Yet another guide to media stocks, Part 3: Sports Rights, RSNs, and ESPN $DIS $SBGI $MSGN

Hi! Welcome to Part 3 of Yet Another Guide to media stocks. This part will cover everything sports rights, particularly ESPN and the Regional Sports Networks (RSNs). Before diving in, I'd highly encourage you to check out the intro section to the guide, which goes over why I'm doing this and dives into the most important thing hitting the media sector today: cord cutting. You can also find links to all of the pieces in this series here. I also wanted to highlight that I put out an update / correction to yesterday's post on networks; please check that out if you haven't yet! That out the way, on to part 3: sports rights and RSNs. I'm from New Orleans, and growing up the Saints and the Pelicans (football and basketball) were huge parts of my life. I'd go to ~2 Saints home games and ~10 Pelicans games every year. I watched every game pretty much religiously. For a while, a friend and I even wrote basketball articles for a relatively popular local Pelicans blog. So when I moved to New York, one of the critical questions facing me was how to watch the Saints and Pelicans. After all, a cable subscription only carries local games (i.e. in New York, the Knicks and Nets for basketball. And honestly, who wants to watch the Knicks? Speaking of the Knicks and how much they suck, now might be a good time to disclose I am long both MSG and MSGN!). For me, the solution to the "how to watch my teams" problem was to buy NFL Sunday Ticket and NBA league pass. At the time, I believe Sunday Ticket was $200/year and League Pass was $150/year. And, because the video bundle didn't carry the sports teams I wanted to watch, I cut the cord and didn't subscribe to video package; I simply used my cable company for broadband, streamed Sunday Ticket and League Pass, and used Netflix for any entertainment stuff I wanted to watch. I know what you're thinking.... Cool story bro, what the heck does this have to do with media investing? Well, at the time in Louisiana, I think I was paying ~$80/month for a video package. Literally the only thing I was watching on it was sports, mostly the Pelicans and Saints. The local Pelicans RSN was getting maybe ~$5/month/sub, and the local Fox station (which carries the Saints local games) got maybe~$1.50/month. That's a mammoth value mismatch: I probably would have been willing to pay $80/month just for the Saints and Pelicans and getting nothing else, yet the Saints / Pelicans were getting <10% of my subscription fees. This issue works in reverse for non-sports fans, too. ESPN costs ~$8/month. If you don't watch sports, ESPN and the Pelicans RSN alone would cost ~$13/month. ~15% of your monthly video fees are going to two channels that have zero value to you. In the intro I showed a simplified cable bundle ecosystem to illustrate how the cable bundle eventually breaks itself as it's in each channels interest to raise prices despite the fact the price raises slowly cause the bundle to collapse. I wanted to show another ecosystem just to highlight how central a roll sports plays in this. Below is a simplified cable ecosystem; similar to the intro, the box in the middle shows how much value each customer gets from each channel. The top shows how much the channels charge per sub (all charge $10/month), the bottom bold line shows the total value delivered by each channel, and the bold on the right shows how much value each customer gets from the bundle.

Customer 1 is basically modeled after me a few years ago: someone who only subscribes to the bundle for sports. So is customer 2. All the other customers range from marginal sports fans to people who don't care about sports. This is a really interesting bundle. Sports delivers way, way more value to the bundle than it gets in pricing.... yet there's no way it's ever going to get as much revenue as it does in the current bundle (assuming it can't perfectly price discriminate). It currently gets $100/month by charging 10 subs $10/month. The next best it could do would be to take its price to $45/month, where it would get two subs and make $90/month (in addition, advertising revenue would drop massively as ratings went down, and the sport would be killing its longer term future if they priced themselves so high that only 10 or 20% of the population could afford to watch it; good luck getting new young fans!). So sports is always going to be pushing for price increases arguing it delivers more value than it gets... but each other channel has the same argument, and the moment one of them gets a price increase is the moment the whole bundle collapses. To be fair, this isn't a scientific overview. I just threw some numbers on a spreadsheet. But I'm near certain they are directionally correct. If we assume they are, there are some really interesting takeaways.

Sports almost certainly deliver a lot more value than they get despite the fact they are the highest paid piece of the bundle

Sports channels are constantly incentivized to increase their price

Increasing their price is eventually going to cause the whole bundle to collapse

Sports maximizes its revenue in the bundle; even ignoring the drops in ad revenue from fewer viewers, there's no way for sports to monetize better than it does currently.

