Some more $DISCA / $T ramblings

It's crazy how fast things can change in any part of the corporate landscape once the right dominoe falls.

Last week, basically every major media and telecom company was presenting at Moffettnathanson's conference. I follow the media and telecom space pretty closely for reasons that are very obvious to longtime blog readers (my largest positions are cable companies and media companies!), so I spent most of last week following those presentations. And every media company was projecting the same thing, "our shift to streaming is going well. We have enough assets that we'll be one of the winners as a standalone company; we don't need M&A to have a bright future." While most media followers believed M&A was inevitable in the longer term, it seemed likely that all of the major companies were going to focus on launching their D2C product and getting that off the ground, and then maybe come up for air and assess the M&A landscape after they had gotten better visibility into how their streaming products were doing and what holes they needed to fill in.

Then news broke Sunday that Discovery and Warner (part of AT&T) were looking to merge. By Monday morning, the $100B merger was official. For good measure, Monday night news broke that Amazon was looking to acquire MGM for ~$9B. Within 36 hours, what seemed to be a semi-stable competitive landscape had been thrown completely in flux.

Anyway, I did an immediate blog post Sunday afternoon when the deal rumors were just breaking. Now that we have a lot more definitive news on the merger (when I did the post, we didn't know what the deal would be structure like or even what assets were in the deal!) and I've had a little time to digest the news, I wanted to provide some updated thoughts on the deal.

My overall thoughts remain consistent with my Sunday blog post: I think the deal is an absolute master stroke for Discovery. I am somewhat shocked the market appears to be disagreeing with me; after opening up strongly on news of the deal, DISCK has given up basically all of those gains over the past day or two. As I write this, DISCK stock is trading at roughly the same level as it was on Friday, before the deal was announced.

I think that's an absolute gift; while not without risk, the combination is hugely strategic, and I could see an extremely easy path to the stock more than doubling over the next 3-5 years as the company executes their vision.

I'll talk about more about why I think the deal is so good in a second, but let me back up for a second and talk about a key figure looming over this deal: John Malone (the original cable cowboy). I'm sure most readers are familiar with Malone, but for those who aren't the important things you need to know about him is the man is an absolute legend (he was profiled in The Outsiders and the author of that book has admitted Malone is the CEO he would invest with if he had to pick one), the man never gives up voting control without getting something in return (which became an issue in the LGF / Starz deal!), and the man loves Discovery (he said so as recently as November, and Discovery is one of the few companies where Malone has made an open market purchase and, to my knowledge, the only company he has made multiple open market purchases in). For years, Malone has been saying Discovery would make a successful transition to D2C, and that the company was a free cash flow machine and he loved how they could return money to investors through huge buybacks.

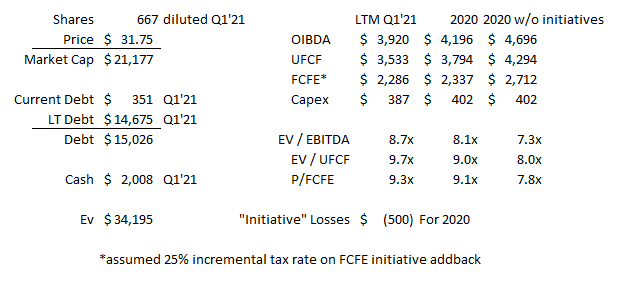

A few months ago, I did a post discussing Discovery in the wake of the Archegos collapse and why I thought the stock was cheap. Below is an updated valuation of Discovery as a standalone company (i.e. assuming the Warner deal doesn't go through); I think the table stands on its own, but please check out my prior piece if you want a discussion of all the assumptions.

So, right now, the stock is trading standalone for <10x EBITDA and free cash flow to equity. Malone is a true believer in this company and loves share buybacks (update: literally as I was finishing up this section, Malone put out a press release reiterating how much he liked this deal).

Instead of just aggressively retiring shares at a low multiple, Malone has chosen to bless a merger that will take share buybacks off the table for several years and has him giving up voting control of Discovery for nothing. In fact, not only is he giving up voting control, but he's largely giving up influence in Discovery; yes, I'm sure he'll still have the ear of the board and management, but T shareholders will own >70% of the company once the deal goes through. I believe Malone will own ~3% of the combined company once this deal goes through, so Malone is literally going from a control shareholder to a shareholder with almost no say once this deal goes through (editor's update: this was sloppy math on my part; Malone will own ~1% of the company once this goes through. My bad; doesn't change the conclusion!).

John Malone is not the type of person to give up control of a company lightly, and he's certainly not the type of person to give up control for free. There are really only two reasons he would do so: he was desperate because he knew the company was about to get destroyed and a merger was the only saving grace, or he thought a deal was so strategic that the value creation from it far, far outweighed what he was giving up.

Obviously, I think the evidence overwhelming points to this deal being one of the later. Malone loves Discovery; I strongly doubt he was desperate. My bet is (and I think all of the evidence supports) that he saw this deal as an incredibly synergistic one, and he was willing to give up control because he knew the combo was that strong.

