Premium case study: $GHIV SPAC-"option arb"

One of my goals for YAVB in 2021 was posting more case studies: ideas from YAV premium that have played out (whether positively or negatively). There are a lot of reasons for doing so: partly for marketing purposes for the premium site, partly because some people get value in seeing fully written ideas and learning from them, and partly (mostly) because when I write I often like to link to past ideas and thoughts and having them behind paywall makes that writing / linking a little awkward. So today I'm following through on my goal and posting the third in an irregular series of premium case studies.

This case study was posted in early December. The idea was simple: buy-write GHIV to create the stock for ~trust value. Worst case scenario, the stock fell and you redeemed to basically get your money back. Best case, the stock ran and you'd make a pretty nice profit. Either way, the trade was reasonably riskless (Disclaimer: nothing is riskless, and nothing on here is investing advice).

The idea played out perfectly. GHIV traded up slightly (to $12.40/share), and the redemption date was set for last Friday (the same day options expired). Net, the buywrite returned a little over 20% in ~a month, and given you had the redemption rights on the backend it was a very well protected trade.

Below is the idea as originally posted to the premium site in early December.

Recently I’ve posted two articles on taking advantage of SPACs with high volatility: The curious case of PSTH’s options, and assessing IPOC’s options. The basics behind these trades are simple: volatility on some of these SPACs is absolutely off the charts, and if you structure the options correctly you can take advantage of that optionality to create the SPACs at huge discounts to trust value.

I’ll admit that these are much more “trades” than investments. You’ll notice that the posts had absolutely no mention of fundamental value; heck, PSTH hasn’t even announced a deal yet so there’s no company to discuss fundamental value on! So I know these are a little different than what the premium site generally puts out. Still, I think these trades are incredibly attractive, and I want to make sure that premium subs are getting access to my best stuff, so I wanted to highlight one more of these SPAC options just for premium subs.

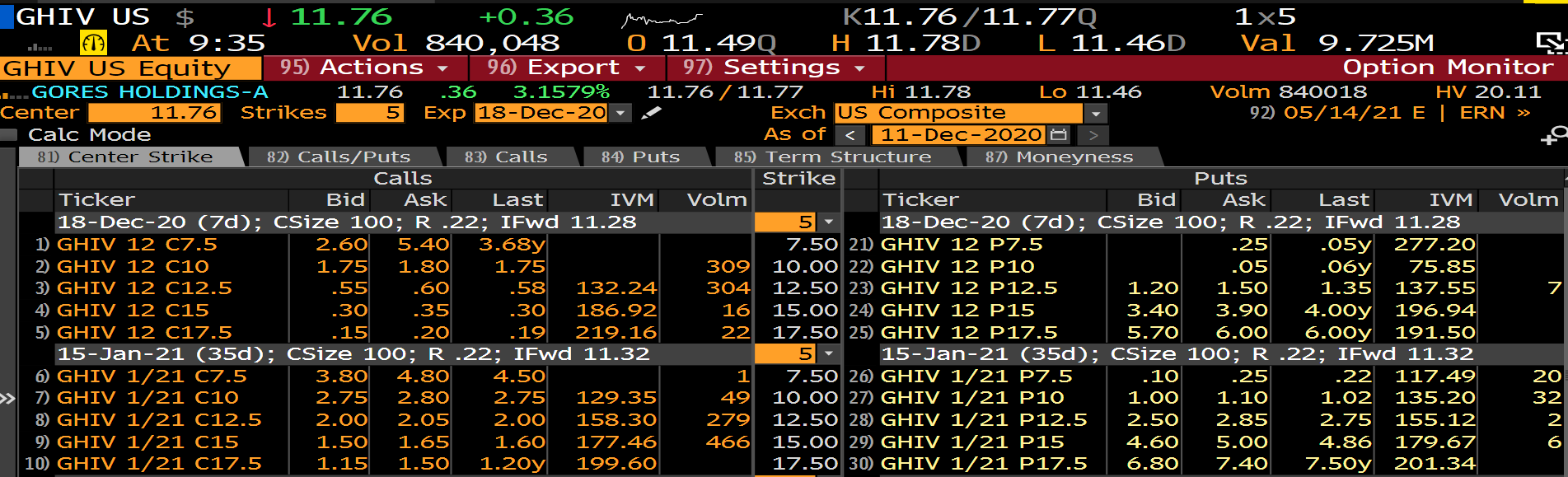

The idea? Buying Gores Holdings (GHIV) and writing January $15 calls against them to bring your cost basis below $10/share (trust value). (As I check before publishing; the buy / write would net to ~$10.10/share. Patience will let you get this below $10, or you could write the $12.50 and get a cost basis substantially below $10)

