Yet Another $PSTH deep dive, part 1: framing the opportunity

I wanted to build out the PSTH thesis laid out in my two public posts a little further (ok, a lot further), because I think the risk/reward on the PSTH options is absolutely outrageous. My bottom line is nothing has changed from my two initial posts; I’m hugely bullish on the set up. In fact, the more I think through this, the more bullish I get.

If nothing has changed since the first two posts, why am I bothering to spend more time on yet another PSTH write up? Because I’m an absolute sucker for providing the disclosure that nothing on here is investing advice, and that options are extremely risky so please do your own work / talk to a financial advisor. But, aside from that love of disclosure, I wanted to write more on PSTH because PSTH’s structure is unique, and while I think that uniqueness presents huge opportunity, it also introduces a lot of potential complexities if you really drill down into how a bunch of different scenarios work. Writing helps me think clearly, so I’m more posting this write up to hold my feet to the fire and make sure I’m thinking about every angle of what is an increasingly large position clearly than posting it for views / likes / new followers / new subs (though all of those are nice too!).

I want to dive super deep into PSTH because I believe the options chain is one of the most mispriced investment opportunities I’ve ever seen. I think it is extremely alpha rich for sophisticated investors willing to do the work and think about it; in particular, over time I’ve come to think buy-writing the stock is perhaps the most mispriced event situation that can be done at scale I’ve ever seen. So I wanted to dive super deep into this both to lay my thinking out and to see if other sophisticated investors can poke holes in my thesis.

I do feel a little silly diving this deep as most “investors” seem to be interested in PSTH on the theory “stonks go up; this big stonk so it go up big”, but I do suspect that a large part of the opportunity here is being driven by that dynamic. I think the craziness of the past few months have taught novice investors a lot of very dangerous lessons, and one of those dangerous lessons has been “buy call options on sexy stocks that can only go up.” Again, that’s a super dangerous lesson that will likely end poorly, but in the mean time that creates opportunity to figure out ways to be on the other side of that trade.

For those who haven’t read the prior two posts (which I would encourage you to do in prep for this one!), the thesis on the PSTH options can be broken down into a few quick points.

Volatility on PSTH is absolutely insane at around 100% implied volatility. For comparison, the implied volatility on Tesla (TSLA) is around 60.

PSTH is a tontine structure. That tontine structure is unique, and things that are unique have a higher chance of being mispriced

A combination of the previous two points, the high vol and PSTH’s tontine structure makes the options chain incredibly compelling, as depending on the timing of any deal and how the deal is structured the options chain is pricing in some dramatically different stuff.

Put it all together, I think the options are perhaps the most mispriced / misunderstood / alpha rich opportunity I’ve seen in event land.

I’m going to split this post up into two parts. In today’s post, I’m diving deep into each of the points above, plus some other random points that pop into my head. Tomorrow, I’m going to use this post as background and dive into some scenario analysis to show why I think the options are so attractive (update: part 2 is now live here). I will be upfront: I am going to go into the fudging weeds here, so this could get technical. Now is a great time to reiterate the disclosure that applies to everything on this site: nothing on here is financial advice, and options are incredibly risky; again, not financial advice, do your own work, consult a financial advisor.

Point #1: PSTH’s volatility is wild

Why do I think PSTH’s volatility is wild? After all, PSTH is a SPAC; a SPAC is a cash shell looking for a deal. In effect, you could look at a SPAC as call option on a good deal (if they announce a good deal, you get the upside; if the announce a deal you don’t like, you can redeem for cash). Couldn’t you argue that, given a SPAC is a call option, an option on a SPAC should trade with huge volatility as it’s effectively an option on an option? Perhaps there is some basis to that crazy high volatility in this market (after all, as I write this CCIV is trading at >5x trust value on the rumor they’re going to announce a Lucid deal), but intellectually / rationally I still think it’s wrong.

