was the fourth private equity firm to own MPLN and says that private equity ownership is "a fact pattern that usually means there's little more than a corpse of a business left." I think that's a fallacy; yes, an unreputable private equity firm might try to strip a business to its absolute bones to dress the company up for a sale and make a quick profit. But there's two push backs here

H&F (and every firm that has owned MPLN in the past) are highly reputable firms. I am not saying these guys are saints (far from it), but they are repeat "players" in the private equity game. If they were consistently stripping companies to their bones and then selling them right before the bottom fell out, word would get around and they'd take a huge reputation hit. Again, I'm not saying they're immune to cost cutting or trying to dress up a company's numbers to get a better deal price; I'm just saying that these guys know that their reputation matters for future deals and consistently selling corpses of companies right before they implode is a really good way to get cut out of the M&A game (as well as get a bunch of embittered former management teams who will tell future prospective acquisition targets and management teams not to work for you!).

Turning a company into a corpse and then selling it before it imploded would involve a quick flip / small hold time. MPLN has been private equity owned for almost 15 years; over that time, revenue has grown from ~$353m to roughly $1B. A lot of that growth has been driven by acquisitions, which your mileage may vary on. But the fact remains this business has grown significantly under private equity control, and that growth plus the length of hold time belies the "fact pattern" that the business is "little more than a corpse."

Note that this slide (showing that they've grown a ton under private equity) is not a new claim from Multiplan. Even back at their analyst day in August they were pointing out they had been owned by multiple private equity groups and had consistently grown under their ownership.

Anyway, those two specific themes (SPAC silliness and private equity ownership) run through all of MW's thesis, so I figured it was worth addressing them before going a little more into MPLN specific points.

Turning from general themes to MPLN specific things, the most explosive charge in MW's short thesis is their fourth bullet point "MPLN was already in financial decline, and its financial statements were engineered to obscure this existing deterioration. We understand that in 2018, MPLN released revenue reserves, dropping them from approximately 30% to 10% of revenue, which we believe enabled MPLN to show 2018 EBITDA growth amid shrinking sales." That's an absolutely explosive charge; if true, I'm not sure if it would qualify as outright accounting fraud, but it would certainly warrant an investigation. It's a large enough claim that, if true, I certainly think MPLN's lenders would be able to sue them for breaching their reps and warranties, and it would probably be enough to drive MPLN into some type of restructuring. Given MPLN is now a publicly traded company and, as part of the SPAC process and their recent note issuance, their management team signed off on their financials (which included their 2018 financials, the year MW alleges these shenanigans happened), under the least favorable light / most extreme outcome this is the type of claim that results in jail time for management teams.

Fortunately, it doesn't appear the claim is accurate. The quote below is from MPLN's Q3'20 earnings call (which somewhat doubled as a short rebuttal call).

Obviously, you shouldn't just take management's word on it. But you can go flip through their financials in their S-1; the disclosure isn't great, but I don't see anything that jumps out as me as "extreme reserve release to make numbers." I think the simplest way to look at it is this: MW's claim is that a huge revenue release number helped MPLN grow EBITDA in 2018. If that's true, that would be a pure accounting change with no corresponding cash inflow, and we should see cash from operations (CFO) dramatically lower YoY. But, breaking down the numbers, we don't really see that. CFO was down ~$77m from 2017 to 2018, but this was largely driven by a $101m increase in interest expense year over year. Absent that change, cash flow from operations would have increased from 2017 to 2018, consistent with a company slightly growing earnings.

Again, I'm not saying this is a full forensic audit. MPLN's disclosures leave a lot to be desired on that account. But the numbers seem to back up what MPLN's management is saying: 2018 numbers were not boosted by some random revenue recognition.

Which begs the question: where did MW get that claim? Page 12 of their short report notes the claim comes from "our conversations with a former MPLN executive." It's strange, to say the least, to make such an explosive claim based on the word of one former executive and not by pointing to specific assumption changes or items in the financials.

Reading the short report, a lot of MW's bearishness is based on conversations with former MPLN executives. If one former executive could steer them so wrong (as they seem to have with the revenue recognition thesis), isn't it possible a lot of what these execs said were biased? One of the big issues with calls with former executives is the former executives are often "former" for a reason (they were fired); separating truth from a natural bearishness that comes with being dismissed from a company is a key part of any DD call with a former executive. I'm sure MW knows this, but for the revenue recognition claim to make it into the report without any seeming basis in reality (or specific references to things in the financial statements to back them up) begs the question if MW was looking for a short in the SPAC space and bought into the claims of some bitter former MPLN execs.

The last major piece of MW's short thesis, and the part that I think is most credible, is the Naviguard risk. MW paints the picture as follows

Sick of Multiplan's pricing / describing MPLN's "fee structure as a scam", UnitedHealth (UNH) funded Naviguard.

Naviguard undercuts MPLN's fees, creating pricing pressure. In addition, by avoiding balance billing, Naviguard improves customer satisfaction.

