Feb. 2021 premium update (paywall)

Hi subs,

Before we get to the updates- first, thank you so much for subscribing to the premium site!

Second, a quick housekeeping. This month’s housekeeping has three parts:

I mentioned it in my 2021 vision, but my goal for the premium site is simple: 2 posts/month (24 posts a year). One of the monthly posts will be a well thought out and actionable idea (at least in my mind it will be!); the other post is the monthly premium update that will provide thoughts/commentary on any ideas that have news or new thinking behind them.

As we noted in August, we’re now running the premium site through both substack and the blog. The content on both is identical, so there’s no need to sign up for both. However, if you’d like both (or you signed up for one and want the other), obviously we can accommodate that. Simply email Rob at resterner@rangeleycapital.com and he can make sure you have access to both without incurring additional fees or anything.

I know it’s complicated to have two systems, so thank you for bearing with us. Our hope is that, over time, running the site through the blog will give us the optionality to introduce new features to increase the value of membership. In the mean time, I try to include links to articles for both the blog and substack to make following back to links and ideas as easy as possible.

If we ever have added features on the blog that we can’t have on substack, we’ll of course let you know! Thanks again for bearing with us, and always feel free to reach out if you have any questions / concerns

The premium site is always a work in progress, so feedback is very much appreciated.

You can always reach me at awalker@rangeleycapital.com with any questions / concerns etc.

I’ve introduced a new segment at the bottom of this post that includes every past idea, both open and closed ones, and links to them for your convivence in looking at / refreshing on past ideas.

In last month’s updates (substack / blog), I called out GTXMQ as my highest priority premium idea, with AMBC, SIGA, and WOW still high priority as well. With GTXMQ having gotten a $7/share offer and trading just a little below it as I finish this up, I’d take it off my highest priority list (though I still think it’s rather attractive, so I’m keeping the rec open until the bidding war shakes out). In place of GTXMQ, I’d add both JEF (Feb. 2021; substack / blog) and CURO (January 2021; substack / blog) to my highest priorities list; I would also always highlight IAC as an interesting situation; the immediate upside isn’t as large or (potentially) as fast as the other companies but if you asked me for one stock to buy and hold for the next 5/7/10 years and substantially outperform the market, it would be IAC (I mentioned it a little in this post on building conviction).

On to the updates

AMBC- The company announced a small deleveraging transaction at the end of January. We should know more when they report earnings in the next few weeks, but I’d anticipate that deal drives a little bit of incremental book value. They also announced plans to pursue a specialty insurance business. I think that’s an EV negative pursuit, but I’m willing to be proven wrong. Still, shares trade at a huge discount to book, and I still think there’s a path to AMBC wrapping up their lawsuits and seeing a huge boost in book value sometime this year. Note that MBI settled with CS this month; the settlement “materially exceeds” the amount recorded on their books, so MBI’s earnings should provide another clue to how large the potential gain from AMBC’s suit could be.

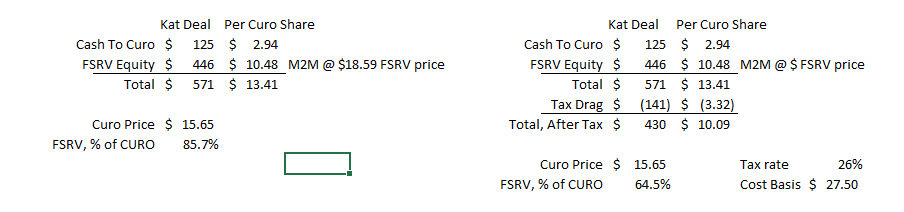

CURO- Two big items here: they reported Q4’20 earnings, and they bought a stake in Flexiti. Before I dive into those, just a reminder: the most important thing here remains that CURO is screamingly cheap. At current FSRV prices (the SPAC who will buy CURO’s stake in Katapult for stock and cash), CURO’s stake in Katapult is worth between $10.00-$13.50/share (depending on if you tax adjust or not). CURO is trading for just over $15/share, so the vast majority of CURO’s value is fully covered by FSRV. CURO’s core did $1.77 in EPS in 2020, so looking through FSRV you’re paying a low single digit EPS multiple when you buy CURO.