The call option associated with a good deal for any SPAC should be much smaller and much less volatile than the market is currently pricing in. Every dollar of upside from “announcing a good deal” is a dollar of value that the seller leaked by selling their company too cheaply (i.e. if a deal is announced and a SPAC with $10 of trust trades for $20, the market is telling the seller they priced their equity for 50% of its market value); this is then compounded by the fact that most SPACs announce deals concurrently with a PIPE (private investment in public equity) priced at trust value alongside the deal so that all of the upside from a good deal does not go to the SPAC shareholders. PSTH, for example, has a $3B forward commitment from Pershing (PSH) to buy units at $20 (trust value) when a deal is announced. PSTH is a $4B SPAC; if we assume that the PSH forward commitment is the only PIPE attached to whatever deal PSTH ultimately does, then ~43% of the upside ($3B in forward commitment divided by $7B total trust + forward commitment value) from any good deal will go to PSH through the forward commitment, not PSTH shareholder directly.

Note that this is a little bit of simplification: I am ignoring the possibility of the PIPE being expanded to include more investors, I am ignoring the dilution from the sponsor warrants that will further sap upside from a good deal (a very meaningful expense!), I am ignoring any other fees and such associated with a deal (bankers fees, transaction fees, etc.), I am ignoring the tontine warrants attached to the PSTH shares, and I am ignoring the very real “winner’s curse” issue that I think all SPACs face and that will eventually be a problem for the sector. Still, I think all of the complexities point to even more value leakage from a deal than I have simplified down to, which suggests that PSTH’s implied vol and the premium to trust it’s trading for are baking in an even larger value gain from a deal than I’ve suggested.

Also remember that PSTH is a SPAC designed to go after “unicorn” targets. PSTH is the largest SPAC ever: $4B in trust with a $3B forward commitment. That’s $7B in equity value for PSTH. Realistically, the smallest company PSTH could announce a deal with would need to be valued at around $20B. Those types of companies aren’t exactly desperate for liquidity right now: VC firms are more than willing to make big investments in pre-IPO companies, the IPO window is wide open, and there are plenty of other funding sources out there (including other SPACs that could raise a huge PIPE). So PSTH’s current huge premium to trust and implied volatility (in effect, baking in a good chance of PSTH announcing a deal that drives shares even higher) suggests that PSTH will be able to announce a deal that hugely underprices the target despite the target having a ton of other options for raising money.

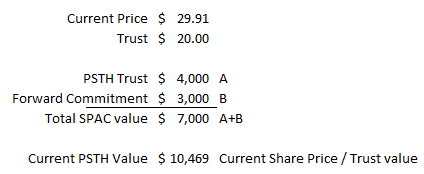

Maybe putting the numbers down will help show this. As I write, PSTH is trading for ~$30/share. Trust is $20/share, so PSTH trades for a 50% premium. Trust is $4B, and PSTH has up to $3B in forward commitments, so the total “SPAC value” is ~$7B. At market prices, that $7B is being valued at ~$10.5B.

With $7B in trust, PSTH would be taking a significant piece of any business they merged with. The largest SPAC merger ever was GHIV / UWMC, which was valued at $16B. PSTH is almost certainly targeting something multiples larger than the UWMC deal. I’ve included a table below that shows how much ownership PSTH would get of any target deal they struck in addition to how much the company would be worth based on PSTH’s current market price and the degree of underpricing of the target. So, for example, with $7b in trust + forward commitment, PSTH would own 10% of a deal if they valued the target company at $70B, and with PSTH currently trading at ~$30 (a ~50% premium to trust), the market is saying that a company who agrees to sell themselves for $70B company is worth ~$105B (and the market is saying that without even seeing the deal or knowing the company!). In effect, the seller has underpriced the equity in this deal by $35B, and with PSTH getting 10% of the deal, the seller has just handed PSTH ~$3.5B in value. Note that the math for “seller giveaway to PSTH” works the same way no matter how large the deal is or how much of it PSTH takes; at ~$30/share, the market is assuming the seller is transferring $3.5B in value to PSTH.

Ok, so what does showing how much of a business PSTH will own and the value transfer from the seller have to do with the volatility in the options?

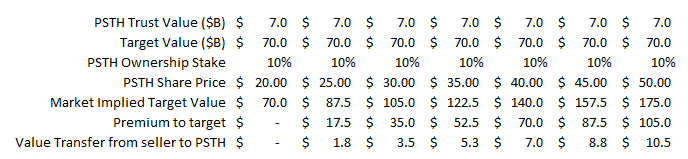

I wanted to highlight two things: First, I wanted to show that the bigger the target is, the more notional dollars the market is assuming they give up to merge with PSTH. For example, if a $100B company decided to merge with PSTH, at current PSTH prices the market is basically assuming they’re willing to underprice themselves by $50B in order to go public through PSTH. Given how wide open the capital markets are right now, that does feel like a stretch!