So just keep all that in the back of your mind as we jump through the different pieces of the sports ecosystem. There are a few ways you can invest in sports rights in the public markets: you could go buy a publicly traded sports team (BATRA, MSG, MANU. I'm long BATRA and MSG). You could buy a publicly traded sport (FWONA; WWE). Or you can buy an RSN (MSGN is a pure play; SBGI is a hybrid RSN / local broadcaster). The networks (FOX, ABC) also have significant exposure to sports rights. Personally, I'm bullish sports rights and bearish the current sports rights holders (RSNs, networks, etc.). My personal view is the sports rights are the most unique things out there: guaranteed to drive eyeballs and attention with huge passion. If there's one thing we've learned about the internet, it's that passion monetizes. You know what's better than selling a blockbuster game for $60? Giving the game away for free, grabbing a massive audience that gets really passionate about it, and then monetizing that audience through advertisements or microtransactions. Sports is going to do gangbusters as they get more and more consumer data. My guess is that the sports leagues all eventually take their sports rights back and launch direct to consumer apps that they can monetize through hyper targeted advertising and merchandise sales. Look at Disney Plus; 10m people signed up for it on its first day. Sure, it involved Disney making a massive near term investment to get the majority of their rights back, but it certainly looks like that bet is going to pay off. How many people would sign up day one if the NFL announced the only way to watch their games going forward would be through the NFL plus app? If the NFL suddenly had millions of subscribers with all of their personal information (plus an active credit card) downloaded in an app, how lucrative would the marketing opportunities be? Imagine them pitching your favorite teams jerseys right after they clinched a playoff spot. Opportunities for exclusive meet and greets with the star players. Season ticket marketing. Etc. It would be enormous, and we haven't even discussed sports gambling yet.... So I think sports rights are going to be massively valuable going forward. However, I think all that values accrues to the sports franchises themselves, either because they do it directly (as mentioned above) or because other people compete furiously for the rights and the bidding wars drive the price up to where there's limited economic value left for whoever wins the rights. A particularly interesting dynamic here to think about is what happens if current sports rights holders go D2C (i.e. your local sports RSN drops out of the bundle and forces people to download their app to watch games / subscribe). Going D2C is a massive investment: huge upfront costs for tech and marketing spend, you need to acquire customers, etc. It's most likely going to take ~5 years to hit breakeven (Disney Plus, for example, won't be breakeven until FY2024). I believe most RSN sports rights deals are in the 7-10 year range; there are certainly exceptions (MSGN spun with 20 year rights to the Knicks / Rangers, and SBGI has said the average of their RSN sports is ~11 years, though I question that number a bit (which speaks to how much I trust SBGI's management!)), but I think 7-10 years is pretty standard for RSN rights (just to show three examples, the Hornets recent deal was rumored to be 10 years, a prior Detroit team extension was for 10 years as well, and this article mentions Fox deals being for more than 5 years). If you sign a deal for 7-10 years and go D2C, your app is going to be hitting profitability just as your next rights renewal comes up, then the local sports team is going to have you over an absolute barrel in negotiations. Pay top dollar, or they're going to pull their content and that app you just built is going to be borderline worthless. You might argue that 1) the investment is a sunk cost and 2) won't the other bidders be wary that the same thing will happen to them if they steal the rights away? I'd respond that 1) true, it's a sunk cost, but if you're the manager who sunk that cost and it goes to zero, you lose your job, so you're probably pushing as hard as you can to renew the rights, shareholder value and sunk costs be damned and 2) the sports team could just offer the next bidder 15-20 years to encourage them to bid hard and overcome their fears of having the rights pulled. So I'm really bullish on the overall value of sports rights and believe the vast majority of that value accrues to the sports leagues / teams. That leaves me bearish the current rights holders. I want to talk about three different companies in particular when discussing the current rights holders: There is one company that I'm particularly bearish on: Sinclair (SBGI, a company I previously called "completely uninvestable"). To review, SBGI acquired the Fox RSNs from Disney earlier this year. The headline purchase price was quite low, and included significant tax benefits. In addition, given the company was using a significant amount of leverage for the purchase, the cash flow accretion to shareholders was enormous.