MW particularly hammers home this balance billing point

UNH will switch the majority of their business to Naviguard over the next few years. UNH represents ~a third of MPLN's revenues, so that switch alone would be a disaster for MPLN. However, the disaster would get compounded because Naviguard's new strength will let MPLN's other customers demand significant concessions from MPLN by threatening to leave MPLN, The combination of customers leaving and getting price cuts by threatening to leave will cause MPLN to collapse.

It's a pretty scary short thesis, and one that's difficult to disprove. Saying a client is going to leave for a start up competitor is one thing; I can look at the underlying financials and assess whether that switch makes sense as a risk or not. But saying a client is funding a competitor and will switch to them as a "loss leader" (i.e. regardless of financials) is a much larger risk; MW is basically saying UNH hates MPLN so much they'll cut off their nose to spite their face.

Still, I think there are a lot of holes here. Again, because the risk is so difficult to defend against (if UNH is going to switch away no matter what, there's not much analysis to be done!), it's tough for me to definitively lock down a rebuttal, so I'll just point out some holes in this risk:

Just a general note to start: MW claims that MPLN went public despite the UNH issues because of a "grievous oversight" in diligence by the SPAC promotor (Churchill). That is certainly possible, but it is worth remembering that basically every risk MW lays out were was in MPLN's analyst day back in August. That doesn't mean that UNH will stay with MPLN; they still very well may leave and/or Churchill could have been wrong on their diligence. I just wanted to highlight Churchill was addressing these questions in August because it shows they clearly knew about the UNH / Naviguard risk and got comfortable with it. Again, doesn't mean that Churchill is right or that UNH will stay with MPLN; it just means that Churchill absolutely knew of this risk (or a similar one) and got comfortable with it before buying MPLN.

MPLN / Churchill also suggested on their Q3'20 earnings call / MW rebuttal call that Churchill had performed significant DD on UNH before the merger. I would take that with a huge grain of salt; there was no chance they'd come on a call and say "O yeah, we messed up and didn't talk to UNH." That's why I prefer showing how they were talking about the risks before the short thesis was out there.

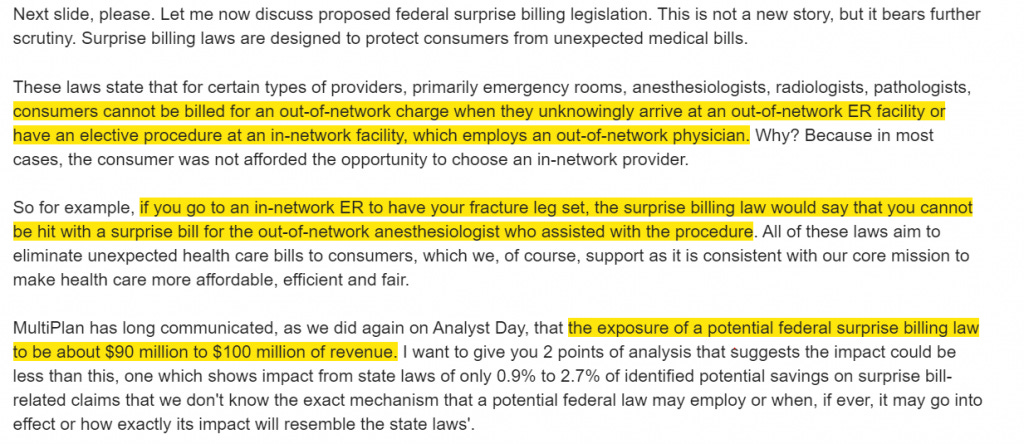

On a similar note, a lot of discussion (but certainly not all!) of UNH switching to Naviguard stems from surprise billing (also known as balance billing). MPLN did a nice job talking about the economics of balance billing and why it isn't a huge risk in their Q3'20 earnings call, so I'll let you read that for more.

Again, I just wanted to highlight that surprise billing is nothing new; it was a big topic of discussion at the MPLN analyst day back in August (see quote below). Again, this doesn't mean surprise billing isn't a risk; I just highlight as another risk that was obviously known when the MPLN deal was struck / the Churchill diligenced and got comfortable with.

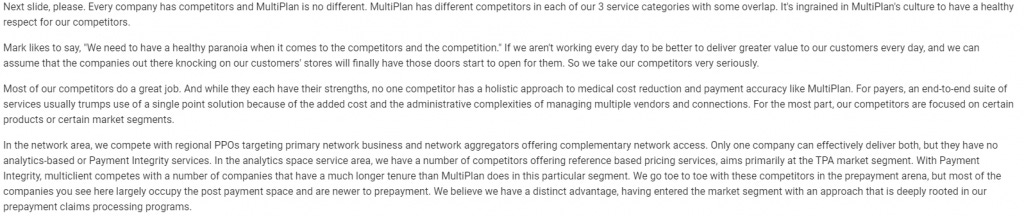

The core of Multiplan's business is simple: if a consumer uses an out of network (OON) healthcare provider, Multiplan uses their scale to handle that claim (see slides below, from Q3'20 earnings, for a good if charitable overview of the business). Just step back and think of this business: this should be a business where scale is helpful; in fact, this should be something of a natural monopoly business with one large player, which greatly supports the MPLN investment thesis and why Naviguard shouldn't make too many inroads here (and why the MW thesis that UNH will use the Naviguard business as a loss leader is so hurtful to the MPLN investment thesis).