Second, I wanted to show how much value transfer the options are assuming happens. If you’re buying a $40/share option, you’re effectively assuming the target is willing to price themselves for half of what they’re really worth. That’s a $7B wealth transfer from the seller to PSTH’s shareholders. I’ve included a table below that shows the different levels of wealth transfer at different PSTH stock prices (so, for example, a $70B company is would give PSTH 10% equity ownership; at $40/share, the market is assuming that company is actually worth $140B and the sellers just gave PSTH $7B in wealth!). And remember: this math would get even worse (i.e. implies a larger value give away) once you factor in the sponsor warrants, chance for a larger pipe, transaction fees, etc.

Let’s round this up with a summary.

Summary of point #1: PSTH’s volatility is absolutely wild. It’s above some of the most volatile stocks on the public markets. PSTH is designed to take a multi-billion dollar unicorn public; the high volatility is effectively pricing in larger and larger chances of the target company giving away billions of dollars to PSTH’s shareholders. Between other SPACs, the IPO window being wide open, and huge windows for late-stage / pre-IPO investment, whatever business PSTH is targeting will not lack for liquidity options, so the market is basically saying the target will chose to give away billions to PSTH’s shareholders for some reason (maybe because they are unsophisticated, maybe because Bill charms them with his silver foxiness, or maybe just because Bill is willing to bet the market will give the target company a way high valuation than anyone else would ever believe and the market will prove him right! Either way, I like selling the calls against stock because it effectively is underwriting a bet that a seller won't hand billions of dollar in value to PSTH by selling themselves way too cheaply.

On to point #2

Point #2: PSTH is a tontine structure

I’ve dived into the tontine structure a bunch in my prior write ups, so I’m not going to go too hard here.

You can read more on tontines here, but basically it’s a pool of money a group of people form that is eventually distributed back to the survivors. That structure makes it great for story lines and intrigue; if you’re a writer, a great (if basic) story line is a group of 10 people formed a tontine, and now one of them is looking to kill the others in order to collect the payday. They’ve been pretty popular in pop culture, including in episodes of Archer and The Simpsons.

Pershing’s Tontine structure works in the following way: right now, each share of PSTH trades with 2/9 of a warrant. Just like a normal SPAC, PSTH will eventually announce a deal and give shareholders the options to keep their shares and roll it into the new company, or the redeem their shares for trust value. However, unlike a normal SPAC, PSTH’s tontine structure means shareholders are given something if they roll their equity / lose something if they redeem. If a PSTH shareholder decided to redeem their shares, they lose their 2/9 of a warrant. If a shareholders decides to vote for the deal / not to redeem their shares, they get to keep their 2/9 of a warrant; in addition, any warrants that were forfeited by redeemers will be distributed evenly among any shareholders who don’t redeem (p. 6 of PSTH’s S-1 goes into the structure a little more). This tontine structure is unique (I’m only aware of one other tontine like structure on the public markets: Starboard Value’s SPAC, SVAC).

This uniqueness is important for a few reasons. For example, this is a little simplistic, but I’ve found that things that are completely unique in the financial markets present increased opportunity for mispricing because they can fall into a research gap bucket (where no one group at an investment bank or major investment company feels the need to take ownership of that security because it doesn’t tightly align with the other securities they cover, and so it can go underfollowed) and because unique things can often have wider than normal outcomes because they are 1 of 1 (i.e. if you’re looking at a major oil and gas company, it’s unlikely their financials results dramatically defer from peers; if you’re looking at the only company that is attempting to go to Mars, the end game for them is likely to be very unique!

Summary of point 2: Pershing’s Tontine structure is unique, and uniqueness in financial markets often means opportunity.

That may seem a small point… but the tontine structure is important because, combined with the high volatility, it creates the mammoth opportunity in the options chain I’ve been discussing.

Point #3: high volatility and tontine structure create mispricing in options structure.

In my first PSTH post, I described how options could “get DVMT’d” and how I thought PSTH’s options would get “reverse DVMT’d”. Basically, a reverse DVMT would happen when PSTH completes their merger. The options chain would adjust so that the deliverable went from one share of PSTH to one share of PSTH plus however many tontine options remaining shareholders kept.