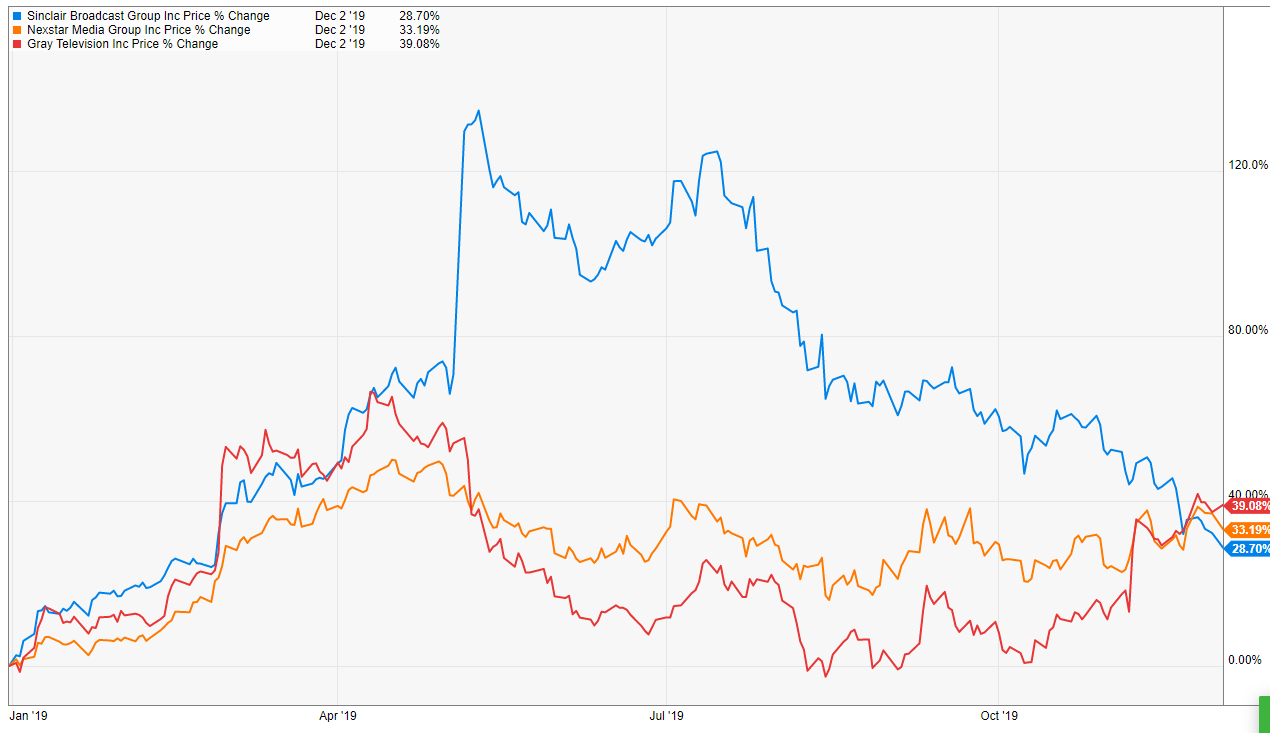

It's tough to fault a company for going out and buying something at a really low cash flow multiple, particularly when it's something like a cable network that should have relatively stable, contracted cash flow, and with possible upside from sports betting (either from launching a sports betting product they own, or simply from getting tons of revenue from advertising and tie-ins). But I think SBGI made a big mistake. Why? Well, Fox's RSNs had always been negotiated with the stick of Fox news behind them. If you tried to drop the RSNs, you risked losing Fox News in every market (plus Fox in the stations Fox owned the local affiliates). That is a really powerful, nationwide stick behind the Fox RSNs; sure, the RSNs are expensive, but if you want to drop the Fox RSNs you're losing the most popular cable channel as well. Sinclair, in contrast, only has their local network affiliates as a stick to force companies to negotiate. That's a stick, sure, but it's no Fox News. And it doesn't have the same nationwide appeal as Fox News; Fox News provides protection in every place nationwide, while Sinclair's local affiliate portfolio only provides protection in places where there is overlap between Sinclair's local affiliate and the Fox RSNs. For example, Sinclair operates the local affiliate in Flint and Traverse City (Michigan), and the Fox RSN portfolio included the Detroit RSN (Red Wings, Pistons, and Tigers). That provides some protection, but not a ton. In contrast, viewers all through Michigan (including, most importantly, Detroit) watch Fox News. When someone negotiates with Sinclair, they can drop the RSNs knowing that they'll get an affiliate blackout for one channel in a few markets but not all. If someone dropped the RSNs under Fox's watch, they get a nationwide blackout of the most popular cable channel (Fox News). That's a much different stick. Sinclair should have been underwriting significant potential pricing compression when they bought the RSNs, as their negotiating leverage had substantially weakened. Sure enough, right around deal close time, Dish blacked out the Fox RSNs, a blackout that continues to this day, and Sinclair has given up all the share price gain it got when they made the RSN purchase and has now performed worse than it's peers YTD (not that YTD stock price performance means anything, but I just highlight it since they had literally doubled on announcing the RSN deal and now that questions are emerging that has more than reversed).