Anyway, CURO’s earnings were fine. Runoff driven by regulatory changes and pulling back on loans in the face of the pandemic (plus stimulus resulting in less loan demand) meant earnings were lower, but this is reasonably offset by CURO’s low multiple and the strong credit performance given stimulus and lower balances. The most exciting story here is really the Flexiti acquisition; CURO appears to be paying a reasonable valuation given the growth prospects, and given CURO’s history with Katapult and some synergies, I wouldn’t bet against this deal being an absolute homerun. The nice thing about CURO is, at today’s prices, you’re basically paying nothing for the chances Flexiti does end up being a smash. I think the quote below helps frame the opportunity; remember that CURO has ~43m shares out so $20m of net income accretion in 2022 would be almost $0.50 in EPS (to be fair, the accretion is driven by swinging from a ~$10m loss to a $10m profit).

GTXMQ- The equity committee updated their standalone plan to offer $7/share to shareholders who want to cash out. Recall that the thesis here as evolved over time as the bankruptcy process has played out, but the most updated thesis is that the current plan (which offers shareholders $6.25/share) represented a floor value with the potential from improvement if we saw competing bids, so the equity committee plan fits perfectly into that thesis. I think the odds are good that the current group will need to improve their bid in some form to get their deal through. Shares are trading above $6.25/share, so the thesis is a little different than I was pounding the table on it ~a month ago at $6.25, but I still think the risk reward is very attractive.

IAC- What to say about IAC? Shares have enjoyed a massive run on the heels of selling more of Vimeo as they move closer to spinning it off, and their earnings revealed almost all pieces of their businesses are firing on all cylinders. As a compounder, this company is among the best in the world to put cash to work in, but I will say that the current valuation is much fuller than I’m used to. Despite that, I think there’s mammoth upside and optionality over time, so I continue to hold my stake here with the plan to #neversell (well, never sell IAC. I expect to eventually sell the spins if and when I receive them!).

LGF- I recommended Lionsgate last summer (May 2020; substack / blog) on a pretty simple thesis: they traded way below what they’d be worth in any M&A, and their controlling shareholder was buying stock on the open market and making a bunch of moves that signaled some corporate actions might be on the horizon. The company is still reasonably priced (its EV is ~$5B, roughly the value CBS offered for just Starz two years ago), but we haven’t seen any of the big corporate actions I thought could be pending, and I am increasingly worried about a bunch of pieces of their strategy (in particularly, with every major media company focusing on their D2C strategy, I’m worried Starz goes from niche player to irrelevant over time), so I’m closing this idea out.

VTRS- Nothing particularly new here. There was an insider buy at the end of 2020. Shares have been reasonably flat, as their cheapness has somewhat been offset by a conservative guide at the JPM healthcare conference. The overall thesis here is still very much intact; this was one of the worst publicly traded culture / governance companies, and the continued focus on “performance-driven” culture post-merger / with the new management team should be really good for them over time. We should have some more info on them in the near future; earnings arel later this month, they have an investor day in early March, and the dividend turns on in Q2.

SNEX- Their annual report is worth reading. The near term here looks pretty good; annualizing Q1’21 earnings, they’d do ~$5.80/share, so they’re currently trading for ~10x P/E. They’d be a huge beneficiary of rising rates (a 1% rise in interest rates would increase annual EPS by between $0.50/share to $1/share; likely closer to the high end of that range), and the stealth bull markets in commodities is very good for them (management called out a “very positive market” for physical trading of precious metals). As they fully integrate Gain, we should see a big capital release which will free them up to buyback shares or pursue M&A. I continue to think the thesis is simple: fair value is easily $80/share (~2x book) given I think they can sustainably achieve a 15% ROE (with the potential for upside given their history of strong deal making).

Prior Ideas still open / actionable

SSSS (July 2020 idea; substack / blog, though the November update (substack / blog) was important)

GTXMQ (originally publicly published, but a fairly lengthy premium update in October 2020 (substack / blog) and an update on the new bid in January 2021 (substack / blog))

Prior Ideas, Closed

IWG (April 2020 idea); closed November 2020 (substack / blog)

COOP (May 2020 idea: Substack / Blog); closed August 2020 (substack / blog)

KTB (June 2020 idea); closed January 2021 (substack / blog)

WUBA special sit (July 2020 idea; substack / blog); merger closed September 2020

WOR- (July 2020 idea; substack / blog); closed September 2020 (substack / blog)

JWN (October 2020 idea; substack / blog): closed December 2020 (substack / blog)

CNNE (September 2020 idea; substack / blog): closed December 2020 (substack / blog)

MAC (April 2020 idea; substack / blog): closed December 2020 (substack / blog)

TCO prefs (our first idea in March! Substack / blog): closed December 2020 (substack / blog)

GHIV (December 2020 idea; Substack / blog); closed January 2021 (substack / blog)