Again, DISCK's stock is ~flat since the merger announcement. If you agree with everything laid out above, the market today is offering you the chance to buy DISCK at the same price it was trading at before they announced a deal so good that the best media investor in history broke basically all of his historical rules and trends in order to get it over the finish line.

I think that's a gift. Full disclosure: I have bought a lot of DISCK over the past two days. I suspect the stock will be extremely volatile over the next few years as there will be a long time till the deal closes, a possibly contentious regulatory review, and a lot of noise in the integration. But my bet is that, when all is said and done, the merger will be a mammoth value creator, and the stock will be a lot higher.

Let me flip through some other quick thoughts while I'm here

Both the FT and Bloomberg have a deal timeline article out. It appears talks started in February and concluded this weekend. That timeline is hugely interesting because it starts right when Archegos is ripping Discovery's stock higher; remember the stock starts February trading at ~$40, approaches $60 by the end of the month, touches ~$75 by the middle of March, and then crashes all the way back down to ~$40 by the end of March. I cannot wait to read the deal proxy and see how the companies are thinking about valuation while DISCK's stock is moving that quickly through the deal talks.

Another reason I'm interested in the deal proxy: in many ways, this deal would have been more synergistic if it had been announced last year. One of the reasons this merger is going to be so complicated is because Discovery is running Discovery+ and Warner has HBOMax. If they had done this deal a year ago, they could have merged and just instantly rolled all of Discovery's content into HBO's platform. Now, the two companies will have to approach the world with two separate apps (and likely find a way to bundle them together, as Disney does with Dsiney+ and Hulu) or figure out a way to merge the two. So I'm curious to see if Discovery had talks with anyone last year before they launched Discovery+, or if the fact the Discovery+ roll out seems to have gone so well emboldened them a little bit to swing for the fences in a merger.

I'm also curious from the T / Warner side and how they approached strategic decisions. I'll discuss this later, but both reporting and my gut suggests they really thought about going with Comcast / NBC instead of Discovery, but given Comcast's size and the fact T has fought the DOJ twice in the past ten years, I don't think T had any appetite for the regulatory risk that came with a Comcast deal.

I made this point a little in Sunday's piece, but the combined Discovery / Warner will have the second best brands in media (behind Disney). I'm still trying to think through their content spend (their deal language and call was a little confusing; I'm not sure exactly how much of their spend goes to linear and for sports rights versus straight content investment), but I think it's safe to say that the combined company and Netflix will be, by far, the two biggest content buyers in the world when this deal is done. Given how weighted DISCA is to cheaper reality type shows, I think Discovery Warner will be head and shoulders above anyone else when it comes to sheer volume of content released. I just make this point to drive home that Discovery, Disney, and Netflix will be head and shoulders above everyone else when it comes to a streaming service; this is just a killer deal from a strategic perspective as you lock in a top-three with scale beyond and brands way better than everyone else, and you take any pieces that could get a smaller competitor into the top-3's league off the table.

The synergies for the deal won't be bad either! The company is guiding to $3B in cost synergies, but I think there should be real juice on the revenue side as well. The combined company should have much better operating leverage in negotiating deals with the legacy cable bundle, I think the opportunity to bundle HBOMax and Discovery+ can get really interesting in terms of value they offer subscribers, and the larger size of the company should create interesting optionality on the advertising side (both in terms of better targeting and striking brand deals).

The table below is how I'm looking at value for the combined company right now; I'm guessing that's how most other people are too. So, just on these numbers, you're paying ~9x EBITDA and FCFE on their 2023 guide. Obviously that's pretty cheap, but I think it's even cheaper than that headline number when you factor in a few things

The 2023 guide doesn't include their full run rate synergies yet; they probably won't be fully done with synergy realization until 2025.

This also doesn't include any of the revenue upside opportunities discussed above.

Discovery and HBOMax are both making huge investments into their streaming services; right when all of the synergies start to flow through is when their investments in the streaming services should really start to scale.

Anyway, bottom line if you add up those three points: I think the projections way understate the economics of the combined company; 2024 and particularly 2025 should be materially better than this if they successfully integrating.

Discovery will generate billions in free cash flow between now and merger close. In addition, the combined company will be generating multi-billions of free cash flow every year after the deal closes. This is a pretty levered company, but by the time the deal closes and the synergies start flowing through, debt is going to come down quickly and all of that value should accrue to equity.

Given everything above, I will be very interested to see the deal proxy and the projections that they lay out in there. I suspect that could be a mini-catalyst for the stock, as people get bullish on rosier out year numbers.

One question I have been thinking about with DISCK: opportunity cost. The combined DISCK / Warner is trading for ~$130B (as shown above). Yes, it looks cheap on trailing numbers, and I think the combo is a really good one.... but obviously a lot of the value comes from the legacy media bundle that is eroding. Netflix is currently trading at $225B; yes, it's more expensive on near term numbers (it trades for ~30x next year's EBITDA), but they've already shown they can successfully scale and they won't have any of the merger noise or issues or slow timeline that DISCK + Warner will face. Maybe the right play here is to just buy the best company with the best leader in the space (Netflix)?