A long term blackout is really, really bad for an RSN. An RSN's leverage is pretty simple: if you drop us, all of our passionate fans are going to leave you for someone who carries us. That's a really powerful stick; however, once the RSN has been dropped, the stick isn't there any more: after a few weeks, all of the people who cared enough about the team to switch providers have largely done so. Now the distributor who dropped the RSN faces new math: if I pay up for the RSN, then I have to pass that cost on to all my remaining customers... who don't really care about the RSN and don't value that RSN (remember, the customers who cared enough about the RSN to leave have already done so!). If I don't pay the RSN, I can cut pricing to my current subs and I'll be permanently cheaper than competitors, which might let me peel some of their non-sports fans to my cheaper bundle over time (Dish discussed this exact strategy recently). There was a really interesting lawsuit a few years ago over collusion between DirecTV and some other cable providers to keep the Dodgers new RSN off that goes over some of this math; I can't easily find a shareable copy of the lawsuit, but it was really interesting and the summary alone is worth reading. Anyway, my point is this: now that the Fox RSNs have been dropped from Dish and Dish has taken that initial pain, I doubt that Dish is ever going to take the RSNs back (DISH discussed this dynamic a bit in their Q3'19 call). And that's going to really reduce SBGI's leverage in future negotiations with other distributors. Previously, when negotiating, SBGI could go to the local cable company and say "you better pay us; if you black us out, think of how many subs are going to switch to Dish to get us." Now that threat is gone; the cable company is the only place for fans to get the RSNs. If the RSN prices too high, the cable company might black the RSN out and fans have no where to switch to (this is somewhat similar to what's happening in Denver with the Altitude RSN). Also, think about the blackout from the sports team perspective. Viewership is absolutely critical to the sports team: it drives fan engagement, merchandise sales, popularity, season ticket sales, etc. If you're a team and your RSN gets blacked out, you're not going to be very happy. You're going to be leaning on Sinclair constantly to get back on the stations, and you're definitely going to remember is the next time your rights are up for negotiation. So Sinclair paid a low price for the RSNs, sure. But the earnings stream they bought was always very vulnerable and almost certain to decline under their watch. RSNs are a high margin business with mainly fixed costs; with Dish blacked out, the RSNs earnings and value are quickly dropping, and I wouldn't be surprised to see more blackouts in the future and/or Sinclair need to pay a premium to maintain their rights when they come up for negotiation simply because current teams don't trust their ability to deliver the largest viewership possible. Ok, at this point hopefully I've driven the point home that I'm bearish RSNs in general and SBGI specifically. Which begs the question: why do I own MSGN? I view MSGN as something of "an exception that proves the rule" company. for a few reasons.

They have an exceptionally long life on their RSN rights; they have the Knicks and the Rangers rights till ~2035, and I believe they have a significant amount of time remaining on their other sports teams (Islanders, Devils, and Sabres, though I can't find the exact lengths quickly). Those are really long lives, which will allow MSGN to invest into future products (i.e. D2C) without worrying they'll lose their rights just as their investments are starting to payoff.