The thesis here is very similar to the one from “assessing IPOC’s options".” Gores has announced a merger, and they have yet to file their definitive proxy or schedule their shareholder meeting. With the holidays approaching, every day that Gores doesn’t file their proxy increases the chance that their shareholder meeting happens after the January options expire, in which case you’ve acquired the shares for less than trust and have something of a free roll (you can either sell the shares at a profit if they remain above trust value or continue to rise as the meeting date approaches, or you can redeem them and get trust value back).

For some timing backup, consider IPOC: yesterday (December 10), they published an S-4 setting their shareholder meeting for January 6th (yes, one day after I did a post noting that the timing was getting tight for IPOC to do their shareholder meeting before options expiration, IPOC filed their shareholder meeting before options expiration!).

GHIV has yet to set their shareholder date; at this point, the earliest they could set it is probably ~January 8th and by early next week it’ll become increasingly impossible for them to have their shareholder meeting by January 15th (the day the options expire).

So that’s the crux of the trade. Again, it’s very similar to the IPOC trade, so I’d encourage you to read that post.

I did want to build off of two points.

First, by no means does this trade fully rely on the shareholder meeting happening before the options expire. Yes, that is helpful, as it provides a huge leg of downside protection. But for this trade not to work, shareholders would need to vote for a deal on Jan. 6 or 8th or whenever GHIV holds their shareholder meeting and choose not to redeem their share for ~$10/share in cash. They would then need to sell those same shares for <$10/share within one week. Impossible? Certainly not! But definitely unlikely, particularly when you consider the sponsor history here.

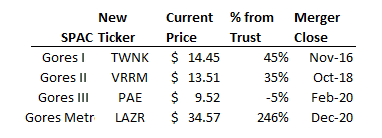

I noted in the IPOC post that “buzzy” SPACs have tended to see their shares rise into deal close. I don’t think GHIV is the buzziest SPAC in history (their target, UWM, has a nice story and enjoys some nice near term tailwinds, but I do think there are longer term questions on the business trends once the current refi and home buying boom slows and I don’t think anyone has ever associated “wholesale mortgage” with “buzzy”), but I would note that Gores (the sponsor) has an incredible track record. Despite the letters “IV” in the ticker, GHIV will actually be Gores’ fifth SPAC to complete a deal. The first four included one solid deal (TWNK), one deal that was a homerun until COVID destroyed their business and turned it into a merely good deal (VRRM), one deal that completed just before the pandemic and has been reasonably flat but seems to have some potential (PAE), and one speculative deal that just completed and is one of the best performing SPACs of all time (LAZR). I’ve laid out the results below; I do this just to show that Gores is a real sponsor with a real history of producing good SPAC deals. I think there’s a good chance GHIV gets a little “buzzy SPAC bounce” as the merger date approaches.

The last thing I wanted to talk about is the downside: what happens if there’s a huge market crash and all SPACs get hammered? I’ve mentioned several times I think SPACs are a bubble and bubbles can pop quickly, so that’s absolutely a risk. The largest and most obvious way this risk would play out is the shareholder vote happens before options expiration, shareholders approve the deal, and then the whole market tanks.

Again, it’s a risk, though I think it’s a remote one and that the odds suggest the SPAC is more likely to rise than fall into deal close (as mentioned above!). But it’s worth pointing out one other mitigating factor here: if there’s a mammoth market sell off, it is 100% within a SPACs rights to delay their annual meeting to sort through who their new shareholders are and to try to convince redeemers to hold on to their shares.

So, in the event where GHIV sets their shareholder date before the options expire and we have a market crash in between now and then, there’s a chance GHIV decides to push their shareholder vote back simply to reach out to new shareholders and try to stem the wave of redeems that would be coming.

It’s unlikely…. but it provides another mini-downside protection angle to the trade as it would push the shareholder vote well past the date when these calls expire.

(One other thing: GHIV has already indicated they’ll start to pay a $0.40/share annual dividend once the deal closes; that could drive a little buying into the stock once the announcement is officially made. That’ll be well after the deal closes and hopefully after this trade as worked out successfully, but I throw it out there because it will likely provide further incremental buying / support for the stock in the near future).