So, for example, let’s say that every share decides to roll into PSTH’s deal (no redeemers). In that case, each share would get 2/9 of a warrant. The options chain should adjust so the deliverable is now 1 share plus 2/9 of a warrant.

Why does this matter?

Remember, a warrant is basically a long dated call option, so its value will change dramatically with volatility. A PSTH share has 2/9 of a warrant embedded into it, so buying and selling options on PSTH right now is, in part, buying/selling an option on an option (actually, since PSTH is a SPAC and SPACs are options on a deal; selling an option on PSTH right now is effectively selling an option on an option that also includes a long dated option inside of it). As the option's value goes up, the warrants value goes up, and vice versa. There’s something to that circularity that can create interesting hedges and trading structures.

The tontine structure also makes the tail risk options on PSTH somewhat circular and more protected than you would think. Consider, for example, you’re thinking about selling a Sept. $20 put. As I write this, those are trading for $1.75/share. PSTH has $20/share in trust value, so you might be thinking “by writing this, I’m betting PSTH won’t trade below trust value.” I think you’re partially right, but I actually think it’s better than that. If PSTH announces a deal the market doesn’t like, the stock will likely trade towards trust value and there will be some redemptions…. however, redemptions mean that the remaining shareholders will be given more warrants when the deal closes. So, as you get more redeemers, remaining shareholders get more shares of the warrant, which means the put becomes less valuable since it adjusts to include more warrants in the deliverable. For example, say enough shareholders redeem that the remaining shareholders get 3/9 of a warrant instead of 2/9 of a warrant. Suddenly, the deliverable for the $20 puts (post deal) go from one share of stock plus 2/9 of a warrant to 3/9 of a warrant. In addition, extra shares redeeming likely means the remaining company will be a little more levered than originally anticipated, which means the volatility on the stock goes up a little bit more. So, as the shares drop towards the value of the out of the money puts, the underlying basket that the puts will represent goes up in value because the basket will be a bit more volatile and represent a couple of extra warrants, making the puts less likely to be executed.

Selling optionality is an interesting hedge in another way. Remember, the market is pricing in volatility for PSTH without knowing what business PSTH is targeting, and vol will rise or fall dramatically depending on what company PSTH targets. For example, one company that has been floated around as a PSTH target is Subway (the sandwich chain). I think that deal is unlikely, but obviously the volatility attached to something like Subway would be dramatically different than if Ackman bought something “sexier” like Stripe or SpaceX, because Subway would be a low-ish growth, steady business while Stripe and SpaceX are fast growing tech companies attacking massive TAMs in pools that are winner stake most.

Again, that creates circularity in the structure. If you buy the stock and sell calls against it, the call’s value will rise and fall in kind with the warrants. So, if Ackman announces a low-vol deal like Subway, the warrants will likely fall in value alongside the calls, while in a higher vol deal both will rise. If you believe (like me) that the market would be super enthusiastic about a higher vol deal (like Stripe) but would hate a lower vol deal (like Subway), selling the options becomes an even more attractive hedge (if he announces a low vol deal, your stock drops in value but the calls do as well).

Note: for all of this point, I have assumed that PSTH options get “reverse DVMT’d;” the options chain adjusts to reflect the tontine warrants after a deal closes. Increasingly, I like buywriting the stock (buying the stock, selling calls against it) more than I like selling puts, because I think a buy-write benefits from all of the circularity here (options value rises and falls alongside warrant value), but it also benefits from the tail scenario where the options don’t adjust (i.e. if you buy the stock and sell calls, and the options don’t adjust post deal; you’ve just gotten the tontine warrants for “free”). I’m 90%+ certain that the options will adjust, but I think buywriting the stock just to pick up on the optionality if they don’t adjust is worth it. I will build on this more in tomorrow’s post

Summary of point #3: the combination of high volatility and PSTH’s tontine structure creates strange circularity in PSTH’s structure (which I believe lends to the opportunity). Puts written close to trust value will have an increasing amount f warrants assigned to them if a “bad” deal is announced and the stock sees some redemption. Buywriting the stock is intersting because the value of the calls rises and falls in direct correlation to the value of the tontine warrants.

Ok, I think I'm going to stop this post here. In tomorrow's post, I'll go through some scenario analysis and example trades that I think are particularly attractive.