I can't imagine a worse environment for MSGN to be negotiating in than they have the past few years: unlike Fox's RSNs, MSGN has never had the stick of a large nationwide network to provide them extra negotiating leverage. In fact, since MSGN is a standalone channel, they've never had any type of "stick" to negotiate with. And on top of being "stickless," MSGN's teams have generally sucked for the past few years. Poor team performance is death for an RSN; if your team sucks, fans don't bother turning into late season games. Ratings go down. If ratings are down and fans aren't tuning in, there are less people who will cancel if a distributor drops your channel, which provides less leverage in negotiations. So MSGN has been negotiating without another channel to boost their leverage and without the benefits of a good team. Things literally can't get worse for them from a negotiating standpoint... which provides a ton of potential synergies to a potential acquirer of MSGN. For example, Sinclair has made no secret of their desire to buy more RSNs. If Sinclair bought MSGN, there would be natural synergies as Sinclair's threats of blackouts for the rest of their portfolio would now include a blackout in the large NY market, and MSGN's negotiating leverage would be improved because they'd have the stick of Sinclair's channels behind them. On top of that, there would be some G&A synergies, but I'd guess that's small compared to the improved leverage. Also, and I say this somewhat fearfully as a basketball fan living in NYC, but at some point the performance of the Knicks / Rangers has to get better. I'm not expecting championships here, but at some point the Knicks have to make the playoffs, right? I mean, more than half the teams in the league make the playoffs; it's honestly impressive how infrequently the Knicks manage to make the playoffs given they have the natural advantage of playing in a large market. But, at some point, the teams will be decent; when they are, ratings will improve, and MSGN's leverage goes up. I would guess any natural acquirer would look at the team's performance and see some upside potential there as well.

MSGN's market is unique; it's one of the best in the country. NYC is richer and more populous than almost every other RSN's market, so MSGN will get better advertising revenue than peer RSNs. NYC is a particularly competitive video and internet market, with most households having access to two or even three providers, so customers will find it much easier to switch providers if there's a blackout and the customer wants to chase sports programming.

Ok, that covers the two major publicly traded RSNs. The last company I wanted to talk about when it came to sports rights is ESPN. I wish I had something unique to say on ESPN, but unfortunately I don't: I think the channel is in a lot of trouble. Ten years ago the company's moat was enormous: they were the only sports channel in every household, so they had the best reach. Because they had the best reach, they could afford to pay top dollar to sports leagues and justify that spending because they could amortize it on a larger sub number (i.e. if ESPN and Fox Sports both bid $100m for right, ESPN would be paying $1/sub because they had 100m subs versus Fox at $1.25 because they only had 80m). In addition, leagues wanted to be on ESPN because a larger audience would make their sport more popular (I think one of the reason the NHL's popularity has dipped is it's no longer on ESPN), and ESPN's larger audience meant they would get more advertising revenue than peers when airing games (more viewers = more advertising, and more advertising revenue again let ESPN bid more for sports rights than competitors and still be profitable). ESPN also had a massive moat on the in-between hours: they were the only place you could go to see highlights of games, and things like SportsCenter and other day time programming was really profitable for them (they would be highly watched, because they were the best place to see highlights, but they also didn't cost much to make). Today all of those moats are crumbling around ESPN. Highlights and analysis are easily available instantaneously online, which has demolished the franchise value of SportsCenter and a lot of the "talking heads" shows. There are plenty of other companies with similar reach to ESPN (for example, both Amazon and Netflix have >60m domestic subs), and plenty of new platforms can scale up tens of millions of users in quick succession if they have content people want (years ago, if you wanted to bid for a sports deal and launch a new channel, you'd need to go region by region and negotiate carriage with each distributor. Today, you could just release an app and do a marketing blitz, like DAZN has done). And ESPN, of course, faces what I've called the ESPN problem: it signed a bunch of sports rights deals when it had 100m subs, and now their subs are at 80m and dropping. That creates some significant operating deleveraging, and suddenly those contracts are much more expensive than ESPN had originally projected. The household also decreases ESPN's negotiating leverage when getting new sports rights: previously they could tell leagues that being on ESPN would get them more viewers and fans than any other channel, but as ESPN loses subs that argument gets less and less relevant. I also think ESPN is fighting against a few other trends

I've mentioned several times already that I think long term sports leagues take back sports rights for themselves, or at a minimum extract so much in price that whoever "wins" the sports rights can't make an economic profit. ESPN obviously wouldn't do well in either scenario.