Why do I think a monopoly for handling OON payments is the natural endgame? It basically allows for negotiating scale and the deepest network. Consider it from the standpoint below: say you only insure New York residents, one of your members uses an out of network provider in North Carolina, and you get a bill. Yes, you could try to negotiate with them, but your negotiating leverage is awful: no matter how big you are in New York, this is your only case in North Carolina / with that provider. It makes sense that outsourcing that claim should produce better results: if there are ten other insurers just like you with one off cases, and all of you outsource to the same negotiator, then that outsource provider can negotiate with the leverage of ten cases, not just one. And it makes sense for the provider to negotiate with just that one provider: instead of having ten separate negotiations (each with unique administrative costs), the provider can now negotiate with just one provider and get paid across ten cases.

In effect, MPLN has formed a healthcare payment network for OON cases. Providers are incentivized to join to reduce administrative costs / bad debt expenses / improve customer experience; payors join to reduce their claims costs, improve customer experience, and reduce administrative headaches.

Speaking of payment networks, MPLN's investor day included the line below, noting that the only companies with similar margins are Visa and Mastercard. I think that makes some sense, as there's a lot of similarities between the business. Each has high profit margins, but their cut of revenue represents a small amount of the overall dollar transaction they are delivering (the credit card companies take a small percentage of each dollar spent; MPLN is taking a 10-20% cut of what they're saving the payor). Each has a concentrated payor base (issuing banks for the cards; healthcare insurers for MPLN) but a super diffuse provider base that the network needs to do the dirty work of acquiring (over a million healtcare providers for MPLN, tens of millions of merchants for the credit cards). I understand the parallels are loose here, but I do see them and I think they help reinforce why MPLN's economics can be so good and why MPLN's scale should be an unassailable moat.

Note that this moat is not unassailable. MPLN's network only works if there are a lot of OON cases. The more concentrated the U.S. healthcare payor market gets, the worse for MPLN. In an extreme where we went to one nationwide payor (i.e. Medicare for All or something similar), there would be no reason for MPLN to exist (similar to how if there was only one bank nationwide, there would be no reason for Visa or Mastercard to exist!).

Again, the comparison to V/MA is very loose. V and MA are getting paid for processing transactions; MPLN is getting paid for using their network to cut the price of transactions / generate savings.

There are other pieces to the MW short thesis: concentration risk, pricing risk, etc. All of them are reasonable risks, though all of them are in some way tied to the risks discussed above so I won't dive into them here.

But, at its core, MW's piece suggests that Churchill made a huge error in due diligence by failing to account for the risk of UNH leaving them for Naviguard. All of the evidence I see suggests that Churchill did in fact diligence this risk, and everything I can see from a competitive positioning standpoint suggests that MPLN's scale gives them a huge advantage that would make leaving them for a competitor a money losing proposition (even if the competitor offered a lower take rate!).

Could I / Churchill be wrong? Sure! Again, that's why the claim that UNH will leave and treat Naviguard as a loss leader is so powerful; if UNH is leaving regardless of how much money it costs them, then MPLN is in big trouble. But I think that would be silly: MPLN identified $19b in savings for their clients in 2019. UNH is ~a third of revenues, so if you assume they were a third of savings, MPLN saved UNH over $6B in 2019. For those savings, MPLN charged UNH ~$300m. Sure, Naviguard could probably help UNH on some of those savings if they fully switched over, but would UNH really be willing to risk billions of savings to switch from MPLN to a semi-unproven start up? UNH makes ~$15B in net income every year; asking them to take a multi-billion dollar hit to fund a start up as a loss leader for no real competitive reason is a pretty big ask (to say nothing of the pissed off clients getting hit with balance bills and increased medical costs in this scenario!).

Anyway, we should know pretty quickly how real the Naviguard risk is. The MW piece suggests UNH will take 2.4m lives from MPLN to Naviguard in January 2021, rising to 4m lives by June 2021 and all key accounts by the end of 2022. MPLN provided guidance for 2021 alongside their Q3'20 earnings; I'd expect they'd reiterate guidance when they report Q4'20 earnings early next year. If UNH has really pulled a huge piece of their business by then, MW will have been right and MPLN will need to take a huge hit to their guidance (and likely eventually restructure the whole business). So we should know in the relatively near future (or, at latest, with Q1'21 earnings, as even if you think MPLN would try to maintain a fantasy guidance after losing a ton of lives to Naviguard, their Q1 earnings would take such a hit in this scenario that it will become clear what's happening).

It's a risk. But, given MPLN's scale moat, I think it's an overblown one.

One last random note: MW says UNH funded Naviguard. I think they're right (footnote 20 of MW's piece contains a link to this YouTube video, which makes the Naviguard / UNH relationship seem controlled), though I haven't been able to find anything online that explicitly lays out the relationship between UNH and Naviguard (is UNH just a customer, or does UNH actually have a stake / control Naviguard). Just puttign it out there if anyone knows the definitive relationship between the two!