Just to frame that a different way: would you rather have DISCA / Warner today for ~$140B, with tons of cash flow that is facing secular issues and interesting assets but challenges getting to the future / integrating? Or Netflix for ~$225B, with not a lot of current cash flow but absolutely dominant distribution and execution and absolutely no questions about their place in the future?

I noted above that I thought the combined DISCA / Warner could match Netflix for content scale. Let's just say that you think the combined company could hit Netflix's current valuation in the next few years ($225B). I don't think that's completely unreasonable; it's a little over 16x their 2023 EBITDA estimates. On today's cap structure, DISCA would be a >$75/share stock at that level. But the company will also pay down billions of debt in the medium term; factor that paydown in and I don't think it's unreasonably to think the stock could trade towards (or above!) $100/share if the market starts to get really comfortable that the merger is a success and Discovery Warner will be one of the three dominant scaled global media players.

There's going to absolutely be a wave of M&A on the heels of this, and the market is certainly picking up on that! On the heels of the deal, the big "losers" have been basically all the major media and telecom players, and the big winners have been all of the remaining free radicals.

I don't thinks it's a coincidence that a few hours after this deal was announced the AMZN / MGM rumors leaked. I wonder who planted that story.

Both Comcast and Viacom are obviously going to need to consider some M&A to scale up or they're going to get left behind on the heels of this merger. Again, the market seems to have picked up on that by sending all of the free radicals higher, but there aren't a ton of targets left out there. To my knowledge, the digestible assets left are MGM, AMCX, Lionsgate, Sony Pictures, and then.... nothing?

Obviously Lionsgate has to be thrilled to see this deal announced; they're probably the best / most strategic free radical left so they might command a big premium if VIAC or Comcast gets desperate.

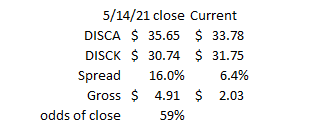

Speaking of desperate, it's tough to understate what a tough spot this puts Comcast and Viacom in. I know a lot of people think Comcast might come in over the top for Warner, and the market seems to be implying some chance of that happening. As part of this deal, DISCA and DISCK will collapse their share class. DISCA was trading at a ~15% premium to DISCK before the deal was announced, and it's currently trading at a ~6% premium. Just using those, the market is implying only a 60% chance of this deal closing. That seems much too low to me; obviously there is a little regulatory risk here, but the biggest risk is definitely a bidding war for warner breaking the deal up. I struggle to believe that will happen; Warner was clearly scared of regulatory risks and T doesn't want the headache; I'm not sure how CMCSA can alleviate those concerns.

Speaking of bidding wars, I think it's significantly more likely someone (either CMCSA or VIAC) comes over the top for Discovery than someone comes over the top for Warner. Why wouldn't someone target DISCA? Paramount+, HBOMax, or Peacock are all subscale without Discovery and all of them can hit scale with it; there's no other asset out there that gives them that optionality w/o an insane amount of regulatory risk or headache. If either VIAC or CMCSA bid for Discovery (and won!), they'd put HBOMax in the exact same quandary that they are currently facing! I may be the only one who thinks so, but I think there's a serious chance of either of them looking to compete for DISCA. Both of the last major "strategic" media mergers saw pretty intense bidding competition (Comcast/Disney bidding war for Fox; Discovery / Viacom bidding war for Scripps); it would be historically strange if this process went through without some type of bidding pressure!

Speaking of bidding wars, I thought the termination fees for superior proposals in the merger contract was interesting. Remember, Discovery standalone is a $21B company. They are trading where they were before this deal was announced; if the deal breaks, they'll get ~$1.8B in break up fees. That's a lot of cash for their troubles!

Another reason DISCA stock will be volatile over the next year? Shareholder overhang. Tons of people own T for the dividend; if they spin out the DISCA shares, suddenly you're going to have >70% of the company in the hands of dividend focused investors. DISCA won't be paying a dividend, so that could create some real selling pressure when the deal closes. I'm cognizant of that potential pressure, but I think the combined company is so cheap (and the optionality from a bidding war for DISCA is so good) it's worth owning in front of that.

Hilariously, the WSJ had a long profile of current Warner head and soon to be retired Jason Killar last week. I wish I could have been a fly on the wall when that article hit the desks of the top brass at DISCA and T. I wonder how they responded; I'm guessing a heck of a lot of laughs at DISCA and I'm guessing a lot of awkward pauses and maybe an immediate call to legal to figure out how to settle a severance package at T?

Anyway, I'm still thinking through this deal, and I'm sure I'll have more to say in the near future. But I love this deal, and I think buying DISCK at no premium to the pre-deal price is a really unique opportunity.