ESPN is focused on all sports nationally; I wonder if the longer term trend is for fans to be more passionate about individual sports and individual teams, and the future belongs to people who focus on that instead of providing a broad sports bundle. You can see some early signs of this in ratings: YTD NBA ratings are apparently down a decent bit, but RSN trends are better. This is a pretty small sample size, but it would argue that fans are increasingly care only on how their team is doing versus the overall NBA. You can see some of this in baseball as well; World series ratings continue to decline, but local television ratings on the RSNs have held in strong.

I'm not saying this argument is set in stone or even correct; just that there are some trends pointing that way and they certainly wouldn't bode well for ESPN.

The other piece of this argument is that ESPN rolling all sports into one "ESPN" app isn't going to be as popular as launching individual apps aimed at each sports (an NBA app, NFL app, etc.) and then monetizing that user base with micro-transactions, targeted ads, etc. Perhaps there is scale and cross subsidization between the sports (if you're a super basketball fan, you're more likely to be a fan of other sports, so ESPN bundling all of them together attracts a larger user base), but I'm not sure that's the route to go versus focused.

Let me try to come at this from a different angle: up till a few years ago, the dominant form of selling video games was selling them for ~$60/month. Then, fortnite and candy crush came along, and they showed monetizing by getting a huge user base and then charging super fans could actually generate a lot more revenue. Currently, ESPN is basically the old video game model: they buy a bunch of sports rights and then charge distributors for the right to carry their programming. I'm not convinced that's the long term model; it may be better to go direct to consumer and give the games away for free (or just charge them for each league they want to watch), and then monetize the super fans with targetted ads, in game betting, selling tickets to events, etc. ESPN's current model of buying as many sports rights as they can across a bunch of different leagues would be very poorly suited for monetizing super fans of a bunch of different sports, and I'm not sure they have any of the capabilities to move them to a microtransaction world. Perhaps they could develop those capabilities, but I think there are tons of other firms that could and ESPN wouldn't really have a moat in that world.

Of course, there is some counter to this: any league that goes direct is going to face huge churn issues (i.e. why would I subscribe to an NFL app when the NFL isn't in season?). Bundling a few sports together could reduce churn and get a bigger market.

While sports are likely to remain wildly popular going forward, I think it's likely there are fewer fans devoting less time to sports in the future. Between video games, Netflix, and videos of dogs doing dog things, there are more entertainment options than ever before, and while I don't think sports are going anywhere, an increase in options should lead to a decrease in viewership and fans over time. ESPN is playing against that trend.

Anyway, I don't have all the answers on ESPN. But it's in a really tough spot, and it's impossible to talk sports rights without acknowledging that. Odds and ends

Literally as I was wrapping this up a NYPost article came out discussing the yankees streaming some games directly through Amazon. Don't think it changes anything in the post; it just kind of highlights how the value of sports rights will likely accrue to the Sports teams in long term.

Did I think I was clever for modeling out a fake little cable ecosystem in today's post and the intro? Yes, yes I did; it's not exactly groundbreaking but I figured it was something kind of new on the free internet. Sure enough, yesterday I saw this article on the car bundle, which included a link to a 7 year old article breaking down the cable bundle with way better charts than I make. Rats.

One bull thesis I didn't really cover here is advertising. Yes, sports betting should open up a bunch of demand for advertising, but I think there's real money to be made in more targetted advertising. Sports is one of the few things left that demands engagement in real time and where consumers will sit through a huge commercial ad load. As sports goes more and more through D2C apps, more targetted advertising opportunities are going to present themselves, and advertisers are going to pay a fortune for those slots (I mentioned in one of the earlier pieces that AT&T had talked about getting 4x more for targetted advertising versus programattic; I wouldn't be surprised if sports gets a slightly bigger premium for targetted just because it's in real time, completely brand safe, and the association with sports is good for advertiser's images).

One interesting thing to think about: if the endgame for a league is to go directly to consumers, does that decrease the incentive for teams to tank currently? Right now, if a team tanks and its ratings go down 50%, the team doesn't super care: they get the same contractual RSN revenue no matter what. But if the teams eventually go direct to consumer, a team tanking is going to see massive cancellation in their D2C subscriber base, and the owner's wallet is going to take a big hit. Will this encourage more teams to fight for mediocrity / a playoff spot versus tanking and hoping to land a superstar (I am specifically thinking of basketball here, though I believe baseball has just as mammoth a tanking problem)?